Background

The Policy and Technical team continues to speak with treasurers to understand what issues they are facing and in what areas the ACT can help. We are also talking with the main banks to understand how they are responding to the COVID-19 crisis. At the same time, we have held a number of conversations with HM Treasury, the Bank of England, the CBI, the City of London Corporation and UK Finance. Through these forums we have been able to ensure that the views of the treasury community are heard by policymakers through a number of different channels.

A list of useful material from the ACT, the Regulators, the Government and Others can be accessed from the ACT Knowledge Hub.

Please continue to answer the 3 quick questions in our “temperature check” so that we can share with you the trends week on week. View last week's results here.

General overview

As businesses start to reopen, treasurers have been considering what it means to their organisations and their own teams. Many feel that treasury will be amongst the last teams to re-enter offices and key factors will include:

- Can my team travel to work without the use of public transport; and

- Will schools be open and childcare arrangements adequate.

Although many treasurers have identified “blue teams” and “red teams”, it seems that in practice many will operate an all or nothing approach (subject to personal circumstances).

We have also been hearing more talk about LIBOR reform and Brexit which suggests that treasurers are moving from fire-fighting to other important issues. A number are dusting off their no-deal Brexit plans.

The CCFF scheme

The ACT held a very informative discussion with the Bank of England last week over the operations of the CCFF programme. We provided feedback from the treasury community on a number of issues and the Bank shared the following information:

- The criteria for access to the facility are set by HMT with advice from the Bank

- Other than the undertaking and confidentiality agreement between the Bank and the issuer (and the documents which that agreement incorporates) and the issuer eligibility form, the other CCFF-related documentation is entered into between the issuer and the dealer or the dealer and the Bank (except in certain circumstances e.g. where a guarantee is required or the issuer is required to provide a conditionality letter). Access to, and participation in, the scheme is still subject to the terms and conditions set out in other documents, such as the Market Notice.

- A conditionality letter is only required in certain scenarios – effectively meaning that any conditionality process run in parallel to but does not form a part of any CCFF application process. More details are available in question A7 here.

- The Bank continues to review the decisions of rating agencies with information from Credit Benchmarks and HMT and the Bank look for firms to be consistently rated as investment grade across rating sources. HM Treasury and the Bank reserve the right, in their sole discretion, to deem any issuer ineligible after taking into account all available information. More details are available in question B2 here.

- Unless otherwise stated, the facility will close to new issuers on 31 December 2020.

- The Bank will provide 6 months’ notice of the withdrawal of the facility. Further details on these and other linked points can be found in ‘length of facility’ section here.

More information on the programme can be found under https://www.bankofengland.co.uk/markets/covid-corporate-financing-facility. Additional detail is available via the related links in the top right-hand corner of this main CCFF web-page.

If you have questions you’d like raised with the Bank of England, please email technical@treasurers.org.

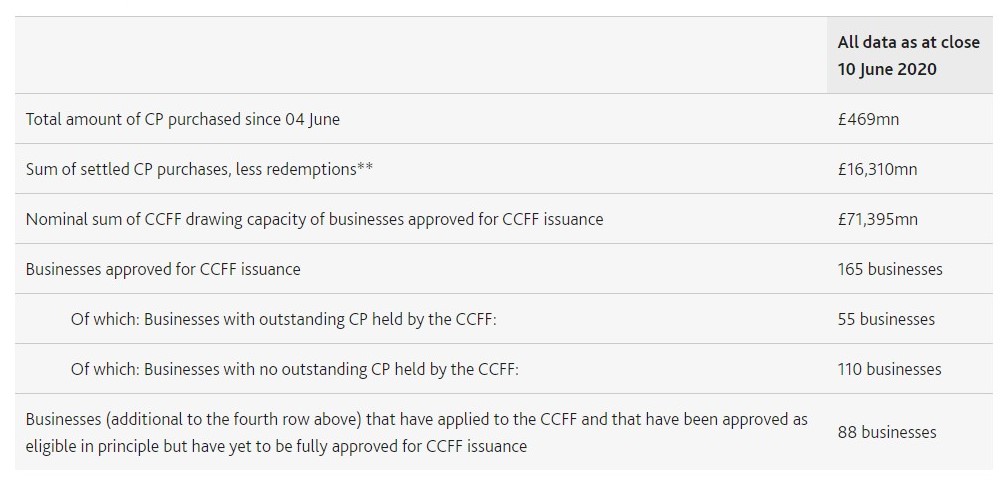

Taken from the Bank of England report, the following table provides some interesting insights (https://www.bankofengland.co.uk/markets/bank-of-england-market-operations-guide/results-and-usage-data).

The data shows that only 33% of applicants to the CCFF facility have currently drawn on this facility (down from 43% at 27 May) and whilst the notional sum of drawing capacity has increased from £62,975mn (a 13% change), the actual amount currently outstanding has decreased from £18,979m (a 14% change).

This continuing trend of increasing facilities available but a decreasing amount of funding drawn supports the conversations we’ve had with treasurers who have applied for the facility as a back-up to their existing financing arrangements or to support additional borrowings from existing lenders. We know that some treasurers prefer to access their own private financing arrangements given that details of borrowers is now being made public every Thursday (https://www.bankofengland.co.uk/-/media/boe/files/markets/covid-corporate-financing-facility/cp-held-by-ccff-by-business.xlsx).

We are starting to hear from firms that have been able to access the CCFF programme; we provide anonymised feedback to the Bank of England. If you’d like to share your experiences, please drop an email to technical@treasurers.org.

Other Schemes

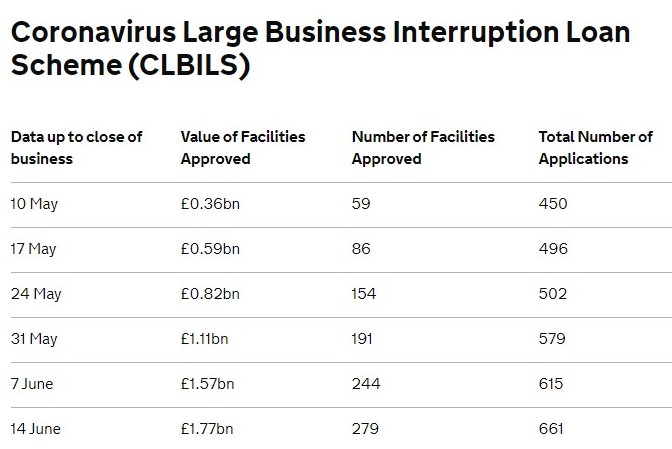

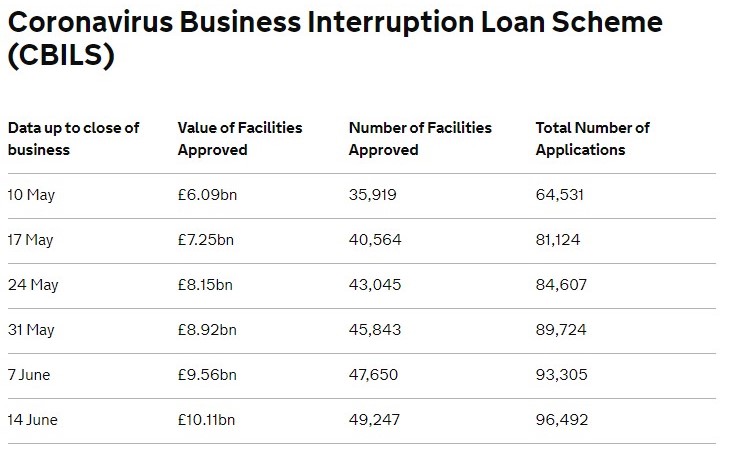

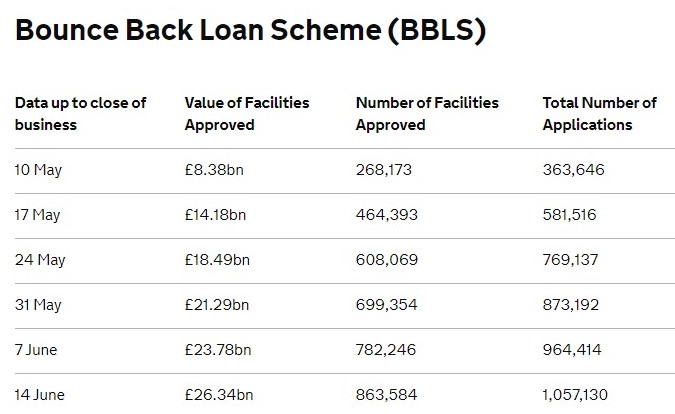

The Bank has also made available details of the other schemes being made available (https://www.gov.uk/government/collections/hm-treasury-coronavirus-covid-19-business-loan-scheme-statistics#Coronavirus-Business-Interruption-Loan-Scheme ).

The tables below show an extract from this and it shows that:

- The average value of a CLBILS facility has steadily increased to £6.3m

- The average value of a CBILS facility has steadily increased to £0.2m

- There have been 176 times as many applications for CBILS compared with CLBILS

- Although the average value of the Bounce Back Loans was only £30,430, the value of approved facilities was almost as large as the other three schemes in aggregate

Update from the UK regulators

- Jon Cunliffe, Deputy Governor for Financial Stability at the PRA delivered a speech on the impact of COVID-19 as a stress test on the financial sector and outlined that the Financial Stability Board can be a platform to determine whether more financial resilience is needed in the wake of the pandemic.

- The BoE published an analysis of the role of margin as a safeguard against counterparty credit risk during the COVID-19 pandemic.

- Chris Woolard, Interim Chief Executive of the FCA, discussed how the Authority has prioritised work in the face of the COVID-19 pandemic, underlining interventions in business interruption insurance as a key priority and highlighting the importance of timely reporting of financial information.

- The Financial Reporting Council published updated guidance on Annual General Meetings for companies in light of COVID-19

- The BoE published an overview of how COVID-19 impacts the economy and inflation through increased uncertainty.

- The BoE and PRA published a joint-statement in response to the ESRB’s recommendations on distribution restrictions, outlining measures taken to suspend dividend distribution during the COVID-19 pandemic.

- The Government announced that it will provide guarantees of up to £10 billion to Trade Credit Insurance schemes for B2B transactions, to help protect businesses from customer defaults and payment delays.

- Sam Woods, Deputy Governor of the BoE for Prudential Regulation and CEO of the PRA wrote to CEOs of UK banks and building societies setting out further guidance on treatment of COVID-19-related payment deferrals under IFRS 9 and CRR.

- John Cunliffe, Deputy Governor for Financial Stability at the BoE, wrote a letter to Financial Market Infrastructures (FMIs) on profit distribution in response to COVID-19 outlining that FMIs are expected to pay attention to additional risks and operational demands arising from COVID-19 and notify the BoE in advance of distribution to shareholders.

- Andrew Hauser, Executive Director of Markets at the BoE, delivered a speech outlining steps taken by the Bank to mitigate COVID-19 liquidity shortages and maintain financial stability. He noted that the Financial Policy Committee in future plans to assess why intermediaries faced difficulty during the crisis, review the role and stability risks of non-banks in financial markets, assess how to address stability risks from money market runs and ensure a timely transition from LIBOR.

- The BoE published its Monthly Decision Maker Panel survey for May, highlighting that firms expect Q2 sales to be 42% lower than expected while business uncertainty related to COVID-19 has fallen since April into May.

Views from across the world

As a member of the International Group of Treasury Associations, and the European Association of Corporate Treasurers and working with our colleagues in the US National Association of Corporate Treasurers we are keeping an eye on developments overseas.

- Fabio Panetta of the ECB, said he is expecting a long period of very accommodative monetary policy and that the ECB might consider buying fallen angels if necessary

- The issue volume in the German bond market increased from €116.4 billion to €176 billion and the circulation of foreign bonds in Germany increased by €3.6 billion between March and April

- The IMF published a blog by the Managing Director of the IMF, highlighting the need to ensure an inclusive recovery prioritizing fiscal stimulus, education, and the promotion of financial technology.

- The German government launched parts of its recently agreed stimulus package that included VAT reductions from 19% to 16%, and 7% to 5%.

- The German Institute for Economic Research has calculated that the German stimulus package could help the German GDP decrease by 8.1% instead of 9.3% percentage points between 2020 and 2021. The Institute expects GDP to grow by 4.3% in 2021 assuming no second wave hits the country.

- It is being reported the ECB is working on a pan-European plan to protect commercial banks from the rising amount of Non-Performing Loans (NPLs) in the context of COVID-19.

- The ECB is projecting a contraction of 13% of the euro area GDP in the second quarter of 2020, leading to a decrease by 8.7% for the year 2020 as a whole. It expects growth of 5.2% in 2021 and 3.3% in 2022.

- The French Central Bank released its June economic forecast, showing that the economy should start recovering in the second half of the year. Overall, 10% of GDP could be lost in 2020. The unemployment rate could reach more than 11.5% of the workforce by mid-2021, before decreasing in 2022.

- The Bundesbank is projecting that Germany’s economy will recover in 2021 and 2022 after a 7% diminution of the GDP in 2020.

- The Danish central bank has assessed the liquidity reserves of Danish companies in light of Covid-19, concluding that the median firm has internal liquidity reserves to cover approximately one month of fixed costs, while one third have virtually no reserves.

Engaging with the treasury community

We welcome conversations with our members on:

- How you’re dealing with the crisis

- What you’d like us to raise with the various bodies we are in regular contact with

- How the ACT can support you during this challenging time.

Send an email to technical@treasurers.org and either James Winterton, Naresh Aggarwal or Sarah Boyce will be in touch with you.

If you have found any resources which you feel we should add to our COVID-19 site, please email us with details.

Naresh