Setting aside the financial crisis, the big macroeconomic story of the past decade has been the rise of China to become the world’s second-largest economy. If predictions by the Organisation for Economic Co-operation and Development (OECD) prove correct, this phenomenal growth trajectory will continue and it will overtake the US by 2016. With growth in the developed world still anaemic due to sovereign indebtedness and widespread economic uncertainty, it is easy to see the appeal of trading with China and other emerging markets to companies from the developed world.

According to Kevin Gardiner, head of investment strategy, EMEA at Barclays Wealth & Investment Management, there are three main factors that typically trigger changes in trading patterns. The first is the rate of structural growth in domestic spending in the big economies. For example, the growing middle class in China is driving increased consumer spending – fuelling demand for imports, raw material and finished goods into China from the rest of the world. Secondly, changes in measures of competitiveness play an important role. If one country has higher inflation or lower productivity growth than another, it tends to get a smaller share of trade. Thirdly, policy variables are influential: a country’s economic liberalism or protectionism relative to its peers can affect the role that it plays in world trade. Recent liberalisation of some economies, particularly in Asia, but increasingly in Africa as well, has allowed exports from those regions to make their way more easily into the wider global economy.

With growth in the developed world still anaemic, it is easy to see the appeal of trading with China and other emerging markets

In addition, there is another significant driver for changing trade patterns – one that is often understated. That is trade that occurs within the same enterprise, but across national boundaries. It is not a new phenomenon, but it is often deeply linked to future trade flows whether those are import or export. This entails foreign companies investing in operations in emerging markets to tap into local demand or less expensive labour pools or to improve access to a supply of commodities. Invariably, this leads to trade flow and generates demand for innovative financing techniques in emerging markets to support those flows. For example, we see soft commodities players in African markets making greater use of supplier financing structures to promote loyalty within their supplier bases.

Over the past decade, the emergence of China as an economic superpower has had a profound impact on global trading patterns. While the US and the eurozone are the biggest buyers of its goods, China’s economic might has nevertheless stimulated growth in South-South trading – in other words, trade between countries in Asia, Africa and Latin America.

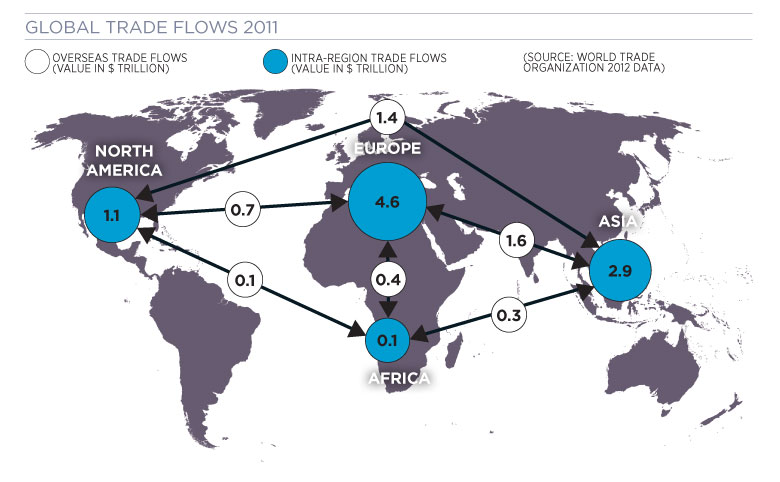

South-South trade growth outpaced North-North by just over two and a half times in the 10-year period leading up to 2011, according to the International Trade Centre. As a result, many of our clients are adapting their regional strategies. This translates into significant interest in local, relatively plain, vanilla trade and banking facilities as well as heightened demand for ‘without recourse’ receivables on an increasing number of local and diverse trading counterparties.

Although China was the big macroeconomic success story of the past 10 years, Africa is expected to present some of the best opportunities over the coming decade. According to the International Monetary Fund (IMF), seven out of the 10 fastest-growing economies in the world are expected to be African by 2015. These are Ethiopia, Mozambique, Nigeria, Zambia, Tanzania, Congo and Ghana. Nigeria is particularly seen as a country to watch because of its population size – over 170 million – and its vast oil reserves.

International Trade Centre figures show that trade growth between Africa and the rest of the world was up a staggering 51% in 2011. In comparison, US export growth has moved a tiny 4% over the past five years.

Turning to domestic demand, the African Development Bank has predicted that African consumer spending will increase from $680bn in 2008 to $2.2 trillion by 2030. Asian multinationals, in particular, are lured to Africa by its rich supply of commodities and the prospect of supplying its local markets, and they are investing heavily to access the opportunity. Due to easing cost of travel and technology advances over the past decade, building a business overseas is not the exclusive domain of global corporations in the way it once was.

We see many clients of differing sizes from a diverse range of sectors setting up subsidiaries in emerging markets. In Africa, we have seen a number of large companies enter the market through one or more of the five major hubs – South Africa, Kenya, Egypt, Nigeria and Ghana. The common theme is that they want to leverage their liquidity across borders and find the most efficient way of using their cash, FX resources and banking facilities (including trade and counterparty risk lines) while accessing new trade flows.

Trading with, or building a business, in any emerging market is not without its risks, but the banking industry is innovating to help companies address these risks. When moving into a new market, the first and most important step is to gain access to local knowledge. Trusted banking partners can assist with this through their relationship teams and by providing introductions to important market contacts. Beyond this, treasurers will find that many of the usual credit, counterparty and FX risk-management tools are available in more developed markets along with adaptions of these products that allow for local market conditions. For example, highly automated supplier finance programmes that are seen in Europe and the US are altered to fit into manual, paper-driven exchanges between buyers and sellers in some developing markets.

Asian multinationals are lured to Africa by its rich supply of commodities

Not all the threats that companies face are related to financial risk, however. The war for talent tends to be a major challenge for companies that invest in emerging markets, particularly in Africa, where there is a small pool of experienced local people across the key industries and roles. While almost all markets accept the need to bring in foreign talent to support growth and development, maintaining the balance with regards to local regulation can lead to some undesirable outcomes for companies. These include a high employee turnover and the considerable expense that goes with securing the few talented individuals in the market. This inevitably affects growth since success is often defined by the quality and quantity of talent on the ground. Political instability can also pose a threat to sustainable economic growth.

While China will undoubtedly continue to dominate growth in world trade for the foreseeable future, we expect to see some slowdown in its growth and that of other emerging economies. Greater integration of the global economy is set to remain the underlying theme of the next decade and there will be more joint ventures and offshoring in all directions: South-South, North-South, North-North and East-West. In 10 years’ time, new industries and trade flows will have evolved significantly – and in doing so, they will change assumptions of what is considered ‘developed’. For example, according to the IMF, Latin American countries such as Peru are experiencing strong GDP trade flow growth, which is driving a surge in financing activity. Bank-to-bank trade finance – a key indicator of Latin American trade flow growth – has increased sixfold since 2005. Where will your company be trading in 2023?

Ray Zabarte is global head of trade and working capital product management at Barclays