In recent months, Europe’s economic outlook has continued to be hampered by uncertainty and the impact of ongoing trade tensions. In light of these uncertainties, treasurers have more reason than ever to make sure they are working towards a sustainable liquidity position.

With that in mind, they have good reason to consider the benefits of trade receivables financing structures that provide for a sale of the underlying asset, rather than a loan against a collateral base. These most commonly take the form of one of two well-established trade receivables finance structures: factoring and trade receivables securitisation (TRS).

These financing forms have both been around for a while and share the basic economic principle of monetising corporate customers’ accounts receivables. The principle is straightforward – but while the two products have much in common, there are also considerable differences.

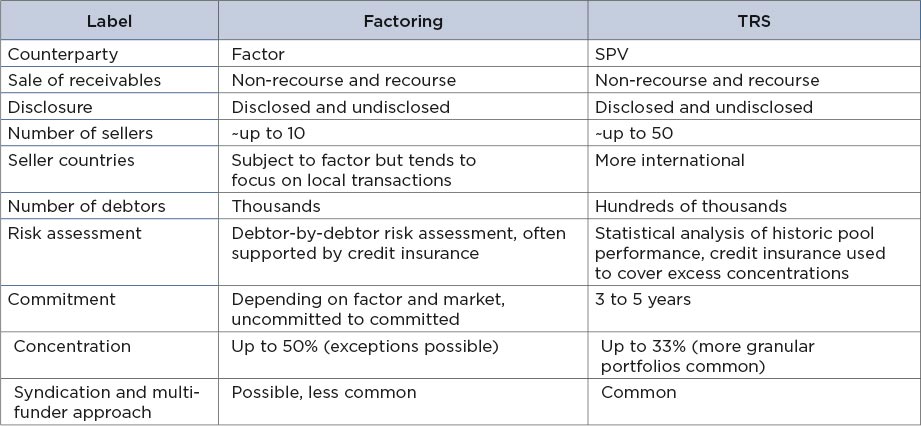

In both structures, the starting point is a corporate (often referred to as the seller) selling its receivables to a factoring house (factor) or a special purpose vehicle (SPV). In both factoring and TRS, the seller may sell either a defined part of its receivables portfolio, or the whole book.

However, even in this aspect there is an important difference between the two products:

The respective syndication capabilities of the two products is another key differentiator. Factoring facilities are often structured as direct receivables purchases, which in most cases limits their capacity to be syndicated from a practical perspective. TRS structures, in contrast, are regularly syndicated to a market of more than 20 experienced investors in Europe alone. This provides significant flexibility to extend facilities beyond the original amount and refinance if required at maturity.

There are also some significant differences between factoring and TRS structures when it comes to the size of the facility and the risks involved.

For factoring, the number of sellers (ie operating and billing entities of a corporate) that can be included in a facility is usually limited by the technical and operational capabilities of a particular factor. Structures are unlikely to include more than 10 sellers in a single facility, although this depends on the factor’s scale and operational readiness.

The countries in which the sellers are based are another consideration for the factor. Larger factors (especially those with an international footprint) tend to offer factoring facilities in a wider range of countries. Generally, however, factoring is considered a more local business, partly due to local law and operational requirements.

TRS facilities, in comparison, tend to be more flexible in terms of the number of sellers and the countries in which they are based. Transactions can accommodate a significant number of global sellers into a single structure – albeit with the setback of higher upfront fees, which are needed to ensure the true sale according to the respective local law.

From a risk perspective, factors will focus on the debtor’s default risk (especially in non-recourse facilities) and the dilution risk inherent in the receivable. Getting comfortable with the debtor’s default risk is a credit decision that is often supported by the use of credit insurance.

To a certain extent, the number of debtors that can be factored is limited by the factor’s ability to assess the inherent credit risk and operationalise the facility. How factors assess dilution risk differs from market to market – and from factor to factor – and is mainly about right-sizing of the reserves agreed upon in the factoring agreement.

The inherent risks a funder assumes in a TRS are similar to those incurred in factoring, even though the approach taken to analysing those risks can differ significantly. In a TRS, receivable portfolios are typically less concentrated, forming a homogenous pool of receivables. This justifies a statistically based underwriting approach, in contrast to the debtor-by-debtor risk assessment taken by a factor. Credit insurance can be used to cover excess concentrations in the portfolio, instead of covering the majority of the portfolio.

Given this risk approach, and based on modern technological capabilities, the number of debtors that can be included in a TRS facility is significant – while this is not unlimited, it is possible to include hundreds of thousands of debtors. Additionally, the legal structure of a TRS allows for a cross-collateralisation of receivables, due to the fact that a single SPV is used and the proceeds will be distributed according to the transaction waterfall to the funder and other stakeholders.

The documentation of factoring transactions is straightforward: a standardised receivable purchase agreement (tailored to accommodate local law requirements) is entered into by the factor and the seller. Factoring agreements govern the contractual relationship and economic terms of the two main participants of a factoring facility.

Other considerations are as follows:

TRS structures, meanwhile, are associated with a more complex legal structure and a higher number of involved parties:

As previously stated, in a TRS structure, the advance rate is determined based on statistical models that reflect the historic performance of the receivables pool. This is also the main driver behind adjustments of the reserves and advance rate during the contract duration.

When comparing the basic functionalities and structures of factoring and TRS, it is clear that factoring is best suited for small to upper mid-market transactions (for example, up to €150m in facility size) with a local or limited global footprint, and for corporates that are looking for a tool to monetise their receivables portfolio. Factoring can also be used as a more tactical tool to cover spikes in liquidity demand.

TRS, meanwhile, is best used as a more strategic and scalable long-term financing solution, which can be used to monetise a sizeable receivables portfolio across various seller jurisdictions. TRS also enables the seller to enter into a multi-funder facility with a larger group of funders.

The good news for treasurers is that irrespective of which of these two products is more relevant, both do provide a significant positive liquidity effect – and can therefore help corporates prepare for future economic uncertainties. It’s just a question of picking the right product and tailoring it according to the individual company’s needs.

Johannes Wehrmann is director of working capital solutions at Demica