“Candidates struggled... even with the first step of estimating the effective loan amount if a minimum balance of 20% of the loan amount is to be maintained [in a non-interest-bearing current account].”

Excerpt from Corporate Finance and Funding (CFF) Examiner’s Report, October 2011

Estimating the effective loan amount without a struggle in the exam required:

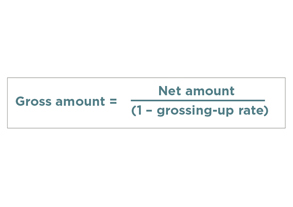

Let’s recap what a grossing-up calculation involves, and what it doesn’t. Then we’ll apply it to some exam-based examples.

Grossing up means increasing a net amount using the following relationship:

A common example is grossing up interest for income tax or withholding tax.

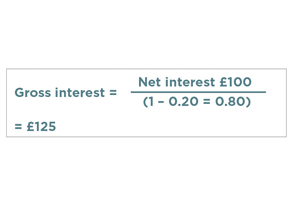

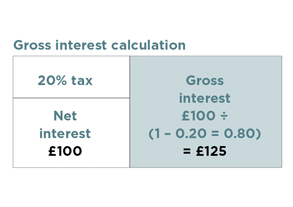

For example, net interest is £100 and the tax rate is 20% (= 0.20).

In this case:

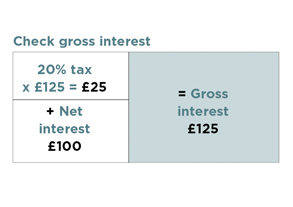

Note: The tax is charged on the gross amount of £125 (x 20% = £25 tax).

This is why the calculation is to DIVIDE BY (1 – tax rate) to give the right answer of £100/(1 – 0.20) = £125.

The calculation is not to multiply by (1 + tax rate). This would give a wrong answer of £100 x (1 + 0.20) = £120, which is too small.

(Because tax payable at 20% on £120 = £24; and when £24 tax is deducted from £120, only £96 remains, not the required £100.)

Now, let’s prove that our answer is right.

A recent CFF exam offered marks for no fewer than three separate grossing-up calculations. Some candidates got all three wrong or didn’t attempt them. Or perhaps they didn’t realise that grossing up was needed.

Happier candidates who had understood and practised the grossing-up technique – and spotted where it was relevant – scored marks in all three places.

CFF summarised extracts, October 2011:

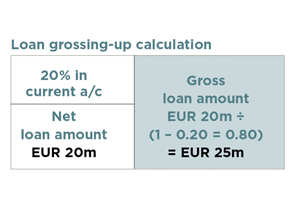

The treasurer of Misbah plc wishes to raise a net amount of at least EUR 20m and is considering:

A line of credit from the company’s bankers at an interest rate of 5.5% per annum, with an accompanying requirement that, for the duration of the loan, a minimum balance of 20% of the loan amount should be maintained in the company’s non-interest-bearing current account with the bank.

Part of the question required evaluation of the true cost of this loan facility.

Interest will be charged (at 5.5%) on the gross loan amount, not the net.

So the first step is to calculate the gross loan amount.

The 20% balance to be maintained in the current account is not available for the borrower during the life of the loan. It is locked away (like the 20% tax that was payable in our earlier example).

So this grossing-up calculation will be very similar to the gross interest calculation that we did earlier.

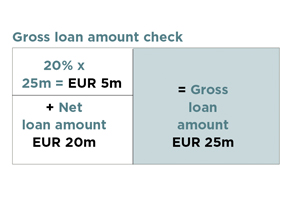

Now, prove the answer.

EUR 25m is the amount on which interest will be calculated and charged by the bank. Even though only EUR 20m will be available to the borrower (EUR 5m = 20% being locked in the current account). In the exam, as in life, this loan is more expensive than it appears to be.

“Many candidates made errors at the first step of estimating the gross value of share issue required to raise a net amount of £24m after issue costs amounting to 4% of the gross proceeds.”

CFF Examiner’s Report, October 2011

CFF summarised extracts, October 2011:

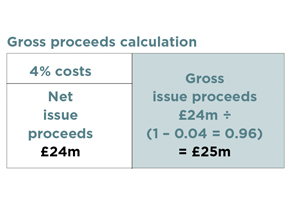

Flot proposes to obtain a quotation on the London Stock Exchange and raise additional share capital for a net amount of £24m. Administration and issue costs are expected to be 4% of the gross receipts.

Part of this question required calculating the gross receipts.

The share issue is good news for the advisers because of the fees they will earn.

The 4% total costs paid to the administrators and advisers are not available for Flot. But they will be part of the total subscription price paid by the investors.

So the shape of this grossing-up calculation is similar to the previous one.

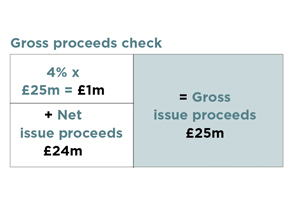

Now, proving it.

So £25m is the total amount that Flot needs to attract from its investors.

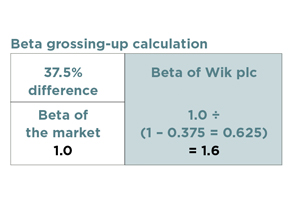

“Many candidates were unable to find the correct company beta using the information provided – which simply stated that ‘the beta of the market is 37.5% less than the beta of Wik plc’.”

CFF Examiner’s Report, October 2011

This was the hardest grossing-up calculation in the same exam. But the basic grossing-up idea was exactly the same.

CFF summarised extracts, October 2011:

For Flot’s share issue to be successful, the company has been advised that it should make the issue by means of a comparison with an appropriate quoted company. The most appropriate company for this purpose is considered to be Wik plc.

The beta of the market is 37.5% less than the beta of Wik plc.

Part of this question required calculating Wik plc’s beta.

For this part we need to know:

There is a difference of 37.5% between the beta of Wik plc and the beta of the market, defined as a proportion of the beta of Wik plc (to be calculated).

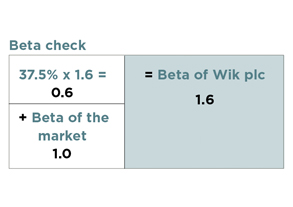

Let’s prove the calculated beta.

The market beta of 1.0 is indeed smaller than Wik plc’s beta of 1.6 by 0.6/1.6 = 37.5%.

Note that it is not right to add the 37.5% to 1.0 to calculate a beta of 1.375.

This would be too small because the market beta of 1.0 would only be smaller than it by 0.375/1.375 = 27% (rather than the 37.5% we need).

Now you understand grossing up:

Then you can score full marks for grossing up if it appears again in your real exam.

Doug Williamson FCT is an examiner, tutor and exam scrutineer for six ACT exam courses