Cash management is often seen as a tactical matter within a corporate. It is about bank accounts and how funds flow. We want to save on bank charges and optimise the use of cash. Cash management is about oiling the wheels of banking operations.

I would argue that such a myopic approach to cash management reduces the discussion to its visible, day-to-day, transactional aspect. Very often what is needed is not visibly obvious. A bigger picture presents itself once we ask the following questions:

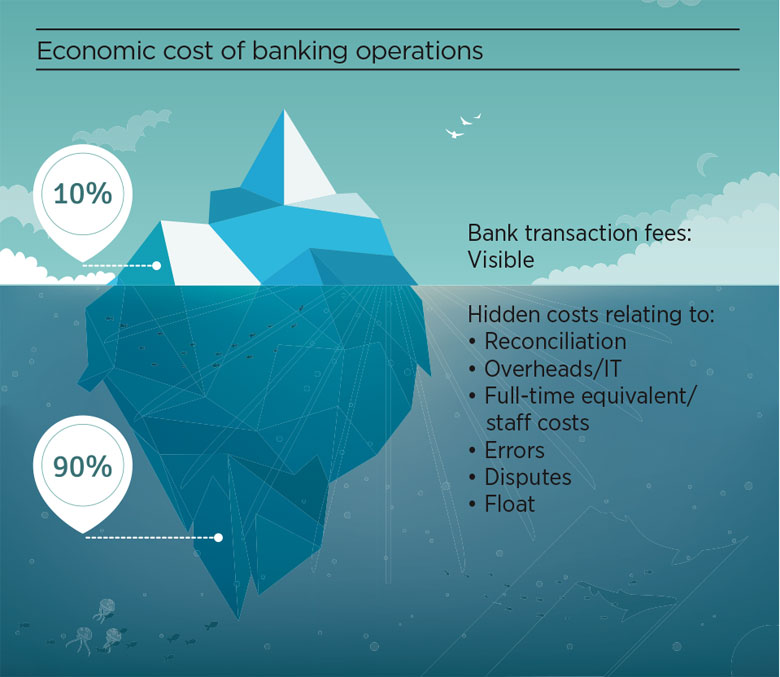

In summary, there is more to consider when judging cash management holistically than the movement of cash. What is highly visible is not necessarily what really matters.

At times, the cash management projects I have seen are too focused on payment and pooling mechanics, and direct cost. Such an approach leads to an auction of one’s banking business, with the deal being awarded to the lowest bidder. The true economic cost, however, is made up of several components, including some indirect factors that will nevertheless lead to very direct cost.

Fewer banks and accounts lead to fewer internal funds transfers, fewer errors and less float

Consider the IT impact – connecting the corporate to a bank is costly, driven by complexity as much as volume. With the transaction volume taken as a given, the treasurer wants to focus on reducing complexity by reducing the total number of banks, bank accounts and electronic banking platforms that need to be supported. Fewer banks and accounts lead to fewer internal funds transfers, fewer errors and less float. Consider the cost of managing exceptions – every operational issue requires a disproportionate amount of time and effort, and sometimes cost, to rectify, so reducing the frequency of errors through simple and streamlined operations saves money in the long term.

So far, there is an argument for using close relationship banks for cash management in general, and for consolidating banking transactions into fewer banks. The question now is, how global, local or regional our cash management organisation should be.

Where do we strike the balance between the synergies to be gained from the one-stop shop of a global banking partner, and the flexibility and domestic competitiveness of a local bank?

At Willis, we have found that regional banking relationships offer the best solution all round.

Willis’s approach is more consultative than scientific, and it takes time to arrive at the right conclusion. It starts by building support within the organisation to undertake a regional banking project, and communicate our philosophy. With leadership from treasury, support from management and genuine buy-in from the business, we kick off the project.

We turn to our core relationship banks first. We identify those that have the right capabilities in the respective region and start a dialogue with them, possibly adding a challenger from outside our core banks. The project starts with an initial overview of our business and its needs in the region, typically through a combination of meetings and phone or videoconferences. Working groups are formed, people connect.

Regional banking platforms combine the synergies from centralisation and consolidation with local banking to suit our individual businesses’ needs

In building the request for proposal (RFP) we take a broad view of what we expect to gain from the project, focusing on service and innovation, and allowing the banks to make suggestions on how our operations could improve. The RFP itself is more concise than scientific, and we look for personal dialogue more than detail. Our banks are our partners, with whom we embark on a journey known as a regional banking project.

To conclude, we develop a decision matrix where every stakeholder in the business rates each bidding bank on a variety of aspects, in addition to a cost analysis. The decision is made through a vote from the business, not including treasury. That practice sometimes comes as a surprise, but is important to me as it demonstrates treasury’s role as a business partner and adviser. The ultimate decision remains with the business. Our experience shows that the business is genuinely committed and supportive where its own choice is being adopted.

In my view, the qualitative benefits obtained through taking this approach are worth more than any small, potential savings on bank charges. Our – and our clients’ – money is held within banks that we consider financially and operationally robust. Electronic banking platforms are being set up within corporate guidelines. The bank account documentation that has been put in place was centrally negotiated and is coherently implemented. Links to our treasury management system have been built, creating high visibility of cash. Local businesses can rely on support from treasury in dealing with our regional partner banks. Our SWIFT connectivity, which is live in the US, could be rolled out to the regions where we use the same banks.

We completed a regional banking project in Asia-Pacific with JPMorgan in 2011/12 that has stood the test of time and continues to deliver benefits. Today, it offers a ready-made structure for Willis to on-board a newly acquired company. We recently tapped Citibank to be our Latin America partner. Its global footprint allows each local market to roll seamlessly into client-defined regional structures.

Cash management is not a technical service provided by the cheapest bidder. It is an element of the finance supply chain, to be considered as such, with additional risk and relationship considerations. Willis’s experience shows that regional banking platforms combine the synergies from centralisation and consolidation with local banking to suit our individual businesses’ needs.

Christof Nelischer is global group treasurer at Willis Group, based in London