The payments landscape continues to evolve and this blog shares some of the topics that caught my attention during the last month. If you think I’ve missed anything important, do please send an email to technical@treasurers.com.

Central Bank Digital Currencies (CBDCs) and other digital currencies.

It is becoming increasingly difficult to keep up with all of the announcements from a raft of central banks and think tanks but here are some that caught my attention:

- The Bank for International Settlements recently issued an update on progress since its October 2020 report. Key messages included:

- any CBDC system would need to involve both public and private actors to ensure interoperability and coexistence with the broader payment system

- involving both public and private actors would help a CBDC to anticipate the needs of future users and incorporate related innovations

- to help maintain safety and stability, a CBDC would need careful design and implementation, allowing time for the existing financial system to adjust and flexibility to use safeguards

- The G7 published a set of Public Policy Principles for Retail Central Bank Digital Currencies (CBDC) alongside a G7 Finance Ministers and Central Bank Governors’ Statement on CBDCs and digital payments. Key messages included:

- Any CBDC should be designed such that it supports the fulfilment of public policy objectives, does not impede the central bank’s ability to fulfil its mandate and ‘does no harm’ to monetary and financial stability

- G7 values for the International Monetary and Financial System should guide the design and operation of any CBDC, namely observance of the rule of law, sound economic governance and appropriate transparency

- Rigorous standards of privacy, accountability for the protection of users’ data, and transparency on how information will be secured and used is essential for any CBDC to command trust and confidence.

- To achieve trusted, durable, and adaptable digital payments any CBDC ecosystem must be secure and resilient to cyber, fraud and other operational risks

- CBDCs should coexist with existing means of payment and operate in an open, secure, resilient, transparent and competitive environment that promotes choice and diversity in payment options

- Any CBDC needs to carefully integrate the need for faster, more accessible, safer and cheaper payments with a commitment to mitigate their use in facilitating crime

- CBDCs should be designed to avoid risks of harm to the international monetary and financial system, including the monetary sovereignty and financial stability of other countries

- The energy usage of any CBDC infrastructure should be as efficient as possible to support the international community’s shared commitments to transition to a ‘net zero’ economy

- CBDCs should support and be a catalyst for responsible innovation in the digital economy and ensure interoperability with existing and future payments solutions

- Authorities should consider the role of CBDCs in contributing to financial inclusion. CBDC should not impede, and where possible should enhance, access to payment services for those excluded from or underserved by the existing financial system, while also complementing the important role that will continue to be played by cash

- Any CBDC, where used to support payments between authorities and the public, should do so in a fast, inexpensive, transparent, inclusive and safe manner, both in normal times and in times of crisis

- Jurisdictions considering issuing CBDCs should explore how they might enhance cross-border payments, including through central banks and other organisations working openly and collaboratively to consider the international dimensions of CBDC design

- Any CBDC deployed for the provision of international development assistance should safeguard key public policies of the issuing and recipient countries, while providing sufficient transparency about the nature of the CBDC’s design features

- In a recent speech at SIBOS, Sir Jon Cunliffe - Deputy Governor of the Bank of England for Financial Stability discussed how regulators are looking at unbacked crypto-assets (e.g. Bitcoin) and backed crypto-assets for payments (stablecoins) which have begun to connect to the financial system.

- Minutes of the first meeting of the Bank of England’s CBDC Technology Forum were released

- An independent forum supporting the implementation of a digital pound has been established. The Digital Pound Foundation has been launched to support the implementation of a well-designed digital Pound and digital money ecosystem.

- The Central Bank of Nigeria (CBN) formally introduced eNaira, a pilot retail central bank digital (CBDC) currency on 25 October. The CBN has taken a platform approach to the CBDC’s design using a centralised blockchain ledger controlled by the central bank that logs all transactions and uses enterprise blockchain Hyperledger Fabric. Banks and payment service providers process retail payments and enable other payment services.

- Oliver Wyman and JP Morgan have produced a recent report that estimates savings in excess of $100bn with the widespread deployment of CDBCs

- The Economic Affairs Committee of the House of Lords in the UK recently discussed the purpose and outcomes of CBDCs including encouraging the use of alternatives to the US dollar as a global reserve currency

- The European Central Bank announced the 30 members of its Digital Euro Market Advisory Group.

- McKinsey issued a report focusing on the coexistence of CBDCs and stablecoins.

Interesting reports

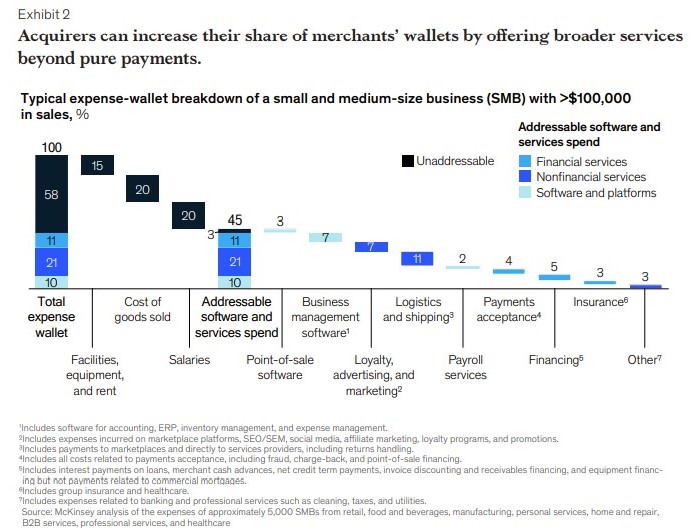

McKinsey has released its 2021 Global Payments Report. It includes the following diagram which shows that payments providers serving SMBs have started to organise their products, services, and go-to-market approach by industry and using the convergence of payments and software, has enabled merchant acquirers to deliver integrated solutions.

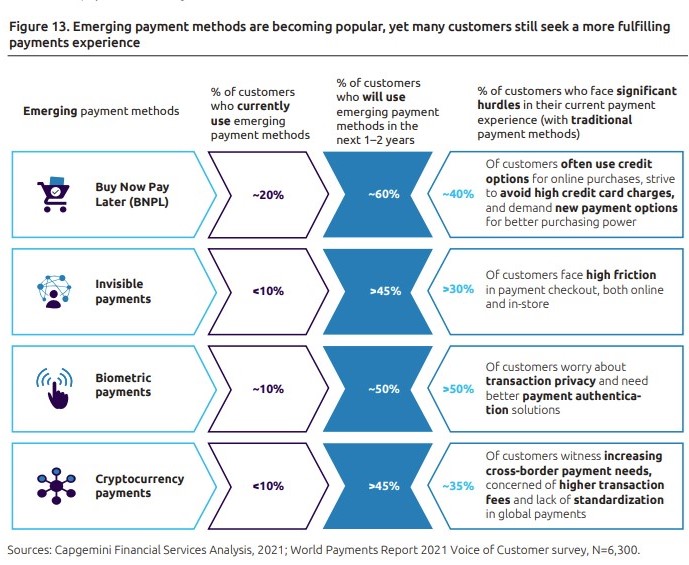

Capgemini released its 2021 World Payments report. The 48-page report includes the following figure which forecasts payment trends.

BCG has issued a report on Global Payments. It identifies five key trends:

- Deeper payments integration with companies to embed payments systems in an increasing number of platforms, workflows, and customer-facing offerings

- More active bank engagement as banks increasingly view merchant acquiring and other payments activities as a strategic source of reliable revenues and rich streams of customer data

- Faster pace of digital currency activity as mainstream interest in digital currencies grew significantly during 2020 with crypto asset trading becoming more prevalent on consumer financial apps and Bitcoin’s valuation reaching historic highs.

- Regulatory emphasis on open banking and payment infrastructure as regulators globally promote economic growth by removing encrusted structures that favour established players and make it harder for innovative offerings to come to market. In Europe, the European Banking Association hopes to promote greater use case development by conducting an API audit of banks in the region. Brazil’s central bank has introduced one of the world’s most comprehensive frameworks and set aggressive implementation targets, with banks expected to complete most of the new data aggregation requirements by the end of 2021. China’s recent introduction of data privacy laws aimed at protecting consumers’ data should help international companies run data-sharing relationships more smoothly. In the US financial authorities have recently begun developing regulatory frameworks for open banking, and private entities such as Plaid and Finicity have developed platforms that enable open-banking connectivity.

- More industry consolidation and M&A as leaders are using their strong position in one part of the value chain to acquire toeholds in others.

UK payments landscape

- The Payment Systems Regulator (PSR) published its final report into its card-acquiring market review. Key findings included:

- The supply of card-acquiring services does not work well for small and medium-sized merchants and large merchants with annual card turnover up to £50 million.

- Merchants with annual card turnover between £15,000 and £50 million served by the five largest acquirers got little or no pass-through of the Interchange Fee Regulation (IFR) savings.

- Many small and medium-sized merchants do not regularly search, consider switching provider, or negotiate with their current provider. This is despite evidence that they could achieve a better deal by doing so.

- The final report identified three features that restrict merchants’ willingness and ability to search and switch:

- Acquirers and independent sales organisations (ISOs) don’t typically publish their prices and their pricing structures and approaches to headline rates vary significantly making it difficult to compare prices for ISOs, acquirers and payment facilitators

- The indefinite duration of acquirer and payment facilitator contracts for card-acquiring services does not provide a clear trigger for merchants to think about searching for another provider and switching

- POS terminals and POS terminal contracts can prevent or discourage merchants from searching and switching provider of card-acquiring services. This can occur as a merchant may need a new POS terminal if it switches provider of card-acquiring services but it could incur a significant early termination fee cancelling its existing POS terminal contract.

The PSR said it would also examine how scheme fees have changed over the period 2014 to 2018. The regulator’s analysis indicates that scheme fees increased significantly over the period and a substantial proportion of these increases are not explained by changes in the volume, value or mix of transactions.

The PSR is also aware of recent announcements by Visa and Mastercard about increases in certain card fees, focused on cross-border transactions. These have happened as previous regulatory constraints have been removed since the UK left the EU. The PSR is very clear that the absence of specific regulatory caps is not itself a sufficient reason to increase fees, particularly if those increases are not obviously linked to costs.

- The PSR issued its response to a consultation paper on Confirmation of Payee. It noted that Phase 1 had had a positive impact, both in terms of reducing accidentally misdirected payments and in preventing what would have likely been a larger increase in Authorised Push Payment (APP) scams, in light of COVID-19 and the increased manipulation of victims by fraudsters. It was also felt to have mitigated payment risk and strengthened consumer confidence in digital payments. However, it also found that:

- there continued to be a migration of the relevant types of APP scams towards institutions that have not yet implemented CoP creating opportunities for fraudsters to target firms not offering the service

- there had been increased social engineering of victims by fraudsters to convince customers to ignore ‘no match’ warnings. In some cases, fraudsters had used the added level of confidence offered by CoP to manipulate victims into sending money to mule accounts

- the presence by the SD10 banks (Specific Direction 10) in Phase 2 (accounting for 90% of transactions across Faster Payments and CHAPS) would be key to enabling prospective participants to progress their plans to join CoP and ensure interoperability for new participants.

- The Bank of England issued its CHAPS and RTGS Annual Report. Key messages included:

- Renewed: Delivery phase includes: ISO 20022 like-for-like for CHAPS payment messages in June 2022; ISO 20022 enhanced in February 2023; and then a new core ledger for RTGS in autumn 2023.

- As part of the move to ISO 20022, published market guidance for property payments and are working on guidance for corporate payments.

- Complete design activity around settlement, liquidity management and account structure functionality.

- Consult on functionality for inclusion in Transition State 4 – a series of additional enhancements for the RTGS service

Global payments landscape

- The European Banking Authority has recently published a consultation paper in which it is seeking comments on proposed changes to the Regulatory Technical Standards on strong customer authentication (SCA) and common and secure communication (CSC) (the RTS) which are meant to make SCA less intrusive in relation to account information services (AIS), and therefore account information service providers (AISPs) more successful.

The FCA proposed earlier in 2021 that the SCA of the customer by the ASPSP would only be required when the customer first decides to connect their account to an AISP (but will no longer be required on every access, or even every 90 days if the Account Servicing Payment Service Provider (ASPSP) makes use of the exemption – the 90-day exemption would only remain for direct access by the PSU to its payment accounts, e.g. via the mobile banking app provided by the ASPSP to the customer).

If the AISP makes use of the right to perform background refreshes, the AISP will need to reconfirm the customer’s explicit consent every 90 days. If a customer fails to re-confirm their consent, the AISP would be required to disconnect access and stop collecting data from the customer’s payment accounts.

Naresh Aggarwal