Targeting a level of balance sheet leverage is a core strategic decision and managing it successfully has a significant impact on the level of shareholder returns.

This article describes how the multinational corporate, operating and earning money in many different currencies, can efficiently manage the effects of FX movements on its balance sheet leverage. For the purposes of this discussion we will define balance sheet leverage as net debt to EBITDA, as this ratio is fundamental in credit rating agency and lender analysis.

Successfully managing the leverage ratio contributes towards these areas:

The approach many corporates take is to borrow against future cash flows or earnings (often EBITDA), particularly where the business is asset-light in nature and shareholder value is more closely linked to cash-flow generation. Traditionally, the effective currency of debt has been aligned in direct proportion to the levels of earnings or cash.

Translation risk to the leverage ratio poses an interesting problem because cash flows or earnings are translated at the average exchange rate for the period, whereas debt is translated at closing rate. The different exchange rates used to translate the two inputs into the leverage ratio can cause variations in the ratio even if levels of currency debt and EBITDA are delivered exactly to target. The reason is very simple: the average exchange rate used for cash-flow earnings translation is significantly less volatile within an annual reporting cycle than the closing exchange rate used to translate foreign currency denominated debt.

The typical formulation of an overall leverage target will see the corporate plan for an appropriate level of CAPEX, M&A and dividends in conjunction with its forecast operating cash flows and EBITDA. Delivery of this plan is beyond the scope of this discussion. What we examine here is the ability of the corporate to minimise the effect of translation upon the reported leverage ratio by adjusting the effective currency of the debt portfolio.

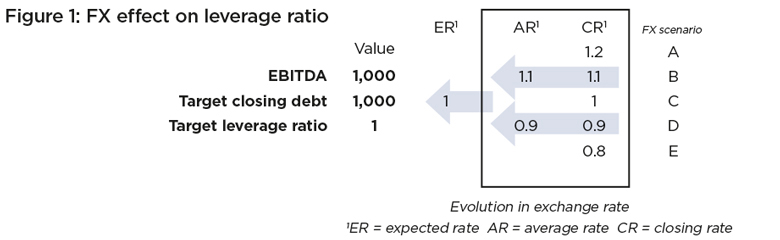

The exposure we are managing in this situation is the impact arising from the average and closing exchange rates being different from the expected exchange rate when the cash-flow plan and the closing leverage target for the year ahead were determined. In the usual financial cycle this would be a spot rate (specifically a forward) around the time that the annual budget or longer-term business plan is finalised.

In Figure 1 we refer to this as the expected rate:

Figure 1 sets up a model that assumes all the corporate’s earning are in foreign currency. The expected exchange rate is one. Using this rate, both EBITDA and target closing debt translate into a reported value of 1,000 giving a leverage ratio of one.

Figure 1 also sets up a crude model of the real world by showing exchange rates moving away from the expected rate by an increment of 10% every six months. This results in an average exchange rate of between 0.9-1.1 of the expected rate and a closing exchange rate within a range of 0.8-1.2.

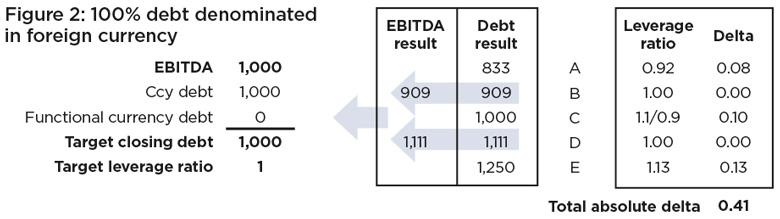

Figure 2 shows what happens when debt entirely in foreign currency is tested through the changing FX rates introduced in Figure 1.

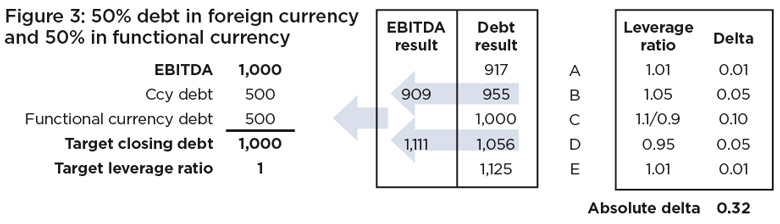

Figure 3 shows the equivalent for a debt portfolio where only half of the debt is denominated in the foreign currency in which EBITDA is earned. The other half is retained in the functional currency of the reporting entity.

Both debt portfolios produce the target leverage ratio of ‘1’ if exchange rates do not change from the expected rate at the start of the year. Reported EBITDA is the same in both Figures 2 and 3; however, the level of reported debt turns out differently given the same closing exchange rate, as the mix of currency debt is different. Comparing the resulting leverage ratios shows that:

Holding only half of the debt portfolio in the same currency that the corporate’s earnings are denominated (Figure 3) produces a lower translation risk to the leverage ratio (as long as the residual is held in the functional currency of the reporting entity). Matching the currency of earnings to debt in the same proportions (Figure 2) introduces more risk into the ratio.

Clearly, across the infinite range of exchange-rate scenarios that can play out over the course of a reporting period, alternative debt portfolios will under- or over-perform versus others. However, the approach discussed allows the corporate to carry out a meaningful analysis of translation risk to its balance sheet leverage.

The corporate can now consider this alongside other factors, such as the interest cost resulting from different mixes of currency within its debt portfolio. Understanding the risk and the tools available to manage it allows management to make informed decisions that, over time, should produce a more stable and targeted reported leverage ratio and benefit the creation of shareholder value.

Ben Walters, FCT, ACA, is a practising corporate treasurer with a keen interest in corporate finance. He has written previously in The Treasurer on capital allocation strategy and can be contacted Scroll to top