Background

The Policy and Technical team continues to speak with treasurers to understand what issues they are facing and in what areas the ACT can help. We are also talking with the main banks to understand how they are responding to the COVID-19 crisis. At the same time, we have held a number of conversations with HM Treasury, the Bank of England, the CBI, the City of London Corporation and UK Finance. Through these forums we have been able to ensure that the views of the treasury community are heard by policymakers through a number of different channels.

A list of useful material from the ACT, the Regulators, the Government and Others can be accessed from the ACT Knowledge Hub - https://www.treasurers.org/hub/technical/covid19

HM Treasury update – 2 November

The deadline for applying to the CLBILS, CBILS and Bounce Back schemes has been extended to 31 January 2021. Firms that have already applied to for Bounce Back loans will be able to top up their existing loans, though this can only be done once.

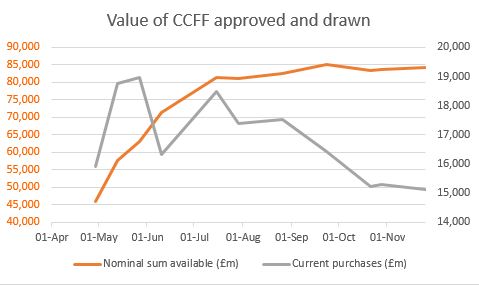

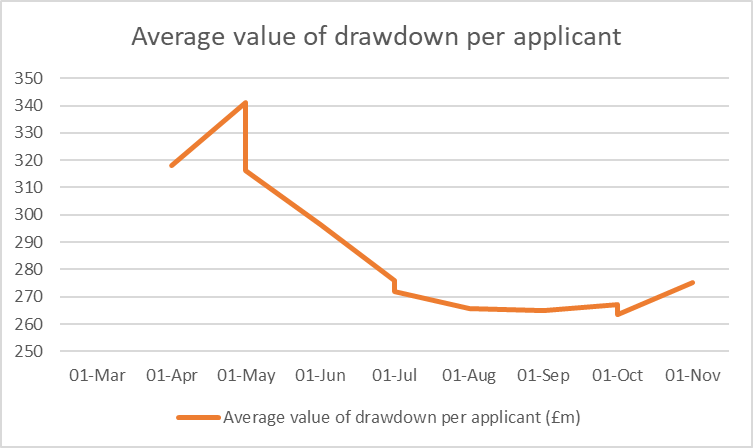

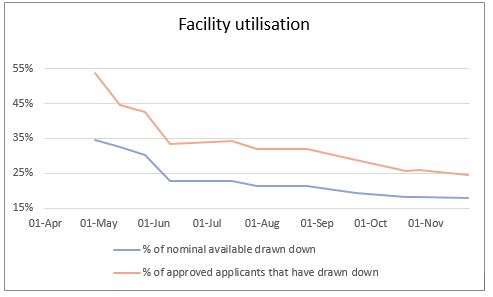

The CCFF scheme

Taken from the Bank of England report, the following table provides some interesting insights (https://www.bankofengland.co.uk/markets/bank-of-england-market-operations-guide/results-and-usage-data

As the graphs above confirm CCFF usage has fallen to its lowest level in 6 months.

Details of current borrowers under the facility can be found at https://www.bankofengland.co.uk/-/media/boe/files/markets/covid-corporate-financing-facility/cp-held-by-ccff-by-business.xlsx.

More information on the programme can be found under https://www.bankofengland.co.uk/markets/covid-corporate-financing-facility.

If you have questions you’d like raised with the Bank of England, please email technical@treasurers.org

We are starting to hear from firms that have been able to access the CCFF programme; we provide anonymised feedback to the Bank of England. If you’d like to share your experiences, please drop an email to technical@treasurers.org.

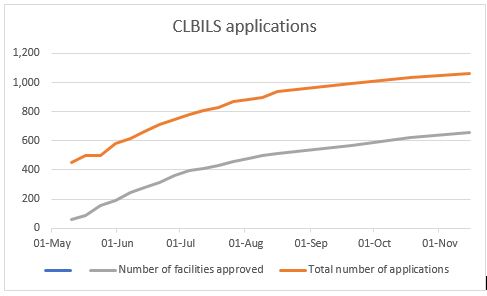

Other Schemes

On September 24, the Chancellor of the Exchequer extended the government’s three Coronavirus business interruption loan schemes and the Future Fund. The extension aligned all the end dates of the schemes to 30 November.

In addition, it was announced on September 25 that businesses applying for the CBILS or CLBILS will benefit from more flexibility on the date the test of whether or not their business is an ‘undertaking in difficulty’ is assessed.

New figures show that the Government paid £135.8 million to lenders for providing billions of pounds to support UK businesses between April and June as part of the Coronavirus Business Interruption Loan Scheme (CBILS) and the Bounce Back Loan Scheme.

It was also revealed that the Government paid around £39.2 million in arrangement fees for the banks to provide CBILS. These fees have not been charged on bounce back loans.

The Government promised to cover the interest on both schemes for the first year after the loans were taken, to help take pressure off the companies.

The interest is paid in quarterly instalments, so the figure only covers the first three months of the schemes being in place.

The bounce back loans have a flat 2.5% interest rates, while CBILS can charge anything up to 14.9%. The average for all CBILS loans is 5.1%.

The Bank has also made available details of the other schemes being made available (https://www.gov.uk/government/collections/hm-treasury-coronavirus-covid-19-business-loan-scheme-statistics#Coronavirus-Business-Interruption-Loan-Scheme ).

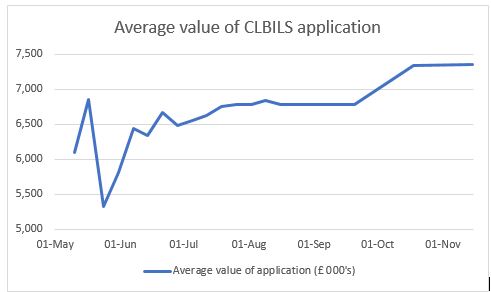

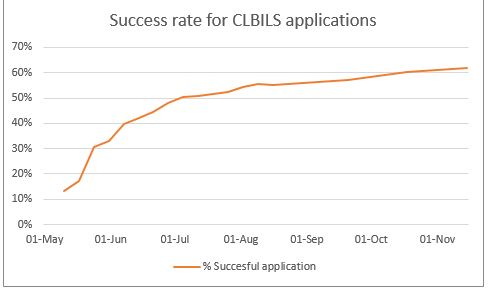

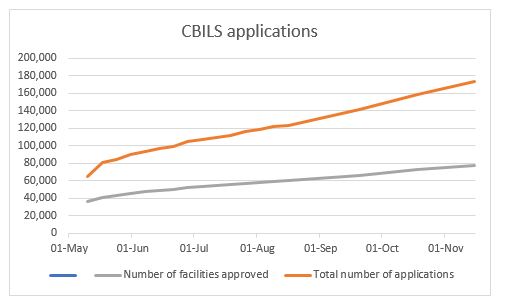

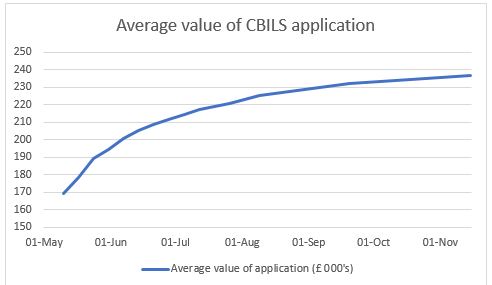

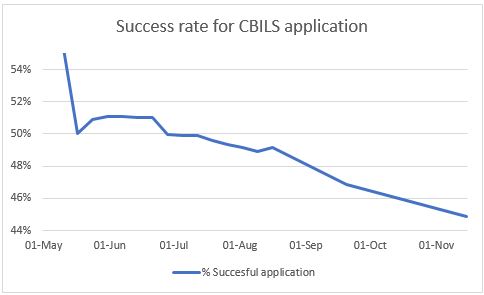

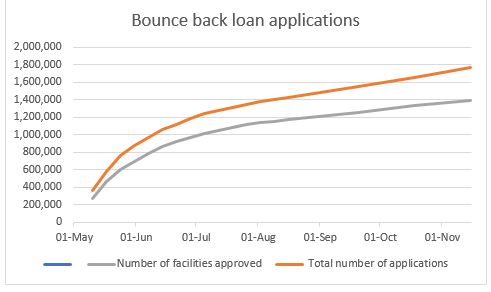

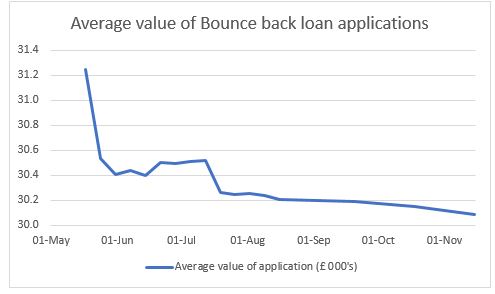

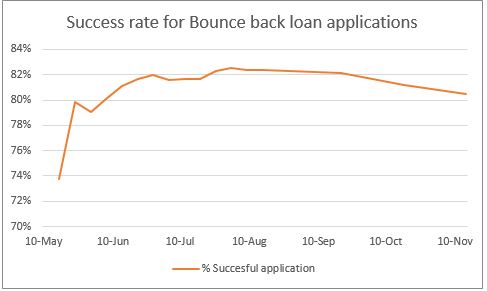

The data shows that:

The British Business Bank has started to release details of the take up of the schemes it administers split by:

Update from the UK regulators

The ONS produces a fortnightly analysis of business responses in a number of key areas. The latest report noted:

It should be noted that the survey population tends to be small businesses.

Feedback from Treasurers

The slight decrease in the number of active borrowers under the CCFF scheme reflects comments we have heard from treasurers who have reported repaying government loans and, in some cases, repaying furlough related payments they received.

Views from across the world

As a member of the International Group of Treasury Associations, and the European Association of Corporate Treasurers and working with our colleagues in the US National Association of Corporate Treasurers we are keeping an eye on developments overseas.

In a recent survey by YouGov

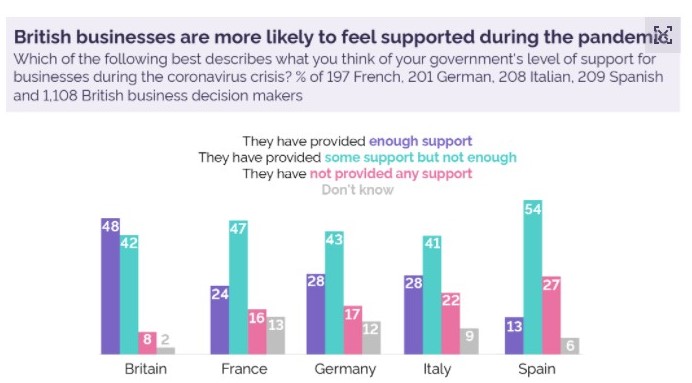

About half of businesses in Britain (48%) felt adequately supported - this is significantly higher than in Germany (28%), Italy (28%), France (24%) and Spain (13%).

In contrast, a quarter of Spanish businesses (27%) said the government had not provided any support. This sentiment is also more common in Italy (22%), Germany (17%) and France (16%) compared with Britain (8%).

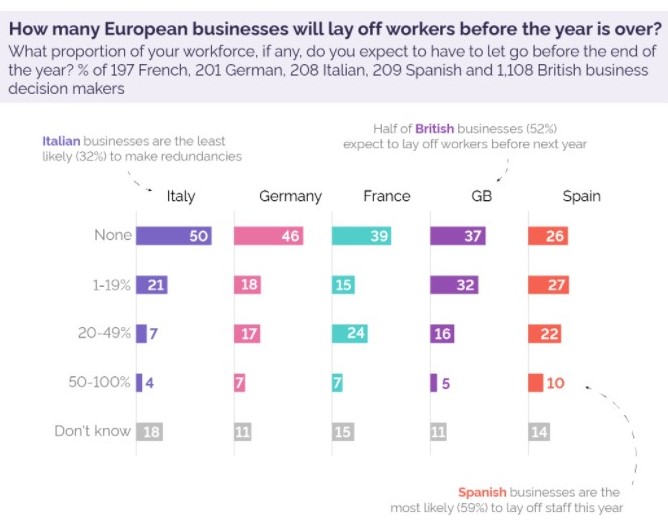

Half of British businesses surveyed (52%) were expecting to make redundancies before the end of the year when polled in the last week of September. This figure is only dwarfed by Spain where three in five businesses (59%) believed they would have to lay off employees before the new year – including one in ten (10%) expecting to let half of their workforce or more go.

Italian businesses were the least likely to expect redundancies, however a third (32%) still assumed there would be some more layoffs this year.

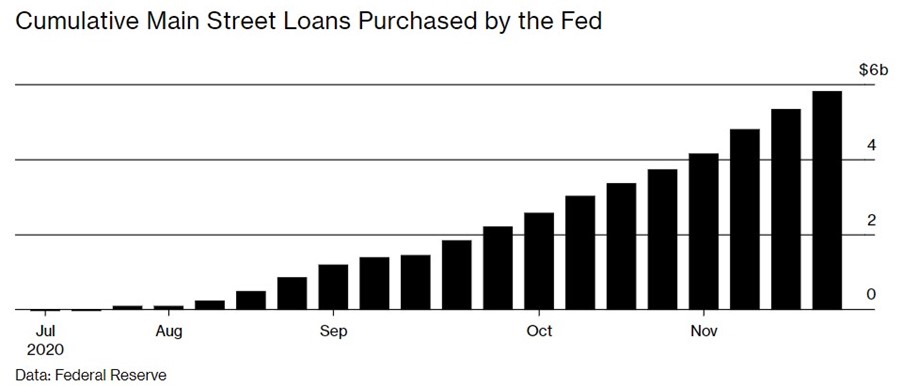

The US Treasury Secretary, Steven Mnuchin announced on Nov.19 that he wouldn’t approve an extension of the Main Street Lending Program programme, along with four other emergency lending facilities, past Dec. 31. This follows an assessment that the $6bn it had lent since April was not working as had hoped as a result of legal restrictions on the Fed’s emergency powers and the risk aversion of banks the program relied on to make loans.

Engaging with the treasury community

We welcome conversations with our members on:

Send an email to technical@treasurers.org and either James Winterton, Naresh Aggarwal or Sarah Boyce will be in touch with you.

If you have found any resources which you feel we should add to our COVID-19 site, please email us with details.

Naresh