Background

The Policy and Technical team continues to speak with treasurers to understand what issues they are facing and in what areas the ACT can help. We are also talking with the main banks to understand how they are responding to the COVID-19 crisis. At the same time, we have held a number of conversations with HM Treasury, the Bank of England, the CBI, the City of London Corporation and UK Finance. Through these forums we have been able to ensure that the views of the treasury community are heard by policymakers through a number of different channels.

A list of useful material from the ACT, the Regulators, the Government and Others can be accessed from the ACT Knowledge Hub - https://www.treasurers.org/hub/technical/covid19

HM Treasury update – 2 November

The deadline for applying to the CLBILS, CBILS and Bounce Back schemes has been extended to 31 January 2021. Firms that have already applied to for Bounce Back loans will be able to top up their existing loans, though this can only be done once.

HM Treasury update – 31 October

The Coronavirus Job Retention Scheme will remain open until December, with employees receiving 80% of their current salary for hours not worked, up to a maximum of £2,500. Under the extended scheme, the cost for employers of retaining workers will be reduced compared to the current scheme, which ends today. This means the extended furlough scheme is more generous for employers than it was in October.

Business premises forced to close in England are to receive grants worth up to £3,000 per month under the Local Restrictions Support Grant. Also, £1.1bn is being given to Local Authorities, distributed on the basis of £20 per head, for one-off payments to enable them to support businesses more broadly.

Mortgage holidays will also no longer end today.

The CCFF scheme

On October 9, the Bank of England issued a Consolidated Market Notice 9.

In line with previous notices, The Bank of England and HM Treasury gave 6 months’ notice of the withdrawal of the facility. The CCFF will close for new purchases of CP from eligible issuers with effect from 23 March 2021. This means that the Facility will make no purchases of CP after 22 March 2021. The CCFF will also close to new applications from counterparties and issuers looking to become eligible on 31 December 2020.

Credit quality: With effect from 9 October 2020 this process will be enhanced. Any eligible issuer wanting to issue new CP into the CCFF after that date will be subject to a review to consider whether that issuance remains in line with the purpose of the facility. (‘New CP’ includes an issuer’s first issue of CP and any subsequent issue of CP, for instance in order to replace maturing CP.)

Where an issuer wanting to issue CP into the CCFF after 9 October has a current credit rating (or equivalent) of investment grade (that is, at or above a short-term rating of A3/P3/F3/R3 or equivalent, or a long-term rating of BBB-/Baa3/BBB-/BBB low or equivalent), it can expect to be able to proceed to issue CP into the CCFF, subject to (i) providing supporting evidence as detailed below and (ii) the issuer’s approved drawing limit.

In cases where an issuer’s credit rating (or equivalent) has fallen below levels deemed equivalent to investment grade, the issuer will have the option to pursue a review on which HM Treasury, as the ultimate risk-owner of the CCFF, will take the final decision. The review will consider whether the issuer’s use of the CCFF remains within the purpose of the facility, which has always been to provide short term liquidity support to fundamentally strong businesses.

In addition, from 9 October any firm whose long-term credit rating falls to, or below, BBB-/Baa3/BBB (low) or equivalent after 1 March 2020 will have their aggregate drawing limit capped at a maximum of £300 million.

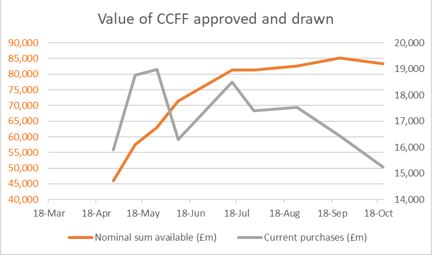

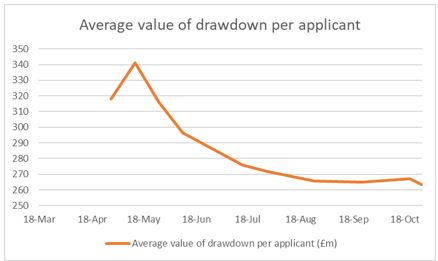

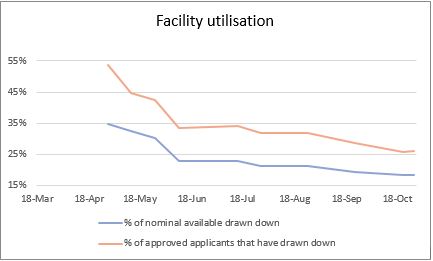

Taken from the Bank of England report, the following table provides some interesting insights (https://www.bankofengland.co.uk/markets/bank-of-england-market-operations-guide/results-and-usage-data).

As the tables above confirm:

Details of current borrowers under the facility can be found at https://www.bankofengland.co.uk/-/media/boe/files/markets/covid-corporate-financing-facility/cp-held-by-ccff-by-business.xlsx.

More information on the programme can be found under https://www.bankofengland.co.uk/markets/covid-corporate-financing-facility.

If you have questions you’d like raised with the Bank of England, please email technical@treasurers.org

We are starting to hear from firms that have been able to access the CCFF programme; we provide anonymised feedback to the Bank of England. If you’d like to share your experiences, please drop an email to technical@treasurers.org.

Other Schemes

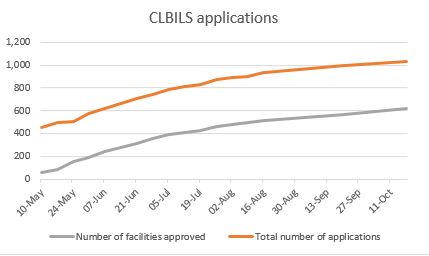

On September 24, the Chancellor of the Exchequer extended the government’s three Coronavirus business interruption loan schemes and the Future Fund. The extension aligned all the end dates of the schemes to 30 November.

In addition, it was announced on September 25 that businesses applying for the CBILS or CLBILS will benefit from more flexibility on the date the test of whether or not their business is an ‘undertaking in difficulty’ is assessed.

The new guidance allows for the ‘undertaking in difficulty’ assessment to be determined at the date of application for the schemes. Businesses that were ‘undertakings in difficulty’ on 31 December 2019 but are no longer ‘undertakings in difficulty’ will now be (in principle) eligible for the schemes. This flexibility means that businesses can take action to convert their debt (for example, in the form of loan notes) to shares (equity) in order to qualify for the schemes, giving them the option to restructure their finances before application so they may become eligible.

The Bank has also made available details of the other schemes being made available https://www.gov.uk/government/collections/hm-treasury-coronavirus-covid-19-business-loan-scheme-statistics#Coronavirus-Business-Interruption-Loan-Scheme

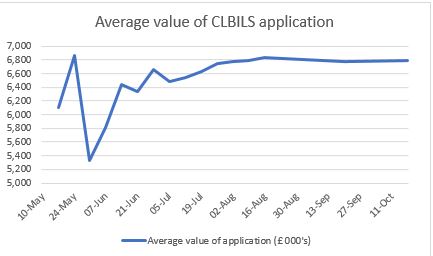

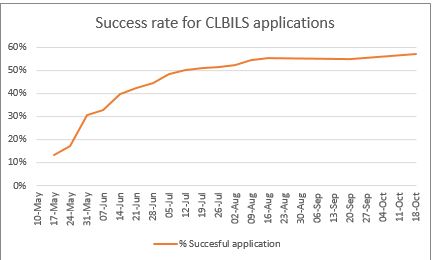

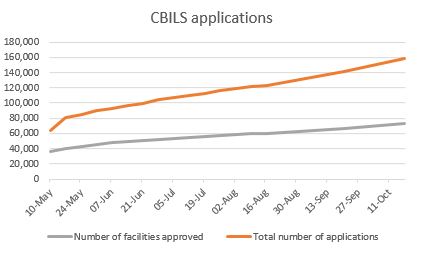

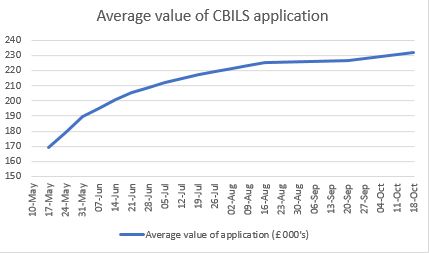

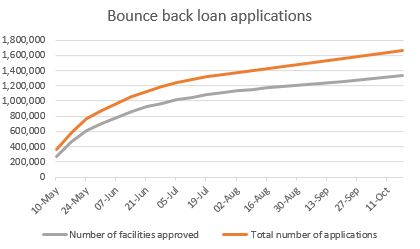

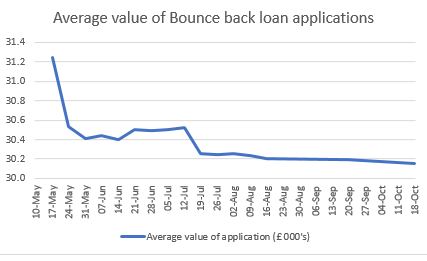

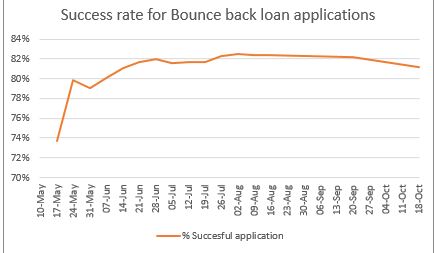

The data shows that:

The British Business Bank has started to release details of the take up of the schemes it administers split by:

Update from the UK regulators

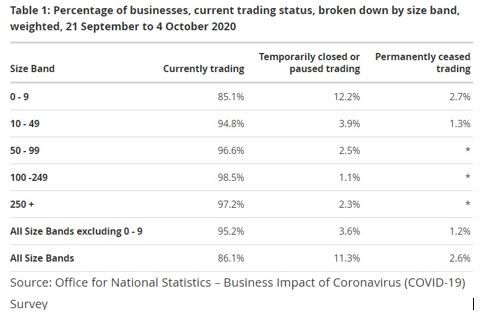

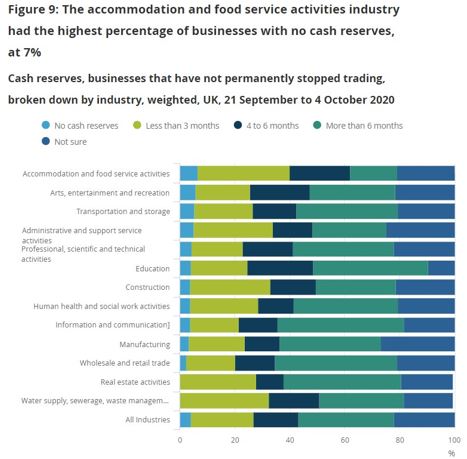

The ONS produces a fortnightly analysis of business responses in a number of key areas. The latest report noted:

It also provided the following tables:

Of businesses who had not stopped trading, the percentage reporting having no or less than six months cash reserves remained stable at 43% and the percentage reporting having more than six months cash reserves remained stable at 35%.

It should be noted that the survey population tends to be small businesses.

Feedback from Treasurers

The slight decrease in the number of active borrowers under the CCFF scheme reflects comments we have heard from treasurers who have reported repaying government loans and, in some cases, repaying furlough related payments they received.

Views from across the world

As a member of the International Group of Treasury Associations, and the European Association of Corporate Treasurers and working with our colleagues in the US National Association of Corporate Treasurers we are keeping an eye on developments overseas.

The Federal Reserve Bank of the United States of America announced changes to the rules of its Main Street Lending Program to help smaller businesses that have been struggling to get by while waiting for additional stimulus from Congress by announcing that it would issue loans as low as $100,000 and reduce the fees for the loans. Previously the minimum amount it would lend was $250,000.

Engaging with the treasury community

We welcome conversations with our members on:

Send an email to technical@treasurers.org and either James Winterton, Naresh Aggarwal or Sarah Boyce will be in touch with you.

If you have found any resources which you feel we should add to our COVID-19 site, please email us with details.

Naresh