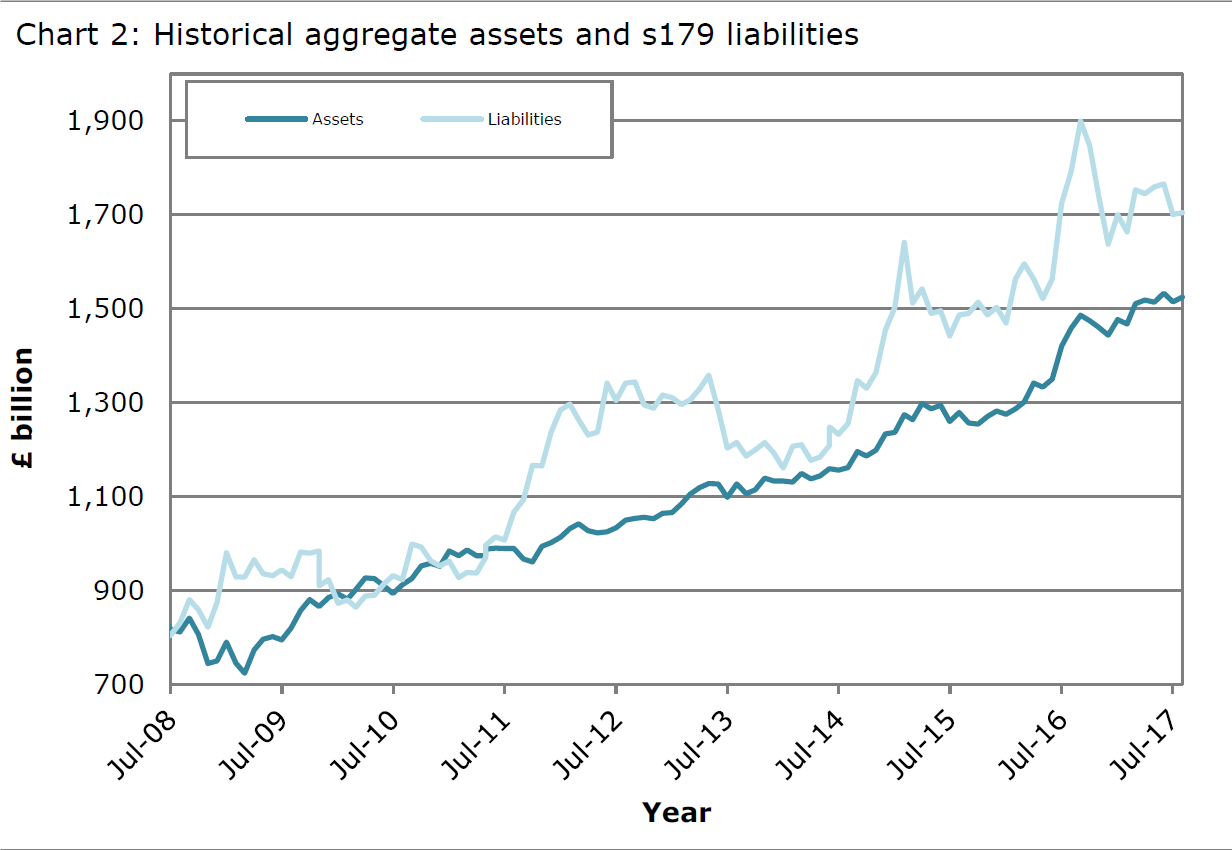

This month’s PPF 7800 index (1) revealed an aggregate deficit of £180bn for the defined benefit (DB) pension schemes within its sphere, at 31 July 2017. Although this is a significant level, it compares favourably with the deficit position at July 2016 (2), when the level was £333bn.

Funding comparisons

| July 2016 | June 2017 | July 2017 | |

| Aggregate balance | -£333.5bn | -£186.2bn | -£180.1bn |

| Funding ratio | 81.4% | 89.1% | 89.4% |

| Aggregate assets | £1,458.4bn | £1,514.6bn | £1,524.7bn |

| Aggregate liabilities | £1,791.8bn | £1,700.8bn | £1,704.8bn |

| Data set / assumptions | Purple 16 – A7 | Purple 16 – A8 | Purple 16 - A8 |

The improvement in the deficit funding level is down to a reduction in liabilities of £108bn and an increase in the level of assets of £124bn. Lower liabilities were primarily due to a decrease in the assumed inflation expectations, resulting from changes in the published yields for conventional and index linked gilts, which are used to set assumptions. The increase in the value of assets of the 5,794 schemes, which make up the index, results principally from changes in the value of equity and bond markets. This is attributable to the high level of assets allocation in bonds and the high level of volatility, this being a feature of equity markets. An increase in special pension contributions has also helped to improve the funding position.

That said, further scrutiny of the deficit position reveals a different picture. If the schemes in deficit are considered in isolation, a concerning picture materialises. There are currently 4,156 schemes in deficit, which is 678 lower than at the end of August 2016. The level of deficit is calculated to be £258bn, which is £193bn lower than reported in August 2016. A further breakdown shows that although liabilities are calculated to be £360bn lower, assets have fallen by £167bn.

Thus, more cash may be required to be paid into these schemes. The trend is for reducing active membership of these legacy DB pension schemes. The effect is to reduce the opportunity for employers to claw money back from employees. Consequently, scheme sponsors will have to consider other alternatives to reduce pension deficits.

For those scheme sponsors with large pension deficits, the impact on cash flow could be significant. Treasurers will need to give careful consideration to liquidity as well as headroom and availability of alternative funding lines.

Going forward, there are storm clouds on the horizon, Brexit being the darkest of all.

Over the next couple of years, treasurers will be considering the impact and the pressure caused by the uncertainty of Brexit on their companies risk management plans. The possible increases in volatile pension deficits will make future investment planning even more difficult.

Notes

(1) PPF 7800 measures the funding position for around 5,800 defined benefit pension schemes, a section 179 basis.

(2) There are slight differences in the deficit valuations for August 2016 and July 2017, as a result of changes to the data set, with the former based on the Purple Book 2015 and the latter on more up to date information in the Purple Book, published in November 2016.

About the author

Mary Finn is a Fellow of the ACT. She is currently an independent treasury consultant, specialising in corporate cash management solutions. She has a keen interest in pension schemes, having previously been the company secretary and a trustee board member for her previous employer’s hybrid pension scheme.