China’s rise to become the world’s second-largest economy and the ensuing growth in demand for the renminbi are key drivers behind the tremendous expansion of China’s debt capital markets, both the onshore and the offshore renminbi bond markets.

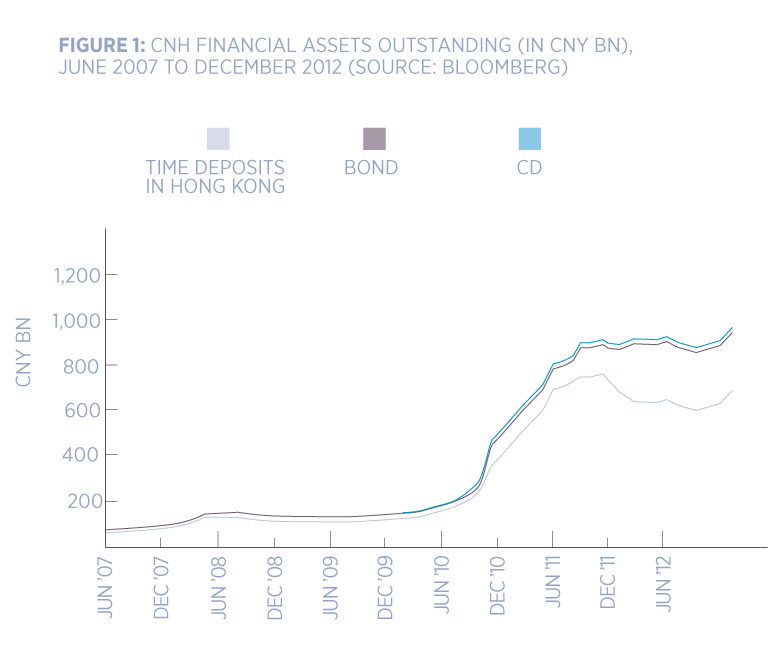

At the end of 2012, the size of China’s onshore renminbi bond market (the CNY bond market) had reached $3.8 trillion, according to the Asian Development Bank, with the corporate bond segment growing by 22% on an annual basis to $1.04 trillion of bonds outstanding. Similarly, the offshore renminbi bond market in Hong Kong (the CNH bond market) had grown to CNY 373bn of bonds outstanding by the end of 2012, according to Bloomberg, up by 66% on an annual basis.

The CNH bond market is the only market where investors can invest with meaningful scale in bonds issued by high-grade foreign entities

Different factors have contributed to the growth of the CNY and the CNH bond markets. While bank disintermediation drives the expansion of the CNY bond market, the desire to internationalise the renminbi and the need to have renminbi to settle trades are causing the CNH bond market to take off. Although the CNY remains a closed currency, making the CNY bond market difficult for global investors to access, the CNH bond market is open to most global investors and offers an attractive risk and return proposition to both investors and issuers.

The CNH bond market is unique in that it is the only market where investors can invest with meaningful scale in bonds issued by high-grade foreign entities such as Caterpillar, McDonald’s and HSBC, denominated in renminbi (see note below), in addition to being a market where investors can invest in bonds issued by various Chinese corporates and financial institutions. According to HSBC, 34% of new CNH bond issues in 2012 came from foreign entities.

Other characteristics of the CNH bond market are its high-grade and short-duration biases. Investment-grade issuers have undertaken significant issuances and most maturities fall within three years. The fact that investment grade-rated, major Chinese banks have been notable issuers of certificates of deposits (CDs) in the CNH market supports its high-grade bias. Difficulties in forecasting the trend in currency movements over the longer horizon is likely to be a reason behind the short duration bias of the CNH bond market.

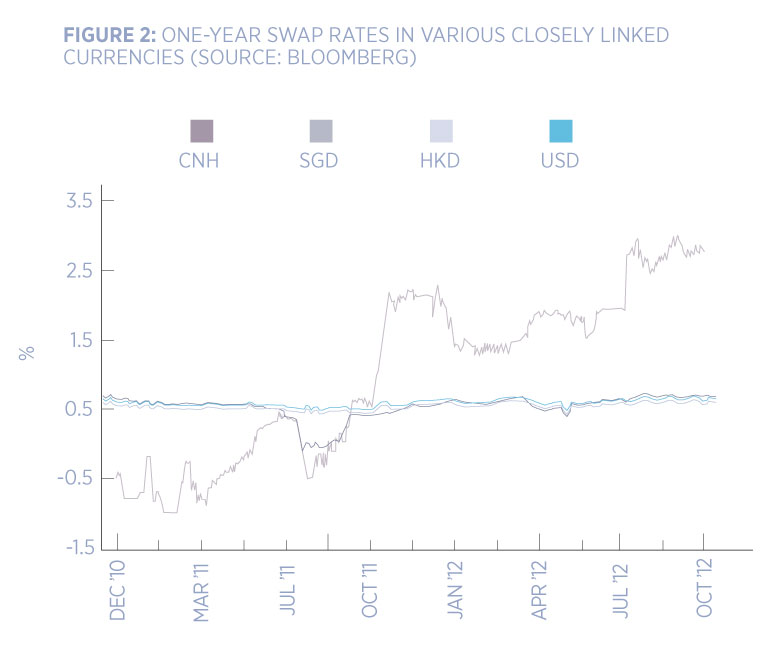

As the initial exuberance surrounding renminbi appreciation expectation fades, traditional credit and bond structure analysis takes a more prominent role in CNH bond investing. Significant bond and CD issues in the CNH bond market are not rated, despite being issued by rated organisations. Unlike the CNY bond market, where pricing of credit risk is still not as efficient and corporate CNY bond yields are more driven by government bond yields, the pricing of credit risk in the CNH bond market is more effective.

Whereas onshore banks and trust companies dominate the CNY debt market, the investor base for the CNH bond market is more diverse with institutional fund managers, banks and private bank investors playing significant roles. Geographically, the CNH bond market investor base is also quite diverse, with investors coming from Hong Kong, Singapore and Europe. Due to the CNH bond market’s still relatively small size, the market can be less liquid at times.

There are several reasons why we think the CNH bond market is attractive:

China’s economic growth bottomed out in 2012, but both domestic demand and exports should improve in 2013. Along with stabilising demand from developed countries, trade demand for renminbi will continue to grow, which will provide support for the currency. Given that offshore and onshore yield convergence has been broadly achieved, bond return is expected to be positive in 2013, driven by both currency appreciation and carry. At the same time, demand for higher-yield and longer-tenor bonds will increase in the current low-interest-rate environment, and credit quality will remain a critical consideration accordingly.

China’s economic growth bottomed out in 2012, but both domestic demand and exports should improve in 2013

We expect the robust development of the CNH bond market to continue in 2013. Chinese banks should remain active issuers in the CNH bond market due to lower offshore funding costs. Additionally, we expect issuance from a growing range of Chinese corporates as they look to capitalise on potentially lower offshore yields if onshore funding conditions become tighter. Issuances by foreign corporates could also grow on the back of increasing trade settlement in renminbi. Finally, we expect the Chinese and Hong Kong regulators to remain supportive of the CNH bond market growth and development – in line with the underlying themes of financial liberalisation and renminbi internationalisation.

Investing in the CNH bond market, if done properly, can enhance returns while not necessarily causing significant additional risks to be taken on. Products such as funds that invest only in high-grade credits with relatively short duration targets could be a suitable choice for investors that desire high-quality investments that offer good diversification and liquidity without being exposed to significant interest rate risk.

Note: Bank of America Merrill Lynch, Offshore renminbi bond market, Decent short-dated yield play, 24 January 2013

Theodorus Hadiwidjaja CFA is credit research analyst and Lan Wu is client portfolio manager at JPMorgan Asset Management, Hong Kong