Until recently, concerns around the viability of Bitcoin as an investment have been plentiful. Is it really a store of value given the historical and inherent volatility? How well can investors secure and store the physical Bitcoin? Is there enough market liquidity? Are regulators going to stifle adoption? But the industry has been quietly addressing these fundamental issues over the past few years: there is now a strong case for a small allocation to crypto in institutional portfolios.

Since the end of 2017, when Bitcoin peaked at just under $20,000, the cryptocurrency’s volatility has declined. Average 30-day rolling volatility is set to hit a four-year low since global markets rallied behind the boom of Bitcoin in 2017. Peaks in volatility continue to decline, too. Looking at returns on a monthly or quarterly basis makes for an even stronger argument about the cryptocurrency’s resilience.

Since 2018, institutional investors have had more ways to access Bitcoin products, such as Grayscale’s Bitcoin Trust, CME & CBOE Futures, Nasdaq-listed CoinShares and Swiss-listed Amun ETP, among many other digital asset management firms.

The combination of these factors has prompted institutional investors to step into the crypto space. Tech companies MicroStrategy and Square have added $475m and $50m Bitcoin respectively for their treasury portfolios, with MicroStrategy planning further allocations. Insurance behemoth MassMutual announced earlier this month that it has bought $100m Bitcoin for its general investment portfolio.

The time has come for corporate treasurers to learn more about this fast-evolving global asset class.

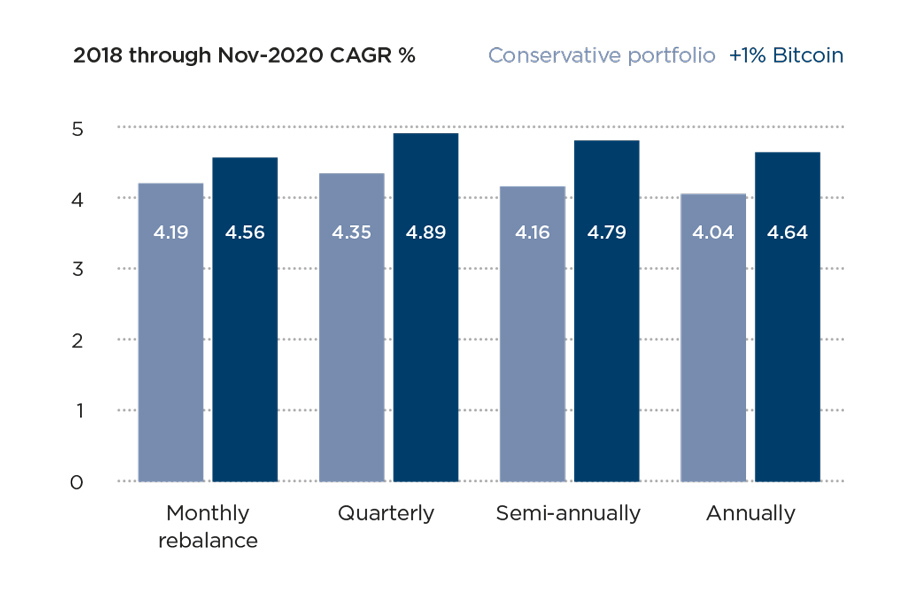

The year 2018 was a bear market. Despite this fact, the cryptocurrency has earned its badges, with a strong comeback since it bottomed in 2019. A diversified portfolio (70% fixed income, 10% cash, 10% equities, 5% commodities and 5% gold) would have fared better by allocating just 1% to Bitcoin instead of cash since 2018 through till the end of November this year (see chart).

Crucially, Bitcoin market trading has also grown exponentially across the board. Spot markets, derivatives and institutional products have all seen a meteoric rise over the past few years alone, with demand showing little sign of abating.

Cash-settled CME Bitcoin futures now account for a whopping 15% of global markets alone, according to data platform Skew. And if that isn’t enough to highlight the interest, this is in fact a 150% growth in 2020 alone.

Month-on-month trading volume growth has been remarkable across the three main options currently available – CME, Bakkt and Grayscale’s Bitcoin Trust. And Open Interest has grown exponentially stronger along with it.

The regulatory environment is also turning more positive. Policymakers are increasingly bringing cryptoassets inside of the regulatory perimeter. The European Commission issued a proposed regulation for the issuance and provision of services related to cryptoassets earlier this year. In the US, the Office of the Comptroller of the Currency has said that banks can now provide custody and banking services for crypto businesses. Similar moves are being made by regulators around the world.

Like any nascent industry, the crypto industry faced immense challenges in its formative stages. But the market has matured. It is increasingly being viewed as a legitimate institutional-grade asset class. It is time for corporate treasurers to take a closer look.

Ralph Payne is CFO of Copper.co

An ACT webinar, sponsored by Copper.co, Understanding the crypto asset market, will take place on 20 January 2021. The webinar will be free to access, and details will be published here shortly: treasurers.org/events