The payments landscape continues to evolve and this blog shares some of the topics that caught my attention during the last month. If you think I’ve missed anything important, do please send an email to technical@treasurers.com.

Central Bank Digital Currencies (CBDCs) and other digital currencies

It is becoming increasingly difficult to keep up with all of the announcements from a raft of central banks and think tanks but here are some that caught my attention:

- The BIS has published its third survey on CBDCs. Key findings include:

- Central banks collectively representing a fifth of the world’s population are likely to issue a general purpose CBDC in the next three years

- Some central banks with advanced CBDC projects are becoming more cautious about issuance timeframes while assessing their work

- A growing awareness of the cross-border implications that CBDCs can have for the financial system has spurred international collaboration between central banks to find common ground on policy

- Over the last four years, the share of central banks actively engaging in some form of CBDC work grew by about one third and now stands at 86%

- About 60% of central banks (up from 42% in 2019) are conducting experiments or proofs-of-concept, while 14% are moving forward to development and pilot arrangements

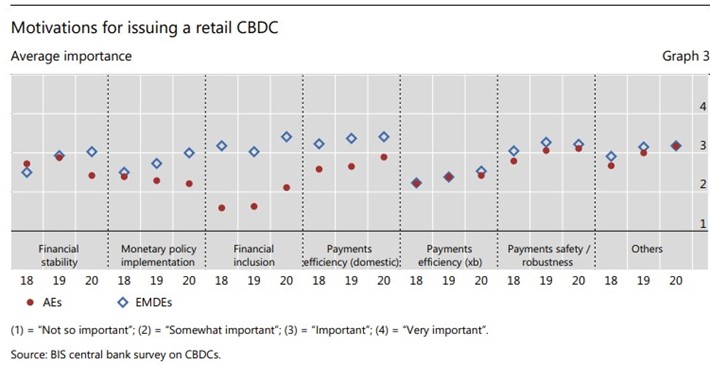

- Emerging market and developing economies (EMDE) report stronger motivations for issuing CBDC than advanced economies (AE) (Graph 3). Financial inclusion emerges as a main factor across EMDEs and remains a top priority for CBDC development. The Sand Dollar was introduced in the Bahamas to help facilitate financial inclusion in this nation of 390,000 people spread across 30 inhabited islands, many of them remote.

- Met Life Investment Management has produced a useful primer on cryptocurrencies that covers a wide range of currencies and notes:

- Blockchain, a revolutionary way of transmitting information trustlessly through time, has captured the imaginations of software developers, economists, and now, central bank policymakers worldwide. Blockchain is a version of distributed ledger technology, a system whose fundamental structure dates back hundreds of years to the Micronesian island of Yapi

- Stablecoins have emerged as a new way to transact value in the cryptocurrency space. Instead of being claims on network equity, such as Bitcoin, existing stablecoins seek to mimic the price of real-world assets, such as the United States Dollar (USD). A central bank digital currency (CBDC) would effectively be a class of stablecoin.

- Motivations for creating CBDCs include an interest in furthering financial inclusion globally, impeding criminal use of cash, improving electronic payments infrastructure, enhancing policy tools, and, in the case of the United States, strengthening the reserve status of the U.S. Dollar. Other CBDCs are likely attempts to offer a different reserve currency option.

- A true CBDC launch among Western countries seems unlikely to occur anytime soon. The head of the European Central Bank, Christine Lagarde, suggested that it could take anywhere from two to four years.

- China is expected to be the first major sovereign power to implement a large scale CBDC initiative, further expanding the footprint of its digital economy and potentially laying the foundation for at least partial yuanization of countries along the Belt and Road.

- The next G7 meeting on 12 February will include a discussion on CBDCs

- At the World Economic Forum, the Governor of the Bank of England claimed that existing virtual currencies are unlikely to last and the high degree of volatility associated with speculative cryptocurrencies is where CBDCs may have a significant advantage.

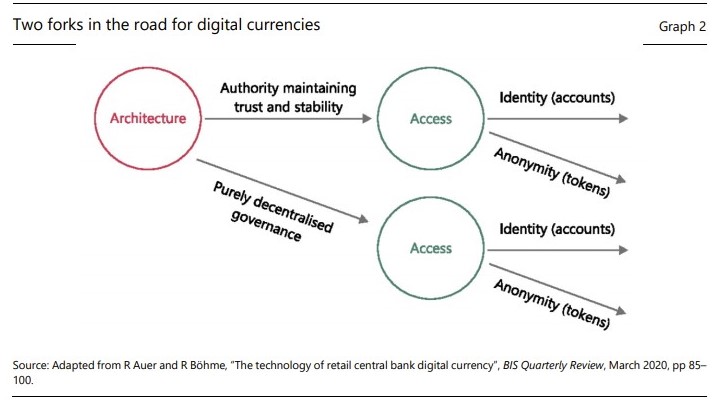

- In a recent speech by the BIS General Manager on digital currencies and the future of the monetary system, he discussed, among other things, whether digital currencies should rely on a central or decentralised authority and whether verification should be based on identity or cryptography. He argued that if digital currencies were needed, they should be issued by central banks and that private stablecoins, even if heavily regulated, cannot serve as the basis for a sound monetary system.

Interesting reports

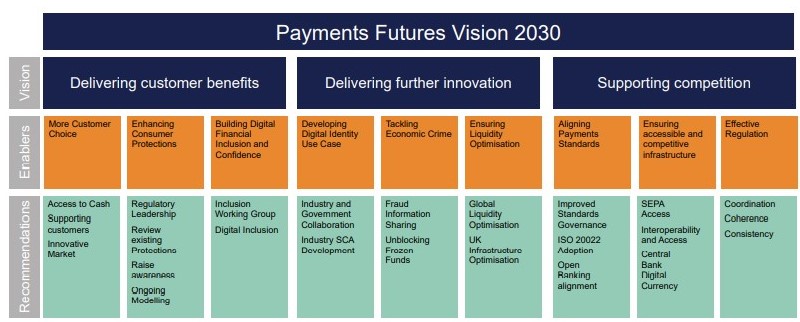

UK Finance, in conjunction with PwC issued a report on payments – Future Ready Payments 2030. This includes the following vision for payments:

The DCC Forum has written an analysis of the Cross-Border Payments EU Regulation (2019/518). The aim of the regulation is to bring greater transparency and understanding to cross-border card payment payments among EU countries.

UK payments landscape

- The UK government announced an overhaul of the Prompt Payment Code under which companies that have signed up to the Prompt Payment Code will be obliged to pay small businesses within 30 days - half the time outlined in the current Code. In addition, businesses owners, Finance Directors or CEOs will be required to take personal responsibility by signing the Code, acknowledging that suppliers can charge interest on late invoices under the Code and that breaches will be investigated. Those signed up to the Code will redouble their efforts to ensure payments are made on time and breaches will continue to be publicised by the government in order to encourage compliance.

- The PSR launched a consultation on ways to reduce risks to the successful renewal of the UK’s interbank payment systems and proposals to mitigate risks to competition and innovation. It is concerned about risks to competition and innovation relating to when the NPA is operational, and how this may affect the quality, range and pricing of payment services delivered using the NPA. Any comments should be sent to PSRNPA@psr.org.uk. The following deadlines apply:

19 March 2021 - deadline for comments on questions 1 to 6 of our consultation (and other comments on risks to the delivery of the NPA and options for reducing these).

5 May 2021 - deadline for comments on questions 7 to 14 of our consultation (and other comments on competition and pricing).

- In January 2020, the PSR issued a Call for Input on potential risks to competition and innovation in the UK’s New Payments Architecture. A number of responses were received.

- The FCA has identified barriers to the success of open banking and future innovation in UK payments. To address these, it is proposing amendments to the Technical Standards on Strong Customer Authentication and Common and Secure Methods of Communication. It is also taking this opportunity to amend its guidance on prudential risk management and safeguarding in its Approach Document (AD), and make general updates to a number of areas and onshoring-related changes. It is proposing the following:

- ASPSPs need no longer require their customers to perform SCA every 90 days when the customer uses a TPP to provide account information services (AIS), although SCA will be required when customers first connect their account to that service.

- AISPs will continue to be able to access a customer account without the customer’s active request to do so, up to four times a day, but will now need to reconfirm the customer’s explicit consent every 90 days.

- The use of dedicated interfaces, rather than modified customer interfaces (MCIs), will be mandatory for personal current accounts, accounts that would fall under the definition of payment accounts within the meaning of the PARs but that are held by SMEs, and credit card accounts held by consumers or SMEs.

One section of the Consultation, relating to contactless payments, will close on 24 February 2021. The rest will close on 30 April 2021.

- UK Finance has proposed an increase in the contactless payments limit from £45 to £100. This would require approval from HM Treasury as well as the Financial Conduct Authority. This would form a break with current EU arrangements.

Naresh Aggarwal