A credit rating is an opinion of both the risk of default on a loan instrument, typically a bond, and the loss in the event of default. It can also apply generally to a borrower independently of a particular instrument. The risk of default carries more weight, especially for higher-grade borrowers where that risk is considered low. Loss given default carries more weight when risk of default is considered high. There is a significant difference between investment-grade ratings and speculative (or sub-investment-grade) ratings.

Credit ratings are for the larger borrower and they are normally first used when the borrower makes a bond market debut

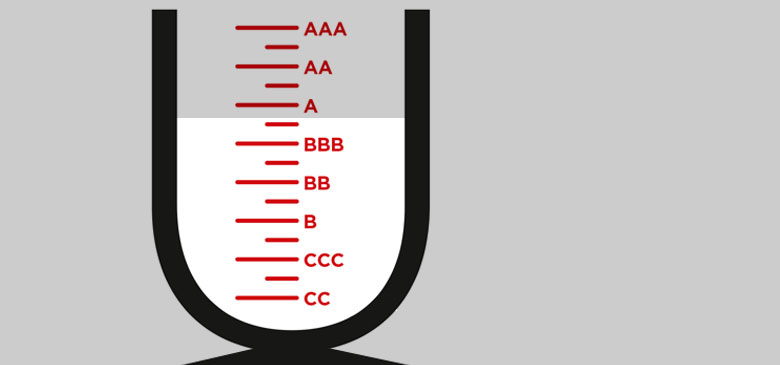

Long-term and short-term ratings both exist, although the long-term rating is usually seen as the more important. The main agencies rate borrowers and their loan issuance from AAA (Aaa) to BBB- (Baa3) as investment-grade and BB+ (Ba1) to C as speculative-grade for long-term ratings. The lowest rating, D, means the borrower is in default.

Insurance companies in the US private placement market use their own ratings, known as the National Association of Insurance Commissioners ratings.

Credit ratings are an essential component of the debt markets, and especially the bond markets. Investment-grade borrowers use the ‘high-grade’ market, whereas sub-investment-grade borrowers use the ‘high-yield’ market. This split also affects documentation in both bank and debt markets, with high-yield borrowers usually having to provide security and detailed covenant protection.

Credit ratings dictate:

In general, a higher rating leads to more liquidity at a lower price. The high-yield market is most subject to cycles and there have been periods when there is little liquidity in that market, often at any cost. This contrasts with the high-grade market, which is usually open. Because of this, corporates often target a particular credit rating in their financial strategy and try to persuade agencies to rate them as highly as possible.

Credit ratings are for the larger borrower and they are normally first used when the borrower makes a bond market debut. Investment-grade ratings are the preserve of the largest and most stable borrowers of all, which are usually mature borrowers. Investors in these companies don’t want their bonds to seesaw between rating notches and they particularly dislike downgrades.

A credit rating is based on both business risk and financial risk. Business risk comes from a review of the sector and the borrower’s position in that sector along with an assessment of management capabilities. Financial risk analysis is predominantly around financial ratios. This is where the treasurer comes in.

The treasurer is typically tasked with managing rating agency relationships, since they are akin to lender relationships, but needs additional support. Management, usually the CEO and CFO, but often also including divisional or operating management, must contribute to the agency relationships and presentations. But the treasurer will be expected to present on the company’s financial strategy, including forecasts and financing plans.

Most treasurers maintain sophisticated forecasting models adapted especially for the agencies. Agencies have been reluctant to publish exact mappings of ratios to ratings, but there are occasional glimpses into their thinking, which are very useful to treasurers.

Treasurers also use credit ratings to assess counterparty risk. This mostly relates to cash investment with banks, but they also use ratings to check the creditworthiness of trading counterparties for both receivables exposure and long-term trading.

Banks are no longer considered completely safe, and one way of assessing their suitability for deposits is to look at their rating. It is interesting to take this counterpoint view and see some of the weaknesses in ratings. Generally, agencies are quite slow to act on news, preferring stability in their ratings, whereas markets can act very quickly against banks.

It is tempting to compare a rating for a bank (some of the most heavily used typically being AA or A), with a rating for a money market fund, which is typically AAA. But they are different asset classes and the ratings are not strictly comparable.

Rating agencies are now regulated and there is more choice available. So treasurers cannot ignore them and should ensure they get the best out of them when both investing and raising funds.

Will Spinney is associate director of education at the ACT