It has been nearly four years since PIMCO coined the term ‘the New Normal’. At first, some criticised us for being too pessimistic – we anticipated an extended period of sub-par growth, elevated unemployment and enhanced capital market risks. Today, the New Normal is heard in many corners, reflecting a recognition that the fundamental forces behind it – deleveraging, de-globalisation and re-regulation – could persist for years.

This suggests that despite the welcome sense of calm that has spread across European markets thanks to the actions of the European Central Bank (ECB) last summer, the long-term outlook for Europe remains fraught with risk, at least until deeper issues are addressed. Also, the US still faces structural problems that will probably hinder growth, including long-term deficits and insufficient investment in infrastructure and education.

We believe that from about 2014, inflationary pressures will slowly build in the global system

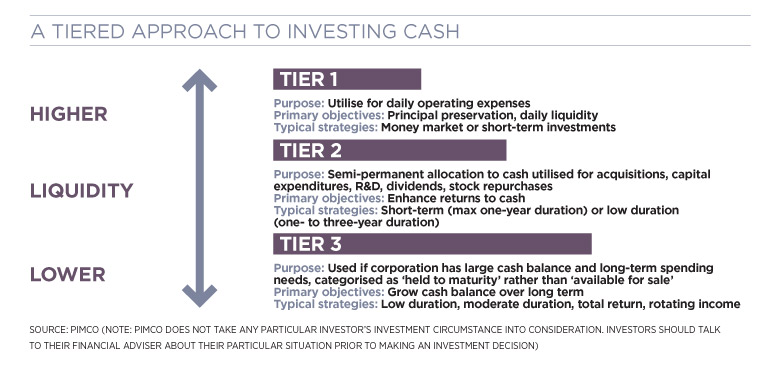

For treasurers, the New Normal means that debt issuance and cash management will be increasingly complex and challenging. The best defence may be a good offence – managing cash in a tiered approach, looking to a wider set of opportunities for funds not requiring prompt liquidity.

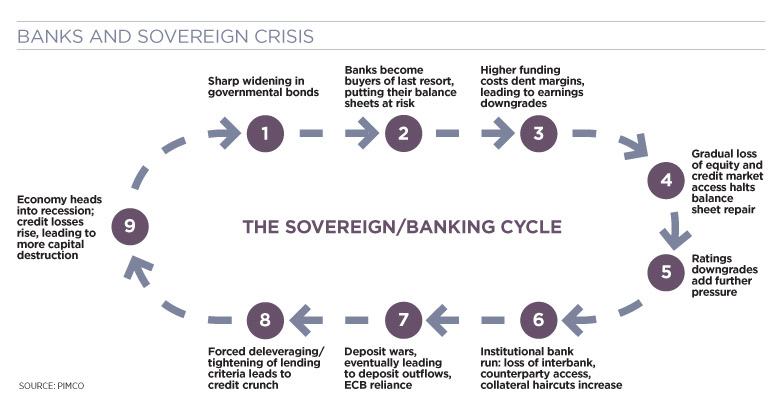

Insight into the dynamics of the New Normal can be gained by looking at the inter-relationship between Europe’s credit channel and capital markets during the crisis.

As a lender of last resort, the public sector was forced to take on a large portion of the private sector’s debt via asset purchases. Government balance sheets were stressed further by higher expenditures and lower tax receipts. Sovereign risk concerns pushed interest rates in several countries to unsustainable levels.

As sovereign fundings struggled to find private market support, domestic banks often became buyers of last resort. This exacerbated the private sector’s reluctance to lend to banks, increasing bank-funding costs. Rating agencies, wary of heightened liquidity and credit risks, downgraded the majority of eurozone members, multiple times for some. The downgrades, in turn, limited capital market access for both banks and sovereigns, spurring capital flight and deeper deleveraging.

In short, we witnessed a ‘crowding-out’ phenomenon, with public-sector borrowing driving interest rates higher for the private sector. (See diagram below.)

In addition to enhanced economic risks and tepid growth, regulatory reforms such as Basel III will pressure European banks to further shrink and simplify their balance sheets. This deleveraging could thwart access to credit for those that depend on direct bank financing as well as corporations seeking to raise funds from the capital markets.

Thankfully, of course, the ECB reversed some of these dynamics beginning last summer. The most dramatic phase started on 26 July, when President Mario Draghi announced that “within our mandate, the ECB is ready to do whatever it takes to preserve the euro”. Then, in September, the ECB’s governing council said the bank now stands ready to buy “unlimited” amounts of government bonds issued by struggling and systemically important peripheral countries (for example, Italy and Spain).

But despite the calm that has spread over European markets in recent months, the longer-term structural issues still need to be addressed. Simply put, over the three- to five-year horizon, the status quo is no longer an option. Europe either deepens its level of political and fiscal integration by creating its own fiscal capacity, or it will evolve into a smaller and less imperfect entity – namely, a closer political union of countries with more similar conditions.

Over the next three to five years, we believe the US will look good relative to Europe, outperforming in terms of growth and financial stability. Look for the Federal Reserve to maintain its monetisation efforts for a number of years; and look for other regulatory bodies to pursue similar avenues in the context of a generally more restrictive regulatory environment. The resulting policy mix, however, will do little to alleviate legitimate concerns about growth, jobs, inequality, debt and deficits; underlying structural fragilities of the economy will grow, in both economic and financial terms.

On balance, we believe that from about 2014, inflationary pressures will slowly build in the global system. With fiscal entities doing too little, central banks will probably maintain highly accommodating policies for too long. Nor should we forget the political appeal of resorting to inflation as a means to delever.

‘Financial repression’. ‘An era of confiscation’. Call it what you will. In this environment, the adage, ‘the best defence is a good offence’, rings true.

For investments in US dollars, for instance, we like a tiered approach. For funds requiring immediate cash liquidity, we like readily redeemable and high-quality assets such as treasury bills or repurchase agreements. For funds destined for intermediate uses, we prefer assets that capture liquidity premiums that avoid the narrow corral of regulated money-market eligible assets. (See graph below.)

In simple terms, this is where allocations to short-term strategies can be very compelling, as they dynamically adjust to changing conditions – market or regulatory – within the broader market. Most importantly, they are able to manage liquidity by defining it within a broader opportunity set compared with the structural limitations of a regulated money market fund (MMF). This in itself is a defensive scheme.

On the offensive side, we believe actively managed short-term strategies will move the ball up the field more effectively than other options. First, in this period of near 0%, or even negative interest rates, capital appreciation rather than simple yield needs to be a focus. Second, with continuing demand for ‘safe’ assets globally beginning to overshadow a declining supply dynamic, a definitive first-mover advantage exists for investors already in active liquidity-minded strategies; those portfolios may benefit from the tailwind of additional interest by investors looking for viable alternatives with proven, experienced managers. Again, this will be reflected in the capital appreciation of the underlying assets as supply becomes constrained over time.

Finally, in the New Normal, treasurers need to think not only about preserving capital simply in nominal terms, but also in real, or inflation-adjusted, terms. While the average MMF might offer a more stable return, in inflation-adjusted terms that return is probably negative. Short-term strategies may better help to preserve one’s capital in real terms, for an incremental increase in risk. With a dynamic game plan incorporating these strategies, treasurers could continue to adapt to the changing economic landscape.

Jeff Helsing is a senior vice president and product manager, and Jerome Schneider is an executive vice president and head of the short-term and funding desk at PIMCO, California