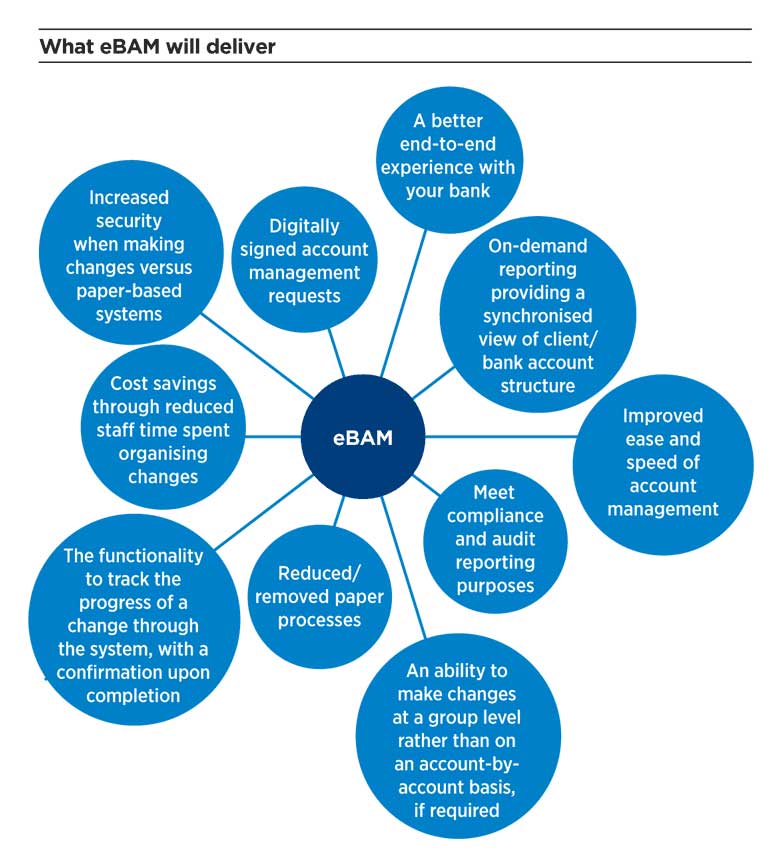

Opening and closing bank accounts and amending mandates to add and remove account signatories remains a labour-intensive and onerous task for many treasurers due to the paperwork required by their banks. Fortunately, advances in bank account management are making these processes much easier for companies with complex bank account structures.

Electronic bank account management (eBAM) is an industry-wide initiative within the banking sector. Its aim is to allow existing clients of a bank to open and close bank accounts, and to amend mandates on those accounts, via electronic rather than paper-based methods. In addition, eBAM uses legally binding digital signatures (electronic codes attached to documents that verify the sender’s identity and maintain document integrity), so treasurers will no longer need to collect and send signatures on paper to change the structure of their company’s accounts.

Another advantage of eBAM is the reporting capability that it provides

The international banking community has worked with corporates, messaging provider SWIFT and technology vendors to ensure that eBAM solutions and terminology are standardised across the industry and provide adequate support to multi-banked corporates.

Companies in the US are leading eBAM and digital identity adoption in significant numbers. Although uptake has been slower in Europe and the UK, realisation of eBAM is starting to gather pace as more corporates become aware of its capabilities. Asia is also starting to embrace eBAM, even though local regulators still require banks to capture and retain various legal paper documents. Running these in parallel with electronic processes is, at least, a step in the right direction.

Put simply, the benefits of eBAM are efficiency, visibility and control. When a paper request has been submitted to the bank, the client has no way of knowing whether it has been received safely and completed correctly. Furthermore, they cannot follow it through the bank approval process during which opening the account may take many weeks, possibly resulting in lost business opportunities and revenue for the company.

With eBAM, treasurers will be able to open and close accounts either through their treasury management system (TMS) if they have the necessary add-on software or through their bank’s proprietary portal. Both channels will be integrated with digital signatures, allowing for the easy collection of account signatories even if they are not physically present. Once submitted, treasurers will know when their request has been received, where it is in the bank approval process and when a new/additional account has been activated.

Another advantage of eBAM is the reporting capability that it provides. Corporates that use eBAM can get real-time reports on their bank account structures. This is a major boon when it comes to meeting audit and compliance obligations since businesses that adopt eBAM will be able to produce customised reports – for example, of individuals who were named on mandates over a certain time period – and demonstrate a high level of visibility and control over their banking arrangements.

It is also a good opportunity for companies to get their back-office account management in order by checking that individuals who have left the company are no longer named on mandates and to add new signatories where appropriate. They may also want to consider rationalising bank accounts and bank relationships as part of the housekeeping process since eBAM is not a single system across the banking industry. Instead, companies must have separate eBAM systems in place with all their main transactional banks.

Finally, although switching to eBAM will require some upfront investment in many cases, the actual day-to-day processes of opening and closing bank accounts and managing mandates should be no more expensive to companies because banks are not proposing to charge them more for using eBAM. Instead, it should be a way for banks to enhance the service that they provide to their clients.

So, how do you decide if eBAM is right for your business at this point in time? As a general principle, the companies that will get the most benefit from eBAM are those that have large numbers of bank accounts and complex mandate structures as well as those that make changes to their accounts and mandates on a regular basis. Companies that have simple account structures and mandates with signatories who rarely change will have less need for it, although the ability to generate reports on their account structures may be useful. Paper will remain an option for smaller organisations that do not manage numerous banking relationships. (See ‘Dispelling Some Myths’, below.)

If it sounds like eBAM would help your organisation, consider the following points when it comes to implementation:

Without doubt, eBAM is the future of bank account servicing. As with any technology, you should not embrace it simply because it has arrived, but as a result of consideration as to how it can be used to benefit your organisation.

If there is no benefit, then there should be no uptake. Many companies will take eBAM from some of their banking providers and not from others; plenty more won’t use it at all for now. Nevertheless, forward-thinking treasurers from organisations of all sizes should be talking to their banks about eBAM’s powerful long-term potential.

While eBAM will certainly benefit companies that use it regularly, it shouldn’t be seen as the absolute panacea for all your account-servicing woes. Here are some common myths surrounding eBAM as well as responses to them:

Don’t get caught up in the hype. If you don’t need to open and close accounts regularly, and your mandates don’t require constant revision, then you may not see much benefit.

That is certainly the long-term goal, but eBAM isn’t there yet. In the short term, banks’ differing back-office platforms and requirements will mean that they will still need their own specific documentation and information. In the longer term, the desire is to move towards a more industry-wide standard – similar to SWIFT messaging – but for now corporates will have to set up discreet eBAM systems with each of their banks.

Unfortunately not. The initial know your customer processes that you undertake with a bank will still need to be paper-based. Once these first accounts are open, however, you are free to use eBAM as much as you like.

Chris Jackson is head of cash management solutions for non-bank financial institutions at Barclays.