While your tax colleague will undertake much of the following, it is always worthwhile checking that they have done everything you would expect them to. Points to consider include:

In the first article of this series, we identified some of the most commonly encountered tax regulations that apply to treasury activities. Now we will look at the activities undertaken by cash managers and identify some of the taxes that they should consider.

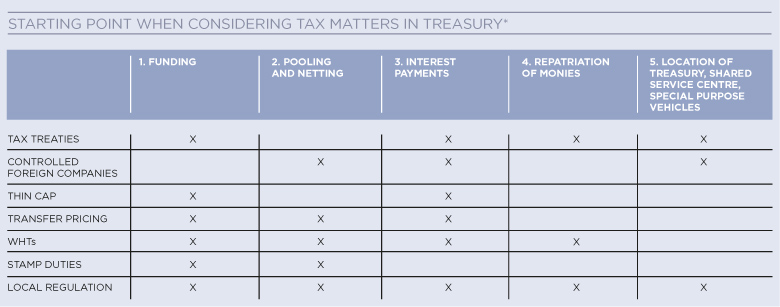

The rate of corporate income tax varies from territory to territory. It is typically preferable to arrange for interest expense to be borne in a territory that has not only a high rate of tax, but also sufficient taxable profits against which to relieve the expense. This can be achieved by maximising the amount that can be advanced to subsidiaries in the relevant territory by way of loan rather than equity capital – subject to thin capitalisation (thin cap) tax rules. Planning to push debt down through the group, where appropriate, will reduce, or at least defer, the amount of tax paid by the group, although the treatment of withholding taxes (WHTs) on (probably intercompany) interest payments must also be considered.

Interest and other funding costs, including FX movements, incurred on commercial funding arrangements are generally tax deductible. But rules vary from territory to territory as to the timing of relevant deductions, ie whether they can be claimed on an accruals basis (as recorded in the accounts), or only when paid or realised.

Both the physical concentration (sweeping) of funds and the notional offset of balances carry their own tax consequences, which may influence the choice of method.

When cash balances are physically concentrated (ie swept), participants replace bank balances with intercompany loans (amounts due to, or from, the group company maintaining the concentration account). Both thin cap and transfer pricing rules can apply here. Participants will have to pay or be paid interest at an arm’s-length rate on the intercompany balance, and their ‘borrowing’ from the concentration account (as opposed to borrowing from the bank) may be treated as debt funding for thin cap purposes.

Under notional pooling (where funds are not physically moved), participants retain their own account with the bank. No intercompany balances are created in this case (contrary to the process of concentration), but any cross-guarantee arrangements between participants may cause the balances to be treated as though they were loans between related parties and the thin cap, and WHT implications should therefore be considered.

Intercompany netting involves the offset of receivables and payables balances between companies of the same group to reduce the number of cash settlements. Such arrangements have potential tax consequences, with the more sophisticated ones carrying particular risks. Where a transaction is taxable on a payments or receipts basis, it is vital to be able to demonstrate to the tax authorities how and when an item was paid or received and so it is important that treasury systems and procedures are in place to provide the relevant data and meet the necessary requirements.

While local regulations are not necessarily a form of taxation, they should always be considered before implementing treasury structures

Some countries levy WHTs both on interest paid by borrowers and earned by lenders. This may depend on whether either party is a resident or a non-resident. WHTs can apply to both interest paid or received on cross-border intercompany loans, as well as on bank deposits. Where a double taxation agreement exists between the countries involved, the WHT is applied at a lower rate or may even be eliminated. WHTs paid may not always be allowed to be deducted as an expense against taxable earnings.

Returning cash to the parent country for use within the group or for payment of dividends is often a priority for any group. There are various ways in which this can be achieved, although each may have different tax consequences:

Accordingly, overseas profits should not simply be remitted as dividends without full consideration of the tax consequences.

Tax is a major issue in the selection of a treasury centre or shared service centre location. Areas set up specifically to attract treasury operations may be located in tax environments where local taxes are low and where there is special treatment of foreign earnings.

Such centres usually have practical tax rules designed specifically for financial activities. They will be located in countries with extensive tax treaties and there will be no WHTs on interest earned or paid, or income from dividends. These locations should also enable the repatriation of profits without tax deductions.

Strictly speaking, while local regulations are not necessarily a form of taxation, they should always be considered before implementing treasury structures.

For example, there may be legal constraints forbidding cross-border right of offset, prohibiting the co-mingling of resident and non-resident bank accounts (ie the two cannot be included in concentration arrangements such as pooling), requiring central bank reporting or requiring reserves to be maintained on a gross basis.

Planning to push debt down through the group, where appropriate, will reduce, or at least defer, the amount of tax paid by the group

Some countries differentiate between resident and non-resident bank accounts (ie bank accounts belonging to entities with or without residence in the country – normally defined for tax purposes by whether or not the board of the company meets in the country). The different classification of account may result in differences in:

In Germany, for example, resident and non-resident accounts cannot be co-mingled (pooled) and WHT is charged on interest earned in resident bank accounts only.

In some countries (even where thin cap is not an issue), payment of interest from a company to its parent may be regarded as a dividend and taxed accordingly by the parent’s tax authority. Furthermore, a company consistently remitting funds to a cash pool under a cash concentration structure may attract deemed dividends taxes.

Many countries require cross-border transactions (which may include movements from resident to non-resident accounts) and foreign currency transactions to be reported to the central bank or local monetary authority. This can become extremely complicated (and hence expensive) when subsidiaries are included in cross-border pooling arrangements and where such transactions are managed in an outsourced vehicle such as a shared service centre or payment factory.

Like any other business transaction, when doing business in an international environment the cash manager needs to be aware of the tax implications, some of which may be very different from those in the home country. The tax consequences of any transaction will not only depend on the nature of the transaction, but also on the specific circumstances of the company or companies involved, as well as the country of residence of the parties concerned.

Taxation rules are constantly changing, therefore up-to-date information should always be obtained when making any decision with possible tax effects. Every situation is slightly different, which is why it is important to work closely with colleagues and know when to seek specialist expertise.

The first part of this two-part series appeared in the September 2012 issue of The Treasurer.

Sarah Boyce is associate director of education at the ACT