Cash pooling is not as prevalent in Asia as it is in Europe and there are a number of reasons for this. Europe has moved to a largely homogeneous currency zone where countries either operate within the euro or have freely convertible currencies, whereas Asia is still a mixed bag of currencies with many restrictions on convertibility.

Controls on capital are also much more restrictive in Asia, making cross-border pooling difficult and cumbersome. Central banks often require reporting and documentary evidence and invoices to support each transaction. In some locations, cash pooling is simply not possible.

Added to this are the various regulatory, legal and tax regimes that need to be reviewed – many of which are still in their infancy relative to other parts of the world.

For my company, CLSA, a brokerage and investment group, another challenge to pooling came from the historical approach it took to managing cash. As a global financial institution with many regulated entities, cash management was often left to the individual entities themselves. This meant that some entities operated with debit balances and others were always long in cash. And CLSA was not alone in taking this approach. Bank relationship managers tend to be used to financial institutions acting in this way. So while they are often experts in custody arrangements, they have little knowledge of cash pooling.

The combination of the above factors certainly makes it easier to just leave your cash where it is. But in the modern treasury environment that is not a luxury we can afford.

When considering cash pooling, CLSA’s first action was to survey the market to see what products were available in Asia and which banks were offering them. We spoke to numerous banks, large and small, across the region to gather ideas on what was possible.

It quickly became clear that some banks had much more expertise than others. Once we had identified HSBC as the strongest regional player in cash management, we quickly moved into designing the pool.

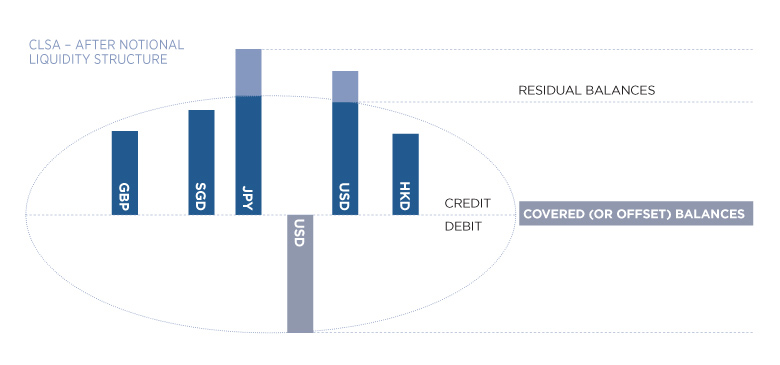

The usual debate of notional pooling versus physical pooling took place. As previously noted, we operate many regulated entities. These entities often have to take a haircut to their regulatory capital for intercompany balances. A physical pool would have therefore created many such intercompany balances and an unwelcome distraction to the benefits of a pool.

The offset pool is essentially a notional cash pool where some participants deposit funds into the pool while others withdraw

At this point, an analysis was undertaken of the various tax (such as interest deductibility and withholding tax) and transfer pricing issues that arise. The latter was difficult given the relatively early stage of development of a number of the transfer pricing regimes in Asia.

In the end, we opted for a hybrid solution combining a multiple currency pool (or offset pool) with an interest enhancement pool. The offset pool is essentially a notional cash pool where some participants deposit funds into the pool while others withdraw. The pool was established in Hong Kong and the whole structure is covered by cross-guarantees between the entities. The pool is backstopped with an undrawn committed facility to ensure that all depositors can quickly access their liquidity if needed. This adds cost, but also security, to the structure.

The interest enhancement pool is a pool that helps to combine all excess operational deposits held across the region. The money can be held in local currency and/or foreign currency in current accounts. The total balance is notionally converted to a base currency and interest is paid at the account level locally. The total interest is calculated on a tiered basis, so the more funds you have in the pool, the higher interest rate you will earn across all currencies and accounts within the pool.

For the offset pool, we included countries such as Hong Kong, Singapore and Japan. These economies have convertible currencies and cross-border flows are not as restrictive as in other parts of Asia. For the enhancement pool, we included countries such as Korea and Taiwan, where local restrictions make notional multi-currency cash pooling more difficult.

It goes without saying that taking on a project of this scope is a major undertaking. The first thing to do was to set up a project team and a plan with HSBC. That way we could map out the key milestones and the required resources on both sides to meet them. There are many hurdles to jump such as putting in place cross-guarantees, setting up the bank account structure, working with finance to establish the controls and accounting for the new pools. You need detailed planning to manage the process.

We also needed to get a buy-in from the business. The pooling proposal was taken to our asset and liability committee and approved. It helps to have approval right from the top when you are putting in place a policy that changes – or challenges – long-standing practices.

Once we had our detailed plan and the business buy-in, it was a matter of following the strategy until all the agreements and accounts were in place. I had a dedicated person in my team tracking the deliverables and managing the different components. Luckily, HSBC had assigned a dedicated project manager to ensure the smooth delivery of the project from the bank’s end.

The impact of this project has been transformational. The main benefits have been:

Brendan McGraw is treasurer for CLSA