This article was written by Amanda Iacone from Bloomberg Tax. It appeared first on the Bloomberg Terminal.

Innovations like data analytics and automation aren’t reaching corporate finance as quickly as CFOs and controllers would like, prompting them to make a big tech push in 2019.

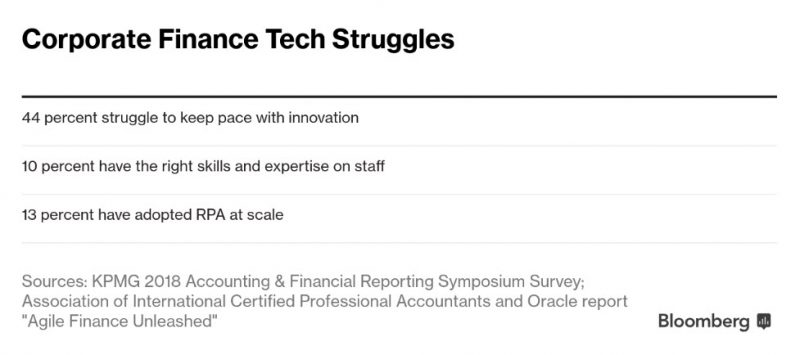

Just 13 percent of controllers and chief financial officers say their teams use robotics process automation. An even smaller group—10 percent—say they have the right skills on their teams to adopt and use emerging technologies, according to a recent joint survey by the Association of International Certified Professional Accountants and Oracle Corp.

The Institute of Management Accountants found in another of several surveys and reports released in the last month that less than 9 percent of members worldwide had met their goal of rolling out advanced data analytics tools and techniques. But nearly 60 percent were actively working to adopt them.

Almost half of financial reporting executives said they aren’t keeping pace with technology innovations, according to a KPMG LLP survey. However, 70 percent said that they had invested in financial reporting technology in the past year.

Controllers and CFOs are aware they are lagging behind. “They’ll readily admit they’re not as far as they would like,” said Chris Westfall, vice president of content strategy for Finance Executives International. “Corporate finance is trying to figure out a way to catch up to the other aspects of the business.”

Investing in tools like robotics process automation and advanced analytics is a top priority for CFOs in 2019—above implementing significant accounting rule changes, mergers, and other business needs, Westfall said.

The accounting profession has struggled to adapt to new tools and technologies that will replace the often tedious, time-consuming checks and processes that accountants have routinely handled. Those tools are expected to free accountants to spend their time on more complex analysis, which advocates hope will provide better insights that would help a company’s bottom line.

For corporate finance, new technology could automate financial controls, allow accountants to focus on areas of higher risk, and offer avenues for more effective auditing. Combined, that could result in more reliable financial statements, said Roger O’Donnell, a KPMG partner and the firm’s global head of data and analytics for audit.

“Technology is changing the landscape of financial reporting and by inference, then, the external audit and what we’re able to do,” O’Donnell said.

Audit firms have invested heavily in emerging technology, including cloud-technology, RPA, machine learning, and data visualization tools.

But putting those new tools to work depends entirely on the client’s own systems and whether they can produce the type of information the auditors need, O’Donnell said.

Auditors have more advanced technology than their clients at this point, said Ash Noah, managing director of learning, education and development for chartered global management accountants for the Association of International Certified Professional Accountants.

Challenges

The AICPA-Oracle report was a check-up two years after a similar survey. It found that not much has changed—while some companies advanced their technical capabilities, others haven’t, Noah told Bloomberg Tax.

Established companies like big banks and airlines invested millions into legacy finance systems and the policies and processes that go with them. Upgrading to cloud-based enterprise resource planning systems is no small task and remains among the biggest hurdles to adopting new technology, Noah said.

Shifting to the cloud represents a giant technological leap forward, and a crucial first step to unlock advanced data analytics, automation and new ways of doing business. The cloud changes the way data can be used and makes it easier to layer on new innovations, Noah said.

The skills gap remains another challenge—a shortage of people in finance and accounting who can apply math and statistics to the mountain of data that companies collect. CFOs are trying to figure out how to build those skill sets into their workforce, he said.

This article is reproduced from the Bloomberg’s Professional Services blog, and is licensed by The Association of Corporate Treasurers.