Although Shell Malaysia issued the first Sukuk (Islamic bond) in 1990, it is only in the last 15-20 years that the international Sukuk market has grown. At the end of 2025, it is estimated that more than $1tn of Sukuks were outstanding, with $300bn of new issuance in 2025, a 25% year-on-year increase.

Furthermore, in recent years, there has also been a growth in sustainable Islamic finance, with $21.5bn being issued in 2025, a 38% year-on-year increase. Both these statistics compare favourably with a 20% year-on-year decrease in new sustainable bond issuance in 2025 of $871bn.

At its core, Islamic finance is designed to promote, among others, social justice, ethical conduct, dignity and stewardship of resources. These principles closely align with sustainability objectives and the UN’s 17 Sustainable Development Goals (SDGs). As a result, structuring a sustainable Sukuk is more intuitive than retrofitting ESG features into conventional debt.

Early green Sukuks successfully financed renewable energy, infrastructure and social projects, such as Majid Al Futtaim, a $600m Sukuk issued in May 2019 to finance green buildings and climate-friendly real estate assets, energy efficiency activities and water management. However, more recently, sustainability-linked Sukuks – where pricing/returns are linked to measurable sustainability targets – represent new developments. Such structures directly align issuer performance with environmental and social outcomes, improving accountability and investor confidence.

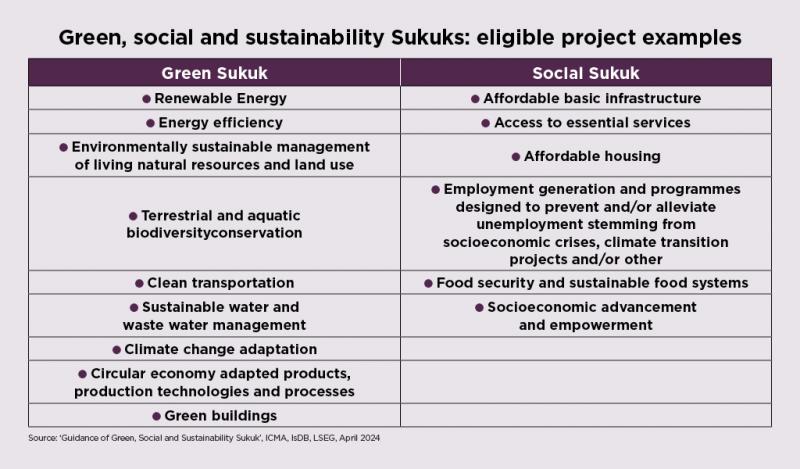

In April 2024, International Capital Markets Association (ICMA), the Islamic Development Bank (IsDB) and the London Stock Exchange Group (LSEG) published ‘Guidance on Green, Social and Sustainability Sukuk’ to provide, among other reasons, issuers and key market participants with information on how a Sukuk may be labelled as green, social and sustainability aligned with the ICMA Sustainable Bond Principles. This guidance also applies for transition, blue economy and gender finance raised through sustainable Sukuks.

The aim of bringing the issuance of sustainable Sukuks within ICMA’s Sustainable Bond Principles’ Framework is to facilitate the development of this market in accordance with best practice and ensuring it develops with high standards and integrity. As with conventional Sustainable Bonds, proceeds from Sustainable Sukuks can only be used for a defined list of eligible projects.

Sustainable Islamic Finance represents a distinct and growing funding opportunity for corporates as it sits at the intersection of two funding pools: Islamic finance and sustainable finance. This enables issuers to access a broader and more diversified investor base – Sharia compliant investors and sustainability-focused investors – which could:

Sustainable Islamic finance represents a growing funding opportunity for corporates as it sits at the intersection of Islamic and sustainable finance investor pools of capital. It enables corporates with real assets and credible sustainability strategies to access a larger, stickier, and values-aligned investor base, often on competitive terms, by bridging Islamic capital and global ESG/sustainability investor demand.

Carel van Randwyck FCT, FCA, ACT Council member, is the ACT Certificate in Sustainable Finance for Treasury course co-author and tutor, and a partner at Rodford & Partners