A daunting-looking question in your exam will often examine a familiar financial relationship, but from a slightly different point of view to the one you’re used to. This article will show you how to use a standard answer plan to transform a tough exam question into recognisable simpler steps. Your task can then become as easy as filling in the blanks.

Here we apply a simple, standard ‘square of arrows’, diagram, which unlocks many FX exam questions. (This particular FX content is relevant for the international treasury management (ITM), international cash management (ICM), financial maths & modelling (FMM), risk management (RM) and MCT advanced diploma papers, although the diagram-planning technique applies to all exams.)

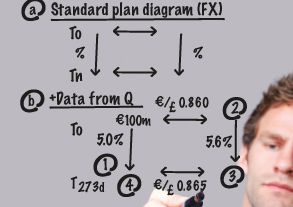

Let’s refresh our understanding about forward FX rates. The FX standard plan diagram [see illustration (a) below] links: the spot FX rate between two currencies; the interest rates in each currency; and the forward FX rate.

One expression of this relationship is interest rate parity theory (IRP). IRP theory says that the forward FX rate (available in the market today) should normally be equal to the current spot FX rate, adjusted for the difference in interest rates between the currency pair: Forward FX rate = spot FX rate +/- interest rate differential.

For example, in the following simplified case:

We already have three of the four linked rates in our planning diagram. So we can calculate the fourth (missing) rate as: Forward FX rate (maturity one period hence) = $2.00 x 1.10/1.00 = $2.20 (per £1).

The higher interest rate currency ($ here) is weaker in the forward FX market.

If the IRP relationship did not hold, it would normally mean that there was a mispricing in one of the rates. (This would be very unusual in practice.) In that unusual situation, it would be possible to ‘round trip’ at a profit by dealing simultaneously in all four of the related instruments. Usefully, this was also part of the answer to the exam question, discussed below.

The same standard planning diagram also illustrates how a synthetic currency borrowing can be constructed. This is done as follows:

Synthetic borrowings often appear in ACT exams. Consider this five-mark question in the April 2012 FMM exam:

You are the group treasurer of a highly rated German group. For operational reasons, you need to borrow EUR 100m for 273 days. You are considering either:

You have obtained the following market rates for nine months (273 days) maturity:

Interest rates:

EUR 5.0000%

GBP 5.6000%

EUR/GBP Exchange rates:

Spot GBP 0.8600

Nine months (273 days) forward GBP 0.8650

Always read the Required part of the question first. And read it at least two or three times. It is important to read it carefully to identify all of its elements and make sure you don’t miss any easy marks. How many different elements can you identify in this Required?

Well, this question is about:

Using a GBP borrowing swapped into EUR means:

How many elements did you identify? If you haven’t analysed the Required yet, please do that now.

If you hadn’t read the Required carefully, you might have missed the easy marks for the later elements. Indeed, the examiner wrote: “Many [candidates] threw marks away because, having finished the calculations, they moved on – but the final phrase of the Required was ‘Comment on your result...’ Those who made no comment missed the marks for such a comment.”

To get those easy marks, you need to identify and answer the ‘Comment’ part of the Required.

It’s time to work on the numbers. Coincidentally there are also six key numbers in the question: (i) the EUR 100m required; (ii) the maturity of 273 days; (iii) the quoted interest rates of 5.0% and (iv) 5.6%; (v) the spot FX rate of EUR 1 = 0.860 GBP; and (vi) the forward FX rate of EUR 1 = 0.865 GBP.

Transferring these numbers onto our diagram [see illustration below] shows we need to calculate just four missing cash flows: (1) The repayment of EUR 100m plus EUR interest, on the direct borrowing.

(2) The alternative GBP borrowing amount required at Time 0. (3) The repayment of GBP principal and interest at maturity. (4) The EUR equivalent of the GBP outflow at maturity.

Now we need just four simple standard calculations to fill in our four blank spaces.

Filling in the blanks

(i) Borrowing directly:

T0 Inflow €100.000m. (1) T273d Outflow €100m x (1 + 0.050 x 273/360) = €(103.792)m.

(ii) Swapped borrowing: (2) T0 Inflow €100m x 0.860 £/€ = £86.000m. (3) T273d Outflow £86m x (1 + 0.056 x 273/365) = £(89.602)m. (4) T273d Outflow £(89.602)m ÷ 0.865 £/€ = €(103.586)m repaid.

Finally, there are easy marks to pick up for our commentary. The exam technique here is:

Practice applying standard plans like this to break down many different exam questions into smaller familiar pieces. If your standard plans are diagrams, so much the better. You will score easy marks for your plans, as well as reducing errors and saving time in your detailed calculations. I wish you the best of luck with your studies.

Doug Williamson FCT is an examiner, tutor and exam scrutineer for six ACT exam courses.