In recent years, private credit, also known as private debt, has rapidly emerged as a vital source of capital for supporting the decarbonisation drive, particularly for SMEs. However, this evolution plays out against a challenging geopolitical landscape, where anti-environmental, social and governance (ESG) and sustainability sentiment, and political headwinds – particularly in the US – are threatening the growth in sustainable and transition finance.

This article outlines the role of private debt in enabling companies to establish more sustainable and climate-resilient businesses.

Sustainable finance is broadly defined as the integration of ESG factors into financial decision-making, resulting in greater levels of investment directed towards long-term sustainable economic activities and projects. Environmental aspects include climate change mitigation and adaptation; social criteria cover inequality, community investment and human rights; governance relates to how companies and organisations are run.

In policy terms, sustainable finance is understood as the process of mobilising capital in ways that support growth while reducing environmental pressures and meeting long-term sustainability objectives.

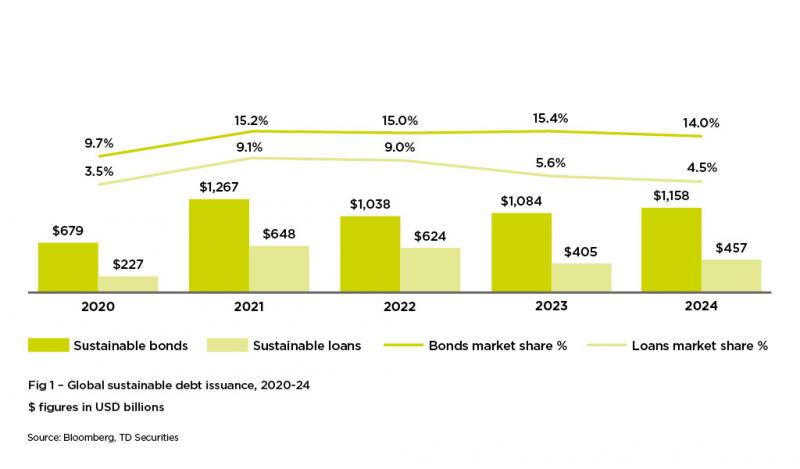

Volumes of sustainable debt have risen sharply over the past decade, reflecting growing investor and issuer interest, increasingly supportive policy environments and the urgent need to finance the net-zero transition. The market encompasses green, social, sustainability and sustainability-linked bonds and loans, collectively known as ‘GSS+’ debt.

In 2024, the global annual sustainable debt issuance (bonds and loans) reached $1.62tn, a 8.5% increase over 2023 and just below the record set in 2021 (see Fig 1).

The forecast for 2025 has volumes holding steady or modestly rising to around $1.8tn, buoyed by green bonds, corporate transition bonds and sustainability-linked loans. Cumulatively, by Q2 2025, the sustainable debt market surpassed US$6tn.

Transition finance is a subset of sustainable finance, geared to supporting high-emitting industries and ‘hard to abate’ sectors, such as energy, steel, cement, shipping and aviation, in gradually decarbonising in line with net-zero pathways. It fills a critical gap by enabling companies that cannot yet be low/zero carbon to fund strategic initiatives to reduce their emissions. Such finance includes loans, bonds and tailored investment products specifically targeting emissions reduction or the adoption of cleaner technologies.

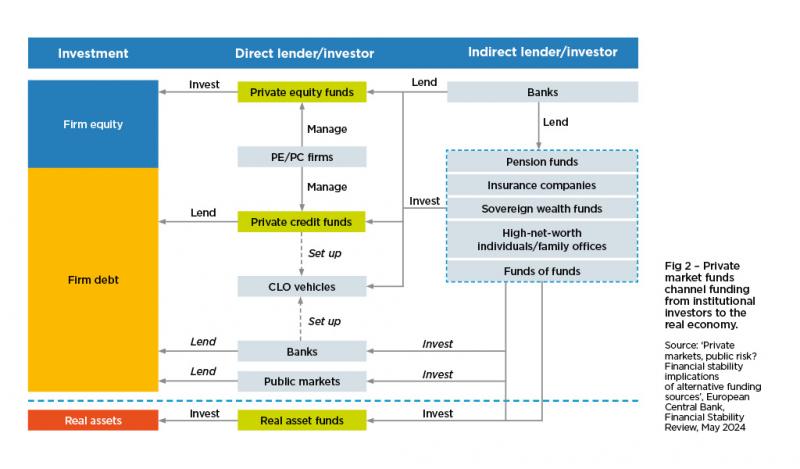

However, private credit is non-bank lending provided directly to companies by institutional investors, asset managers or dedicated private credit funds, such as those run by PE firms, rather than lending through banks or the public bond markets; such loans can vary from $30m to $1bn.

It is an illiquid asset class, typically involving bespoke loan terms and higher interest rates than bank loans, and often more flexible and tailored structuring. Private debt can be senior or subordinated, secured or unsecured, and has become a crucial alternative for businesses unable to access mainstream credit markets, especially those driving innovation or operating in sectors under transition to lower their greenhouse gas emissions.

The role of private debt as one of the sources of finance for a private company is outlined in Figure 2.

Since the 2008/09 financial crisis, the private credit market has grown significantly, reaching $1.5tn by January 2024, according to Morgan Stanley, and is expected to grow to $2.8tn by 2028.

Corporates, particularly SMEs, are turning to private debt funds to meet their financing needs, especially for sustainability and transition-focused projects, as they seek more bespoke financing solutions that banks are unable to provide. This is particularly vital in sectors such as industrials, infrastructure and emerging market energy, which have the ambition to decarbonise their operations.

The benefits for borrowers of such loans are: quicker approval process; funding certainty; and, usually, longer tenors (as the private credit fund investors have long-term horizons). During economic volatility, the lender also typically works with the borrower to restructure the loan.

Private sustainable debt now represents roughly 8–10% of annual sustainable credit flows, amounting to $157bn in 2024 and a projected $180bn for 2025. This share has more than quadrupled since 2018, reflecting intense Limited Partner (ie, investor) and borrower appetite for direct, flexible and impact-focused lending structures.

Transition finance relies on flexible and innovative approaches. Private debt’s ability to create bespoke loans, typically with covenant packages tied to ESG improvements or quantifiable decarbonisation milestones, makes it an engine for funding credible transition plans.

Private credit sustainability-linked (SLL) and transition loans, with interest rates or terms pegged to specific KPIs, are increasingly deployed to align borrower incentive with climate and other sustainability-related outcomes. For example, CVC’s SLL to SLR Consulting included KPIs on emissions, injury rates and women in leadership roles.

The rise of sustainable and transition finance has not come without headwinds. A growing anti-ESG backlash, especially in the US, and wavering political consensus around climate action present complex risks for market participants.

Regulatory uncertainty/pushback or the watering down of ESG reporting standards (eg, the EU’s Corporate Sustainability Reporting Directive) can dampen issuance and investor confidence, creating volatile flows and, potentially, stalling new product development.

Furthermore, the rapid expansion of the market has led to scrutiny over ‘greenwashing’ and the robustness of transition plans, especially for sustainability-linked instruments. Increased investor and regulator demand for credible impact and transparency is reshaping market standards. Those companies that have prepared their transition plans using the Transition Plan Taskforce’s frameworks and sector guidance, or BSI’s Flex 3030 Net Zero Transition Plans for SMEs – Code of Practice, should encounter fewer, if any, ‘greenwashing’ issues.

Geopolitically, especially in the US, there has been a backlash against companies’ sustainability practices and the providers of sustainable finance, while, outside the US, governments, regulators, investors and corporate leaders recognise the need for sustainable finance to decarbonise economies. However, a combination of geopolitical and macro-economic uncertainty has, according to NatWest, resulted in a 14% decline in private sustainable debt fundraising in Europe and North America in H1 2025; yet Europe is considered one of the most promising private credit markets globally, according to Apollo Asset Management.

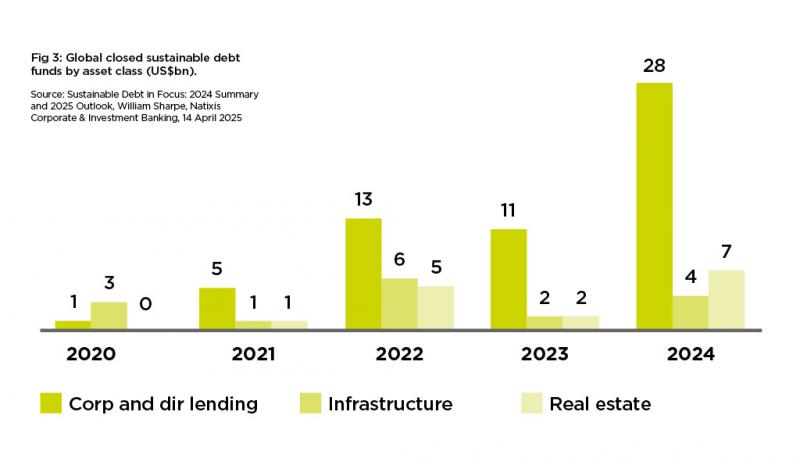

Private debt funds have a key role to play in providing bespoke, agile and scalable sources of sustainable finance to help companies effect their transition plans, particularly for SMEs, thereby reducing their enterprise risk, making them more resilient and increasing their value over the long term (Fig 3).

Transition and sustainable finance will be the backbone of the global economy’s path to net zero and long-term economic resilience, with private debt being key to unlocking capital for sectors and companies most in need of support and with limited access to bank or capital market financing.

Even as the geopolitical winds blow against climate policy in some regions, the structural need for flexible, impact-driven finance will mean that private debt will be a pivotal engine powering the transition.

Carel van Randwyck FCT FCA is an ACT Council member, ACT Certificate in Sustainable Finance for Treasury course co-author and tutor and partner at Rodford & Partners

This article first appeared in The Treasurer, Issue 4, 2026