Banks in emerging markets are structurally inclined to take advantage of, and even initiate, technological breakthroughs. Indeed, they have sometimes turned into real laboratories for testing new products.

Today’s market calls for ‘reverse innovation’ (as opposed to adapting products developed initially for developed countries) and low-cost products and service, ie simple and inexpensive (but not

low quality). It also calls for emerging market-specific multi-distribution channels, which is the only way to reach highly dispersed target markets in the context of poor infrastructure.

Unsurprisingly, emerging countries have become the main regions for testing and using mobile phone payment services (notably in Kenya), while the latest generation of biometric ATMs has been undergoing tremendous growth in certain mega emerging markets. For these reasons, the growth of banking networks is both necessary, and sometimes insufficient, to meet the challenges of these expanding mass banking markets.

Since the start of the financial crisis, commercial banks have tended to imbue ‘El Dorado’ qualities on certain emerging markets. Those markets are characterised by increasing penetration of the banking system; an emerging middle class; institutional changes; and technological advances. So major banking players have begun to bolster customer care over the long term by increasing the density of their banking networks in such markets at an unprecedented pace.

Our Emerging Banking Report 2012 shows that the crisis has put these ambitions under stress, however. First, the liquidity injection by central banks has led to a surge in loan-to-deposit ratios, particularly in Eastern Europe. Risk costs have also increased, which is highlighted by a serious deterioration in the provision/net banking income (NBI) ratio, but risk tracking measures remain ill-adapted to this customer base. In Eastern Europe and North Africa, the economic slowdown coincided with a sharp drop in NBI growth from 14% in 2008 to a mere 2% in 2011.

Major banking players have begun to bolster customer care over the long term by increasing the density of their banking networks

This financial climate has had significant repercussions on the economic fundamentals of banking networks. The race for size in recent years has greatly impacted profitability per client. In some cases, it has even led to a reduction in revenue per branch (adjusted for inflation). This has occurred in Romania since 2008 and, more recently, in Morocco, where investments have fuelled higher cost structures, denting overall sector profitability.

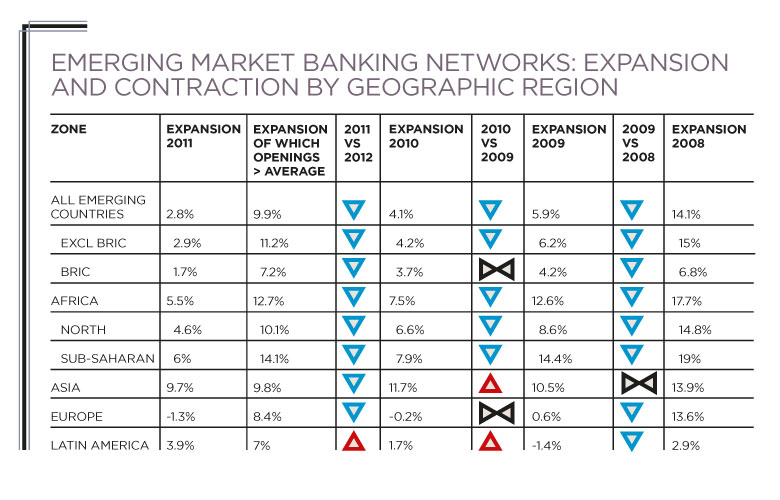

As a result of this challenging business climate, banks have adjusted their expansion strategies in emerging countries. Following the slowdown that began in 2009, banking networks expanded by just 2.8% in 2011, down from 4.1% in 2010 (and 14.1% in 2008). In a further sign of normalisation, just one in two banks grew in 2011. Only Latin America, which began its catch-up drive following the restructuring of its bank branches in 2008-9, is an exception. The region saw an average expansion in bank branch networks of 3.9% for 2012, compared with 1.7% for the preceding year.

But the story is more complicated than it seems at face value. The decline in the rate of bank network expansion conceals what is still a substantial hike in the absolute number of bank branch openings. Top 50 banks opened more than 6,000 new branches in emerging countries during 2011, which is equivalent to the combined branch networks of Barclays, Santander and BNP Paribas in their home markets. Brazilian bank Bradesco alone opened slightly over 1,000 branches in 2011. It was the fastest-growing bank in 2012, according to our annual 300 Ranking, replacing State bank of India, which opened 516 branches and had topped the ranking since 2008.

The general slowdown in expansion reflects the very different realities confronting banking players. BRIC banks have emerged from the crisis stronger thanks to the specific characteristics of their environments: legal protection of their domestic markets; natural barriers to entry due to size; established players suffering from a gradual decline in client acquisition; and high processing costs. Consequently, BRIC banks posted an average return on equity (ROE) of nearly 20% in 2011, which is about double the average across emerging countries. Although the growth pace slowed down, these banks still recorded high NBI growth of between 7% and 8% for the year.

Bank size has been a key differentiating factor. The biggest banks leveraged their positions to maintain profitability, posting 12% ROE in 2011 (up from 8% in 2009). In contrast, the agility of the smaller banks’ business models, whose slighter size was a key factor in their earlier success, has turned into a disadvantage during the crisis. Lacking the critical mass to absorb cost inflation, their cost-to-income ratios deteriorated significantly and now hover near those of Western markets.

Foreign-owned banks’ growth in emerging countries (1.7%) confirms the end of their period of expansion momentum. But in some cases – Latin America, for example – emerging markets are still a key growth driver for Western banks. For instance, given the weakness of the parent companies in Spain, Latin American subsidiaries of Spanish banking groups have even become bases of support and defence (49% of the combined NBI of Santander and BBVA).

Instead of basing their approach on the model developed by their Western peers, banks in emerging countries need to respond to the size and specific needs of their target markets. As with the densification of networks, the challenge for banks is to standardise and develop economies of scale while adapting distribution models to the specific needs of these regions. Firstly, they need to think in terms of ultra-mass market. For instance, Chinese bank ICBC has 282 million clients and State Bank of India has more than 13,700 branches. They also need to reach out to populations new to the banking system with the right product mix and suitable distribution channels.

The findings in this article come from the VELHON Partners’ Emerging Banking Report 2012

Yoann Lhonneur and Jean-Marc Velasque are managing partners at strategy consultancy VELHON Partners.

W: www.velhonpartners.com