Today, you can book a cheap airline flight and a hotel room from the comfort of your home at midnight to fly away the next morning for a quiet weekend getaway with your family for Eid. This might have seemed impossible just 15 years ago, but by innovating in the way they produce and deliver their services, airlines have allowed the dream to become a profitable reality. Airlines know that they cannot rest on their past innovations, however; they need to continually think about what the next generation will expect of them in 15 years’ time.

Banks and financial institutions have a lot to learn about customer service from airlines, hotels and telecommunications companies. The same goes for innovation as well. While successful banking innovations include ATMs and internet banking, banks cannot afford to stand still.

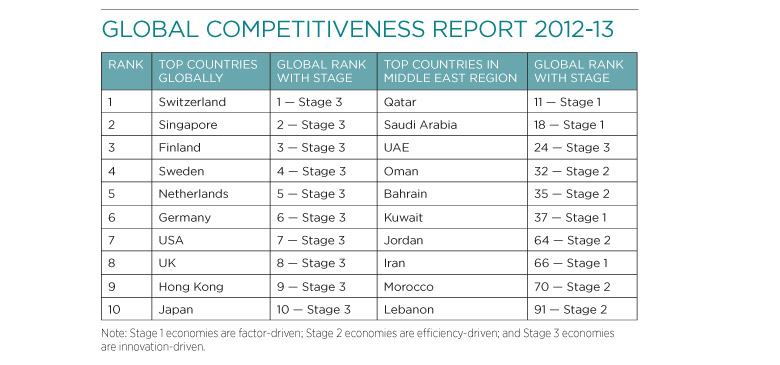

According to the World Economic Forum’s Global Competitiveness Report 2012-13, the United Arab Emirates (UAE) is the only country in the Middle East that can be classified as a Stage 3 (innovation-driven) economy, a classification it has enjoyed for seven consecutive years.

But although the UAE is an innovation-driven economy, a trend towards innovation in banking and financial services here is not as apparent as we might have expected for these reasons:

CEOs and general managers of banks in our region must keep their teams focused on being innovative, customer-driven and service-oriented while challenging them to do things differently. This will help to establish them as leaders in a rapidly changing marketplace where customer trust and loyalty are at an all-time low.

For some reason, many successful banks are imitated by their ‘me-too’ competitors. Banks that try to compete in a space where intense competition already exists can suffer because a strategy of matching and beating competitors tends to emphasise the same basic dimensions of competition. In their book, Blue Ocean Strategy: How to Create Uncontested Market Space and Make the Competition Irrelevant, W Chan Kim and Renée Mauborgne suggest the solution is to look for a market space that makes the competition irrelevant. The challenge is to introduce new dimensions into the market segmentation, positioning and targeting equation that other banks cannot immediately match.

In their eagerness to become all things to all customers, banks sometimes lose focus of what their definition of service is. In their seminal work, Market Leadership Strategies for Service Companies, Craig Terrill and Arthur Middlebrooks highlight this as the starting point on a journey to leadership.

Once the bank’s senior management has clearly articulated its definition of service and communicated this throughout the bank, innovation through precision targeting becomes a simple exercise:

For service organisations like banks to attract the ‘right’ customers, it is imperative that they realise service experiences are intangible and involve ‘manufacture’ and delivery happening simultaneously. In reality, there can be a large gap between what customers expect and what is actually delivered to them.

For the Middle East to claim its place as the financial centre of the world, banks and financial institutions need to become even more customer-centric and involve customers in the development of new products, services and channels that streamline processes for both the bank and its customers. They also need to create a service-oriented and empowered workforce. Banks that attract the ‘right’ customers can consistently delight them, which will translate into higher levels of customer loyalty and a more motivated team of employees.

Harshit Jain Cert ICM has more than 25 years’ global banking and commercial experience. He is the founding CEO of consultancy InnoVention Solutions. Email: hjn@eim.ae