Background

The Policy and Technical team continues to speak with treasurers to understand what issues they are facing and in what areas the ACT can help. We are also talking with the main banks to understand how they are responding to the COVID-19 crisis. At the same time, we have held a number of conversations with HM Treasury, the Bank of England, the CBI, the City of London Corporation and UK Finance. Through these forums we have been able to ensure that the views of the treasury community are heard by policymakers through a number of different channels.

A list of useful material from the ACT, the Regulators, the Government and Others can be accessed from the ACT Knowledge Hub - https://www.treasurers.org/hub/technical/covid19

HM Treasury update

The deadline for applying to the CLBILS, CBILS and Bounce Back schemes has been extended to 31 March 2021 from 31 January. As noted previously, firms that have already applied for Bounce Back loans will be able to top up their existing loans, though this can only be done once.

More support will be available beyond March, through a successor loan scheme. Details of the scheme will be announced in due course, with the government providing a further update on wider COVID-19 economic support at the Budget on 3 March 2021.

The CJRS furlough scheme has been extended until the end of April 2021 with the government continuing to contribute 80% towards wages.

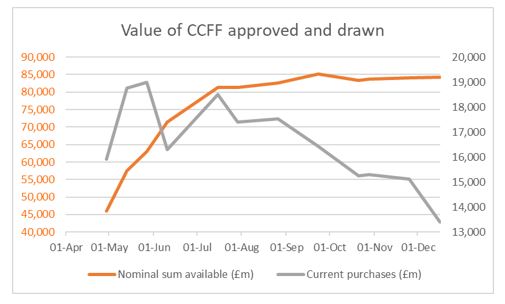

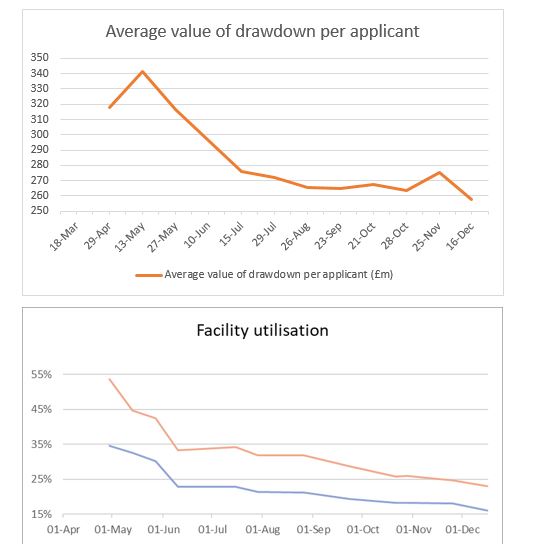

The CCFF scheme

Taken from the Bank of England report, the following table provides some interesting insights (https://www.bankofengland.co.uk/markets/bank-of-england-market-operations-guide/results-and-usage-data).

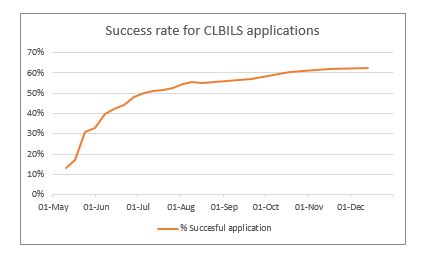

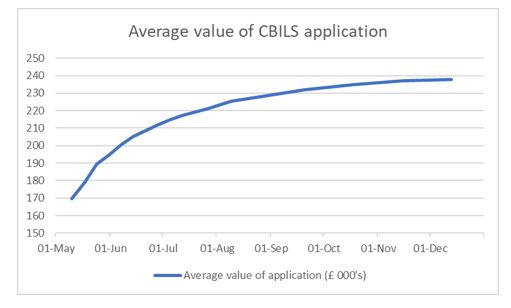

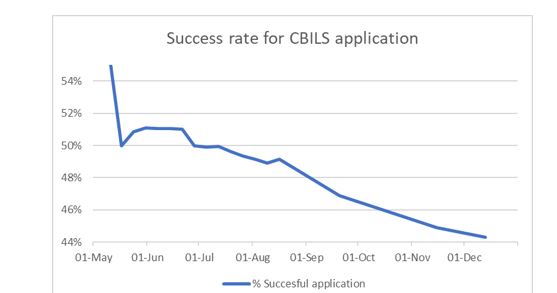

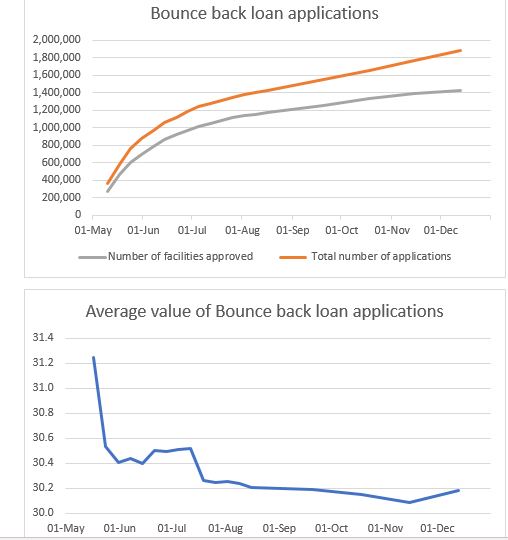

As the graphs above show:

This confirms our conversations with treasurers that many are using their CCFF facility as a back-up programme and also many have been repaying debts ahead of a key reporting period.

Details of current borrowers under the facility can be found at https://www.bankofengland.co.uk/-/media/boe/files/markets/covid-corporate-financing-facility/cp-held-by-ccff-by-business.xlsx.

More information on the programme can be found under https://www.bankofengland.co.uk/markets/covid-corporate-financing-facility.

If you have questions you’d like raised with the Bank of England, please email technical@treasurers.org

We are starting to hear from firms that have been able to access the CCFF programme; we provide anonymised feedback to the Bank of England. If you’d like to share your experiences, please drop an email to technical@treasurers.org.

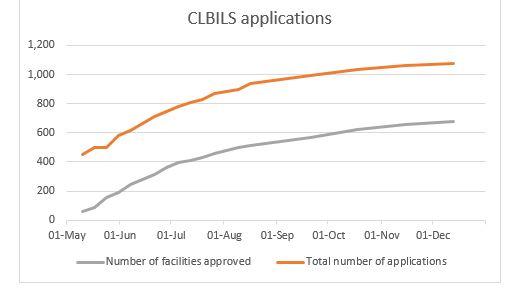

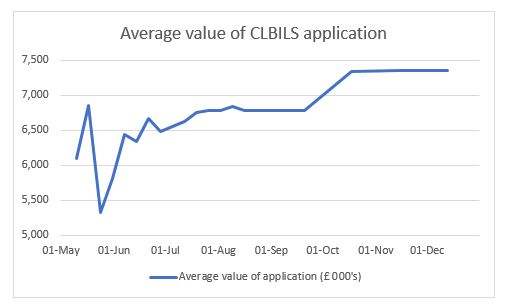

Other Schemes

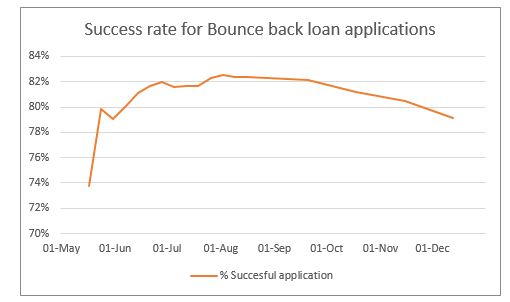

Bounce back loans charge a flat 2.5% interest rates, while CBILS can charge anything up to 14.9%. The average rate for all CBILS loans is 5.1%.

The Bank has also made available details of the other schemes being made available (https://www.gov.uk/government/collections/hm-treasury-coronavirus-covid-19-business-loan-scheme-statistics#Coronavirus-Business-Interruption-Loan-Scheme ).

The data shows that:

The British Business Bank has started to release details of the take up of the schemes it administers split by:

Update from the UK regulators

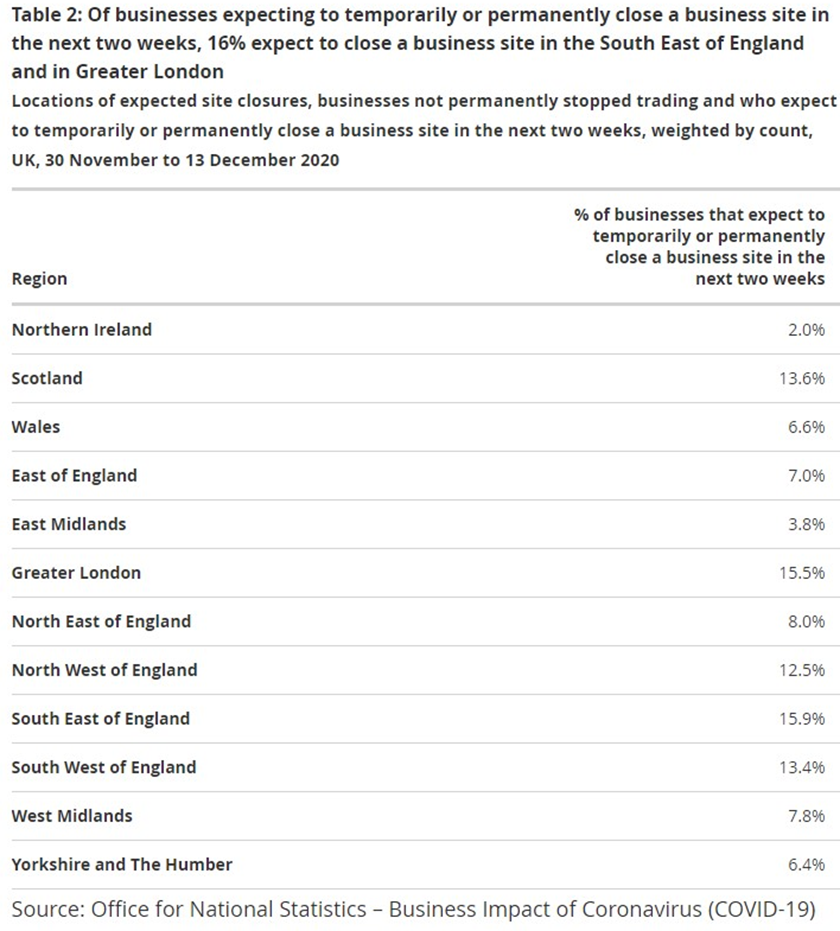

The ONS produces a fortnightly analysis of business responses in a number of key areas. The latest report noted:

Cash reserves:

Trading activity:

Working conditions:

It should be noted that the survey population tends to be small businesses.

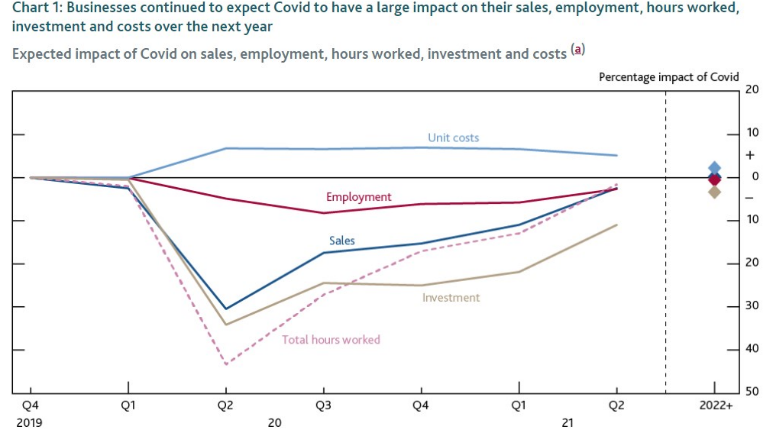

In a survey of Chief Financial Officers from small, medium and large UK businesses, the Decision Maker Panel (DMP) recently provided results on the impact of COVID-19 up until November 2020. Key messages include:

In the November survey, only a modest recovery in sales was expected in 2020 Q4, where sales were expected to be 15% lower than they would have been. However, further improvement was expected in the first half of 2021, such that sales were only expected to be around 2% lower by 2021 Q2. Investment was also expected to recover, but more slowly and by less than sales.

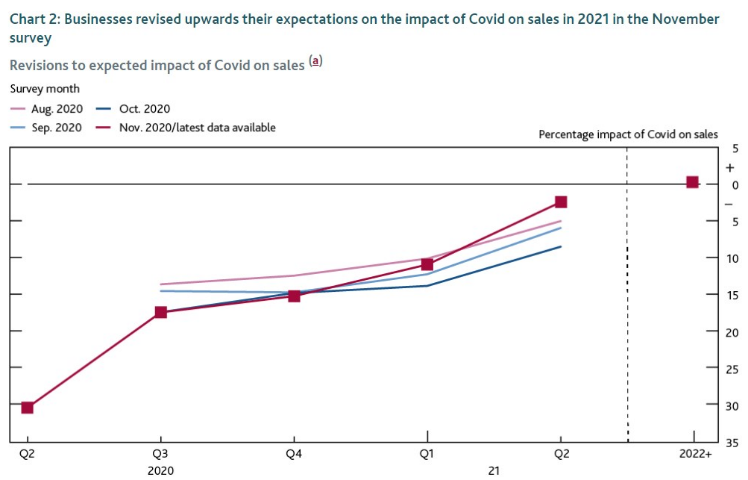

While near-term expectations on the impact of COVID-19 on sales were broadly unchanged relative to previous months, expectations for the first half of 2021 were revised up. The largest revision, relative to the October survey, was for 2021 Q2 at 6 percentage points. That may reflect the announcement about vaccines during the survey window from Pfizer and Moderna. The Oxford-AstraZeneca vaccine news came after the survey window had closed.

Feedback from Treasurers

The slight decrease in the number of active borrowers under the CCFF scheme reflects comments we have heard from treasurers who have reported repaying government loans and, in some cases, repaying furlough related payments they received.

Views from across the world

As a member of the International Group of Treasury Associations, and the European Association of Corporate Treasurers and working with our colleagues in the US National Association of Corporate Treasurers we are keeping an eye on developments overseas.

The US Treasury Secretary, Steven Mnuchin announced on Nov. 19 that he wouldn’t approve an extension of the Main Street Lending Program programme, along with four other emergency lending facilities, past Dec. 31. This follows an assessment that the $6bn it had lent since April was not working as had hoped as a result of legal restrictions on the Fed’s emergency powers and the risk aversion of banks the program relied on to make loans. There have been no announcements yet of any replacement programmes following a small extension of the programme to manage an influx of late applications.

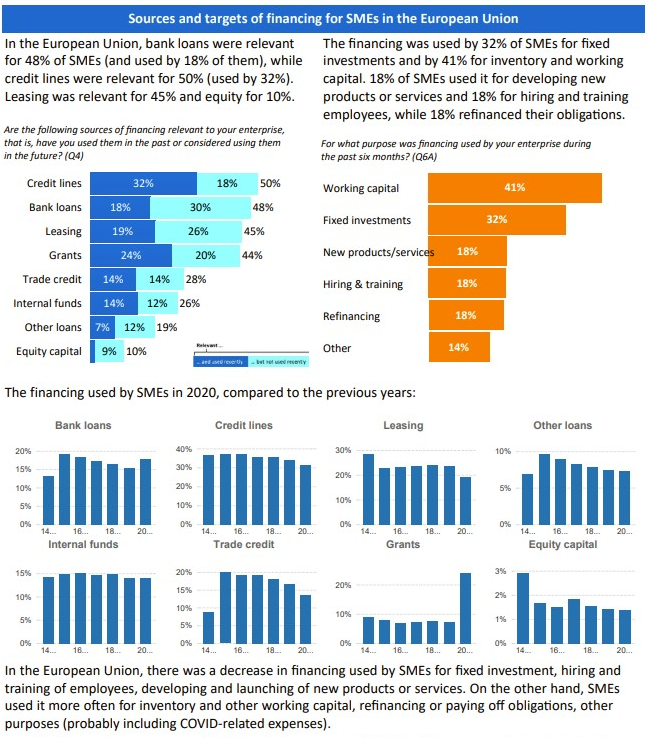

The European Commission undertook a 112-page review of access to finance by SMEs across the EU. This includes the following infographic:

Engaging with the treasury community

We welcome conversations with our members on:

Send an email to technical@treasurers.org and either James Winterton, Naresh Aggarwal or Sarah Boyce will be in touch with you.

If you have found any resources which you feel we should add to our COVID-19 site, please email us with details.

Naresh