Socially responsible investment has some pretty heavyweight origins – for example, the work and investment portfolios of the great Victorian industrialists, plus the ideas of venture capitalists led by Sir Ronald Cohen, founder of Apax Partners and the British Venture Capital Association.

Yet for more than a decade, social investment – as it is sometimes known – has not flashed up on the radar of many corporate treasurers or investment managers. This is despite many potential benefits: in particular, balancing investment and positively profiling the investor.

But is this a door to a new world for corporate treasurers, or a box of mixed blessings best left to a risk-taking Pandora?

Perhaps it is an area most relevant to fund and investment managers – but are there any lessons to be learnt for the corporate, especially where they manage a significant long-term investment portfolio?

Many of this middle range seeks backers for fixed and working capital, and can pay returns on it

Social enterprise generally refers to programmes, organisations and projects focused on delivering improvement in the lives of individuals, families and communities.

These may be as diverse as employment, children and youth interventions, ranging from the general, such as National Citizens Service or the Duke of Edinburgh’s Award scheme, to the intense, such as The Children’s Society’s work, with children at risk of sexual exploitation.

They may also include programmes to combat domestic violence and workplace stress or improve physical activity and community health.

The European Commission expert advisory group on social business (Groupe d’experts de la Commission sur l’entrepreneuriat social or GECES) has developed standards for impact measurement that are now a part of secondary legislation.

These standards define ‘social’ as ‘relating to individuals and communities, and the interaction between them; contrasted with economic and environmental’. Investment takes the familiar definition of funds injected by loan or equity for a financial return.

So, combining the two brings us to social investment: investing in organisations or programmes, the prime or main focus of which is to bring about social change or improvement for individuals, families or communities.

Since the investment requires a return and a repayment of capital at some stage, the services have to be delivered to an enterprise model; that is, they have to make money to fund the return on capital.

This sounds like a very new area for investment, but does it represent real opportunity, and where does it sit between charity and the private sector?

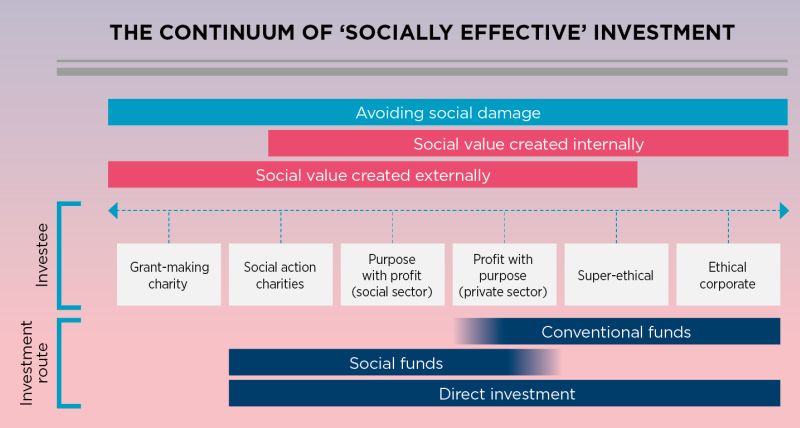

The Social Impact Investment Taskforce, formed by the G8, recognised that as ethical investment stretches its boundaries to not just avoiding harm, but actively delivering social value, and as the charity sector develops from the grant-giving and direct delivery charities into more enterprise models, the two meet and form a continuum.

In the middle are privately owned companies with a primary social purpose (‘profit with purpose’, such as those delivering public services like Core Assets) and social-sector organisations working with an enterprise model (‘purpose with profit’, such as the HCT Group).

Many of this middle range seeks backers for fixed and working capital, and can pay returns on it.

A recent EU publication, Social Enterprises and the Social Economy Going Forward, noted that the social economy represents 8-10% of GDP across the EU. The ‘purpose with profit’ and social delivery organisations it identified include a large number of SMEs, but also some substantial organisations and networks with turnovers above £100m.

This is, by most standards, a substantial area of economic activity and investment opportunity. While the rate of investment into the social-sector element of these is perhaps a little behind the 2012 Boston Capital Group projection that suggested demand of £1bn per annum in the UK alone by 2016, this sector is growing and developing beyond the housing bonds that have been with us for many years.

In terms of structure, the investments follow many of the commercial sector models: debt (secured, senior and unsecured, junior types), equity, and for charities and others who cannot issue shares, debt instruments that behave like equity.

These may be directly invested in the borrower, or its delivery (trading) vehicle, or indirectly through collective investment pools or managed funds. The latter, like their commercial sector equivalents, present different focal purposes (for example, health or children), and different risk profiles based on the instruments in which they will invest, and the degree of portfolio diversification.

As shown by the dark-blue bands in the diagram, where conventional funds invest mostly in the conventional (even if they are starting to move towards the socially focused), the specialist social funds are starting with charities and ‘purpose with profit’, and stretching towards the private sector.

Direct investments, of course, span the whole range.

Investors are typically approached either directly (often in association with an existing business association or for off-market placements through intermediaries or brokers specialising in placing social instruments), or through brokers placing listed instruments.

Listings may be on any of the main markets, or one of the newly emerging specialist provisions. Two of these that seem to offer considerable promise are the Social Stock Exchange (linked to ICAP-ISDX, and offering issues that are certified as having a social impact, as well as offering a largely bond-like investment profile) and the Allia-coordinated issues onto the Retail Bond Market as retail charity bonds (such as the issues by Golden Lane Housing for purchase of specialist housing stock).

As an alternative, investors may prefer to invest through managed funds operated by those offering specialist focus, such as Bridges Ventures, Social Finance UK, FSE CIC or Social and Sustainable Capital. These tend to be five- to seven-year funds, as against the listed bonds that often mature at 10 years or slightly more.

Some liquidity may be offered in these as between fund investors, matching to a degree the opportunity to resell on the market for the listed bonds.

A further alternative used by some who wish to commit funds to this, but do not want to co-invest up front, is to follow, and co-invest with, an existing investor or fund focused on this area.

This typically is either on the basis of a pre-commitment to match pound for pound or similar, or as a club member, in which you are notified of opportunities, and decide piecemeal as you go whether to co-invest and in what proportion.

As an investor, there are probably two broad approaches: to carve off a fixed element of the whole fund holding and apply it semi-permanently to these markets, or to make a more flexible and liquid arrangement, allowing you to move in and out of relevant investments.

The second is harder to achieve at present, other than by working with a fund manager or broker to help you to do so, or in connection with a more liquid holding, such as listed bonds.

Another possibility would be providing shorter-term capital funding for large social ventures in a partnering arrangement. The market, however, is improving all the time, so all of these are worth considering.

There are four main reasons why this is an area of interest. The first is the investment opportunity itself. With a developing market of sound investment prospects with yields, many of which meet market norms, and a substantial part of the economy in this arena, why ignore the opportunity?

To embrace this brings a chance to say something positive about the organisation and its values. It is both pro-social, caring and forward-thinking. The third area is in balancing risk.

With so much of the economy in this arena, and with it responding to different economic risks, it arguably enables the investor to get a greater spread of risk across the portfolio.

This, of course, depends on the investments chosen in this area, and how they are themselves balanced and managed – but the principle is clear.

Finally, it enables an investor, corporate or otherwise to generate and, if it wants, to take some credit for, creating positive social change with its money at the same time as maintaining reasonable investment yields.

In times when consumers, customers, staff and other stakeholders are often looking at a corporate’s values as a driver of their loyalty to it, this could be a significant positive move.

If this sounds interesting, what does it mean for an investor or a corporate treasurer? Perhaps much of this is more relevant to fund managers, or those with long-term cash portfolios (probably six months), but there are four areas worth giving consideration:

Jim Clifford OBE MSc FCA is head of impact and advisory at Bates Wells Braithwaite, where he develops social investment instruments and social programmes, and advises on impact investment and measurement.

Claudia Burger is an analyst within the impact and advisory team at Bates Wells Braithwaite, working on social investment opportunities and programmes.

This article was taken from the Jul/Aug 2017 issue of The Treasurer magazine. For more great insights, log in to view the full issue or sign up for eAffiliate membership