Climate action efforts around the world increasingly rely on carbon markets as a tool for reducing greenhouse gas (GHG) emissions. These markets put a price on carbon, channel funding towards climate solutions and help countries and companies progress towards their climate goals. Consequently, they help companies manage their emissions risks as part of their emission reduction plans and targets.

Carbon credits are traded in two main markets: compliance and voluntary.

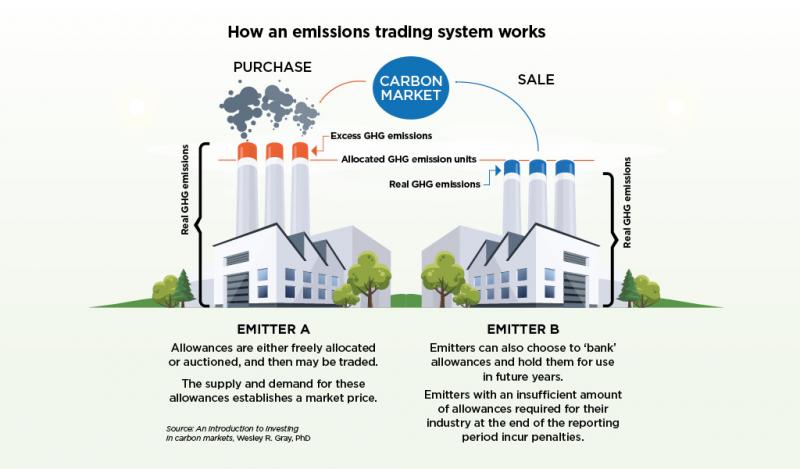

1. Compliance markets (Emissions trading systems)

In compliance carbon markets, governments set a cap on the total annually permitted emissions for the country and allocate or auction “allowances” to regulated companies that permit holders of these “allowances” to emit a specific amount of CO₂ each year. For example, The EU Emissions Trading System (EU ETS) and the UK ETS are prominent schemes. Each company must surrender allowances equal to their actual emissions.

The cap becomes more stringent over time, making allowances scarcer and more expensive. If companies reduce emissions, they can sell excess allowances; if they exceed their cap, they must buy more or face heavy fines, thereby, creating a financial incentive to these companies to reduce their emissions.

The money raised by governments from auctioning these allowances typically goes into government funds, which are meant to support investments in national climate projects, renewable energy and energy efficiency.

2. Carbon credit projects (and offsets)

Separate from government-imposed caps, these are projects that actively remove or prevent emissions, like afforestation, reforestation, wind and solar energy, or direct air capture (DAC) technology. Such projects can be nature-based (eg. protecting forests) or technological (eg. building renewable energy plants).

Organisations can purchase these credits to offset their own emissions, even beyond legal obligations. Credits represent verified emission reductions, commonly one metric tonne of CO₂ equivalent (tCO₂e) avoided or removed.

Under the 2015 Paris Agreement, Article 6 enables countries to trade emission reductions for use toward their climate targets, known as Nationally Determined Contributions (NDCs). Through this Article, if one country reduces emissions more than it pledged, those “extra” reductions can be sold to another country struggling to meet its target. This incentivises cost-effective solutions globally.

As rules for Article 6 mature, most recently at COP29, more nations are entering the international carbon credit market to help achieve their NDCs. Clearing these rules is unlocking large-scale country-by-country trading. Additionally, Article 6 is rapidly becoming the largest formal market for project-based carbon credits, reflecting growing governmental recognition of their need for such credits to meet climate commitments.

Many companies go beyond regulations by investing in voluntary carbon credits. Motivated by sustainability goals and corporate social responsibility, businesses buy carbon credits to neutralise unavoidable emissions or achieve carbon neutrality.

Voluntary credits fund a variety of projects, including reforestation, renewable energy, waste management and improved technologies in developing communities. High-quality credits must meet strict criteria: real, permanent, additional (wouldn’t have happened otherwise) and independently verified.

Carbon markets are becoming increasingly intertwined. Some compliance markets now allow regulated companies to use certain voluntary credits toward legal obligations: Singapore and the international aviation scheme CORSIA are leading examples, with the EU considering similar approaches. This convergence is blurring the lines between markets, allowing for more flexibility and investment in emission reductions globally.

A persistent challenge is ensuring that carbon credits represent real, additional and verifiable climate impact. The Integrity Council for the Voluntary Carbon Market (ICVCM) provides an independent governance framework, establishing Core Carbon Principles (CCPs) to set rigorous thresholds for project quality, environmental integrity and transparency. These standards aim to build trust and effectiveness in the global carbon market by ensuring only high-integrity credits are traded.

As of June 2025, more than 6,000 companies have set science-based targets with the Science Based Targets initiative (SBTi) to reduce GHG emissions. In addition to operational changes, companies purchase carbon credits to offset residual, hard-to-abate emissions. This creates a range of risks:

Additional considerations include regulatory developments, carbon credit accounting, project risks (which can be mitigated through insurance), credit quality, and credit vintage.

Carbon markets align financial incentives with climate goals, making polluters pay and supporting emission reductions. Furthermore, compliance and voluntary markets are both evolving, with growing integration between the two. Additionally, robust standards and independent verifications are essential to ensure carbon credits deliver real climate action and support the Paris Agreement.

Integrating carbon credits into emissions, financial and enterprise risk management strategies is essential, and the corporate treasurer is well positioned to manage these evolving risks.

Doris Honold is a board member of The Integrity Council for the Voluntary Carbon Market (ICVCM), Climate Bonds Initiative chair and UniCredit board member

Carel van Randwyck FCT, is an ACT Council Member, ACT Certificate in Sustainable Finance for Treasury course co-author and tutor, and a partner at Rodford & Partners

This article first appeared in The Treasurer Issue 3, 2025