Healthy businesses normally enjoy substantial cash inflows from their ongoing operations and sales receipts. In simple terms, the related cash inflow will be the adjusted operating profit.

For a growing business, a substantial use of cash will often be investment for further growth – for example, additional investment in net working capital for expansion.

When profitable companies expand too fast, they can run out of cash and liquidity and go bust. (This is known as ‘overtrading’.)

This essential understanding has recently been examined by asking you to: (1) calculate operating cash flow; or (2) prepare the statement for the net cash flow from operating activities; and (3) comment appropriately.

A company had the following results and activities for the year just ended. All amounts are in millions:

Operating profit: 50

Tax paid: 7

Operating profit is stated after charging depreciation and amortisation of: 2

Additional investment in net

working capital: 39

Calculate the net operating cash flow for the year and comment on your findings for the cash manager.

Our calculation of the net operating cash flow starts with the adjusted operating profit.

Our first adjustment to the operating profit before tax of 50 is to deduct the tax paid of 7. The business must pay the tax authorities promptly. (Or else the tax authority will quickly chase the business.)

Operating cash calculation (1)

Operating profit 50

LESS: (Tax paid) (7)

After tax 43

Operating profit has been stated after charging depreciation and amortisation of 2. But accounting depreciation and amortisation charges are not cash flows. So we need to add back the depreciation and amortisation, as non-cash items within the net operating profit.

Operating cash calculation (2)

Operating profit 50

LESS: (tax paid) (7)

After tax 43

Add back: depreciation

and amortisation 2

45

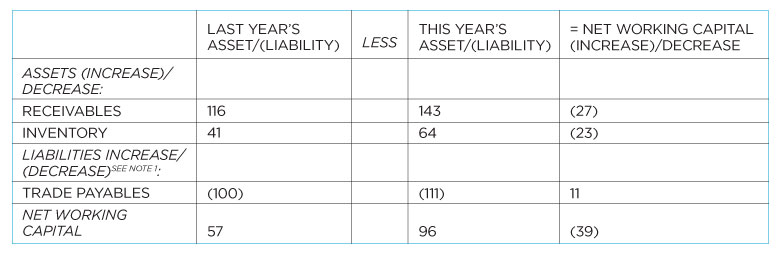

Our company has made an additional investment in net working capital of 39. This is a substantial use of cash. It reduces net cash flow, so it’s an important further deduction in calculating net operating cash flow.

Operating cash calculation (3)

Operating profit 50

LESS: (tax paid) (7)

After tax 43

Add back: depreciation

and amortisation 2

45

LESS: (increase in net

working capital) (39)

= Net operating cash flow 6

The cash manager will need to monitor the increase in net working capital. It has absorbed almost all of the positive operating cash flow for the year.

Net working capital is the total of current working assets LESS current working liabilities. Improved working capital management seeks to: (1) reduce current assets; or (2) increase current liabilities; or (3) both.

If either – or both – of these aims is achieved, then the amount of cash tied up in working capital will be correspondingly smaller. This can result in a smaller additional amount of cash being absorbed into working capital, or even a net release of cash from working capital.

Increases in current assets absorb cash. They mean we are tying up more cash by investing in current assets. This includes receivables and inventories.

In contrast, increases in current liabilities RELEASE cash. They mean we are enjoying more credit from suppliers and others. This includes trade payables and non-trade payables. We will still have to pay all our liabilities, of course. But we can pay them later, rather than now. So, in the meantime, we have more cash in our bank account, and improved operating cash flow.

We need to be careful to get our plus and minus signs the right way round here. It’s a big help to invest time in: (1) tabulating; and (2) row and column labels with explicit sign conventions.

See the table, below, which is based on the October 2010 CertICM exam. This is the more detailed calculation of the net 39m cash outflow that we saw earlier (see note 2).

Certain important cash flows aren’t generally considered to be ‘operating’ cash flows. Non-operating cash flows include investing and financing. So don’t include investing or financing items in your calculation of operating cash flows.

Examples of investing and financing items (to exclude from operating cash flow calculations) would be buying or selling tangible fixed assets, and issuing or redeeming bonds.

“Operating cash flow is a good example. Very few had this entirely right and many skipped it altogether.” CertICM Examiner’s Report, October 2012

“Many missed out this question and some mixed operating cash flow with cash flow. In addition, examinees were asked to comment on their result and this part of the question was often forgotten.” CertICM Examiner’s Report, October 2010

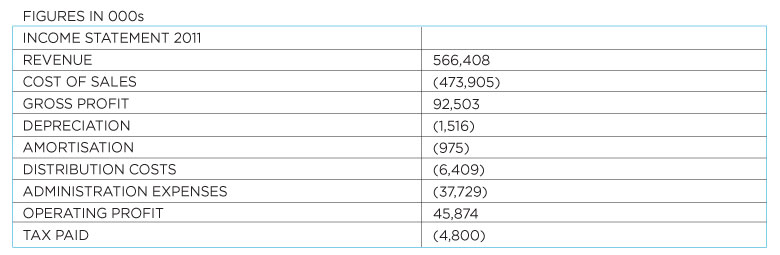

The following example is based heavily on the October 2012 CertICM paper. Work through the 10 easy steps in turn to calculate the operating cash flow for the year.

You have the following information on Tasman Seas plc.

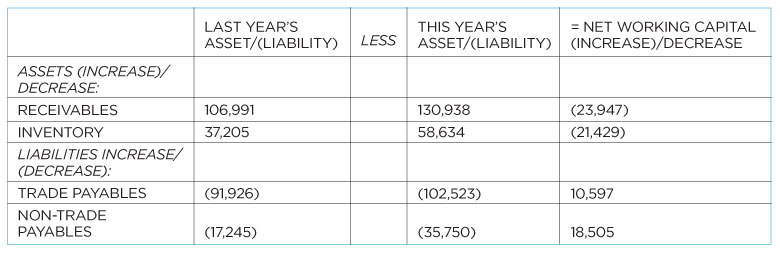

Changes in current assets:

Changes in current liabilities:

The requirement in the exam stated: “From the information above, calculate the operating cash flow produced in 2011.” This simply required following the 10 short steps noted above.

Operating profit 45,874

(LESS): Tax paid (4,800)

After tax 41,074

Add back: depreciation 1,516

Add back: amortisation 975

Subtotal below 43,565

You will score full marks if you reproduce this calculation and supply comments.

Note 1: Notice that for changes in liabilities, this adjustment is the opposite way round, compared with the adjustment for changes in assets.

Note 2: Figures have been rounded for easier reading.

Download the previous articles from this series and other useful study information from the exam tips area of the ACT student site at study.treasurers.org/examtips

Note 1: Notice that for changes in liabilities, this adjustment is the opposite way round, compared with the adjustment for changes in assets. Note 2: Figures have been rounded for easier reading.

Doug Williamson FCT is an examiner, tutor and exam scrutineer for six ACT exam courses