The Tokyo pro-bond market is a new bond market for professional investors (hence ‘pro’ stands for ‘professional investors’). It was established under a 2008 revision to Japan’s Financial Instruments and Exchange Act that provides a legal framework for the establishment of markets intended solely for financial professionals.

The Tokyo pro-bond market offers flexible and timely issuances of bonds, and provides more convenience to issuers, investors, securities companies and other market participants, both in Japan and overseas, than the traditional samurai bond format.

The Tokyo pro-bond market contributes to the development of Japan’s bond market as a central player in Asia’s financial markets.

Earlier this year, Dutch bank ING sought Barclays’ help to access the Japanese bond market. The move was a calculated initiative by ING to broaden its investor base in Japan, taking advantage of a relaxation of the stringent requirements associated with the issuance of traditional samurai bonds.

The JPY 50.7bn (€500m) issuance by ING on 10 April 2012 was the first transaction on the Tokyo pro-bond platform, a new bond market for Japanese professional investors launched in May 2011. A number of international issuers are now set to capitalise on the pent-up demand among Japanese investors for non-domestic names in their portfolios.

For years, Japanese investors and international issuers have looked at each other longingly, frustrated in the knowledge that the country’s traditional samurai market posed too many cultural and procedural hurdles for it to be easily and regularly accessed. So in 2008, the Japanese government decided to tackle this by incorporating the Tokyo pro-bond market into its Financial Instruments and Exchange Act.

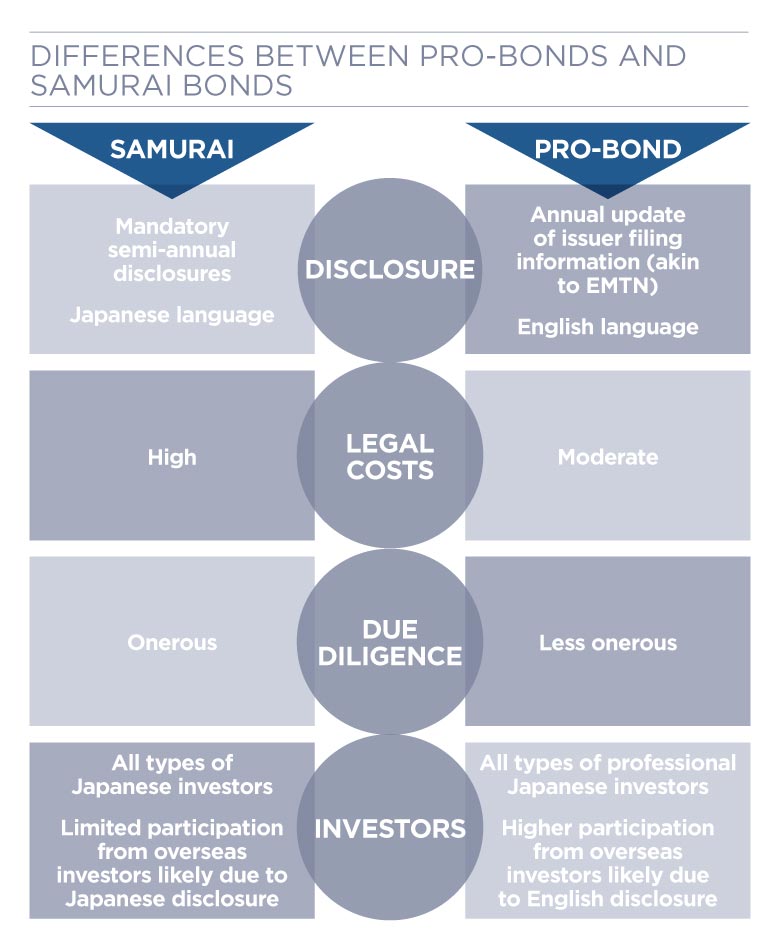

Thanks to pro-bonds, non-domestic financial institutions, corporates and even sovereign issuers have a practical and viable alternative to full Japanese-language samurai disclosure for the first time. They can now use English-language disclosure to place their securities.

In addition, pro-bonds have other characteristics that should make them attractive to corporate treasurers who want to diversify their investor base:

The decision to attract Japanese fixed-income investors was a natural step for ING to take. While it’s in the process of formally separating its banking and insurance businesses, it has been in the Asian markets since the 1970s and is present in over 40 countries worldwide. It currently operates retail banking and insurance businesses in seven key Asian markets.

ING began its pro-bond programme at the end of March 2012 by listing a shelf programme worth JPY 200bn (€2bn) that allows it to issue bonds over the following 12 months, parallel with a euro medium term note (EMTN) programme.

After an important investor road trip in which ING senior management and investor relations successfully articulated the company’s fundamentals and growth plans, ING issued a JPY 50.7bn bond, which priced on 10 April. The deal was distributed via 40 tickets across a spectrum of banks, asset managers and insurance companies. Bonds were even distributed to international investors who favoured the English disclosure.

We were talking to some of the most sophisticated asset managers in the world, none of whom pushed back once they heard the story

The deal priced at 100 basis points above the comparable yen swap curve – not an insignificant point in understanding this transaction. Given the persistent low-yield environment in Japan, local investors are constantly alert to opportunities that offer a yield pick-up. Crucially, ING could offer Japanese investors an appealing headline spread at an all-in level that remained cost-competitive to the euro and US dollar markets.

It is important to examine particular elements of the deal to understand the reasons for its success and why it augurs so well for further activity in this market.

We feel confident that over the next few years there will be a steady flow of issuance on the pro-bond platform. It won’t be a heavy flow initially, but the market will develop slowly with high-quality names, particularly among financial institutions, making first use of it.

If you’re looking for an analogy, go back to the US in the early 1990s, when 144As started appearing – initially as a way to let people invest in sovereign debt deals. For the first few years, those deals came in a trickle until the 144a asset class developed into a full-bore, high-volume marketplace.

The Tokyo pro-bond market is suitable for a broad range of issuers across the financial institution, corporate, sovereign, supranational and agency sectors. The potential issuers that should consider pro-bond format include:

David Lyon is managing director, financial institutions group − investment banking division, at Barclays, London.

E: david.lyon@barclays.com

Kenji Setogawa is head of fixed income syndicate, Japan, at Barclays Tokyo.

E: kenji.setogawa@barclays.com