Historically, corporate treasurers dealt with volatility as a series of isolated disruptions to be managed before things returned to business as usual.

But that underlying assumption has changed: volatility over recent years has been sustained, and treasury teams have adapted by embedding uncertainty into core decision-making.

Rather than viewing disruption as episodic, corporate treasurers now treat uncertainty as a baseline assumption in liquidity management, funding strategy and risk calibration.

This is one of the defining insights of our 2026 Corporate Debt and Treasury Report, published in partnership with the Association of Corporate Treasurers (ACT), now in its 13th edition.

Drawn from a survey conducted in the first six weeks of 2026 (before the crisis in the Middle East) and supplemented by interviews with treasury professionals at FTSE 100, FTSE 250 and equivalent companies in Q1 2026, the findings point to a profession that has fundamentally recalibrated its operating model.

Further key insights include:

In Q1 2026, almost three quarters (72%) of respondents described the impact of macroeconomic and geopolitical events as “business as usual but some continued disruption anticipated”. This is up sharply from 41% in 2025.

Simultaneously, those reporting a material negative impact fell from less than one in five (17%) in 2025 to just under one in 10 (8%) this year.

Treasurers say that macroeconomic and geopolitical events causing disruption appear to be relentless, leading to a sense of “omnicrisis”. Treasury teams are adapting accordingly.

Respondents reported that conflict in the Middle East is causing significant concern for businesses, not least because of its impact on energy prices, as well as uncertainty around US tariffs.

Many UK-based respondents also expressed scepticism that the government's growth policy is delivering its intended impact.

The survey results reflect a more cautious approach to spending.

Only one quarter (25%) of respondents expect to increase spending on acquisitions in 2026, down from more than a third (38%) in 2025. Anticipated increases in capex have also fallen, from around a half (51%) to just over a third (35%).

In contrast, more than a third (38%) anticipate spending more on repaying debt in 2026, up from more than a quarter (27%) in 2025 and less than that (22%) in 2024.

There is an expected increase in the anticipated return of cash to shareholders via dividends – one third (34%) say they anticipate they will spend more on this in 2026, compared with a quarter (25%) who said this in 2025. Respondents also expect to spend more on share buybacks (27% vs 21% in 2025), taking advantage of suppressed share prices.

The aggregate picture is one of prudence, where deleveraging and balance sheet resilience are higher priorities than expansion. However, the view of acquisitions appears to be very sector-specific, with some interviewees showing an ongoing appetite for M&A when the right opportunities arise.

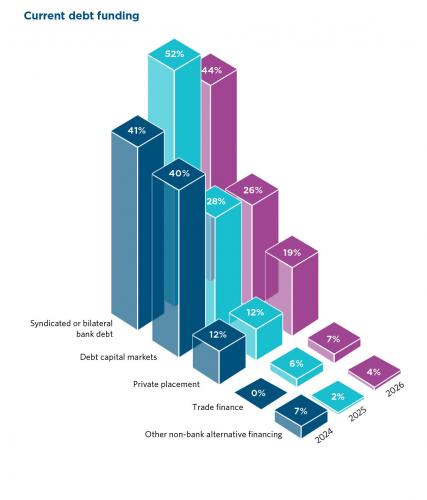

Treasurers are not abandoning traditional bank and bond markets but are instead layering in additional tools

An appetite for debt diversification is fairly evenly split. Almost half (45%) of respondents are selectively diversifying funding sources to improve flexibility and access to liquidity. The remaining respondents (55%) remain confident in their existing arrangements and counterparties and do not have any clear drivers for diversification.

Treasurers are not abandoning traditional bank and bond markets but are instead layering in additional tools, such as private placements, trade finance, and alternative lenders, to improve flexibility.

Private placements rose from just over one in 10 (12%) of the funding mix in both 2024 and 2025 to almost one in five (19%) in 2026, with transaction volumes reportedly reaching record levels in 2025 in certain sectors.

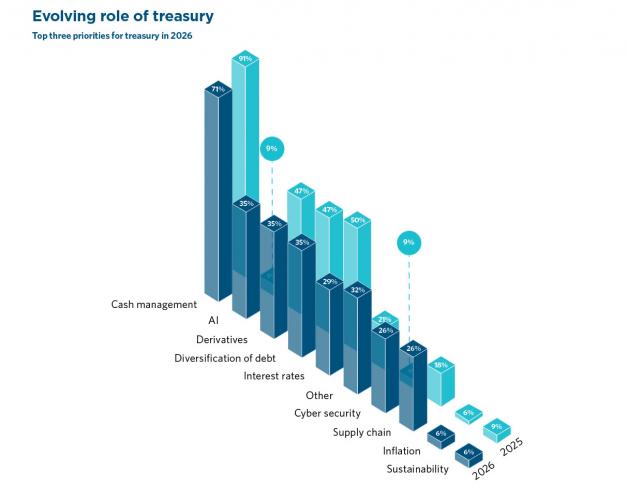

While cash management remains fundamental, treasurers noted that their priorities for 2026 also encompass:

AI holds promise for treasury teams, but it has yet to deliver in practice. Work is still required on data quality, standardisation and output reliability. As one survey respondent observed: “You still need people to make judgment – technology is not better than good people.”

The shift from periodic shocks to “omnicrisis” is not merely a change in mindset. It underpins a fundamental shift in how the treasury function operates, plans and implements strategies.

Stacey Pang, counsel at Herbert Smith Freehills Kramer

Emily Barry, knowledge counsel at Herbert Smith Freehills Kramer