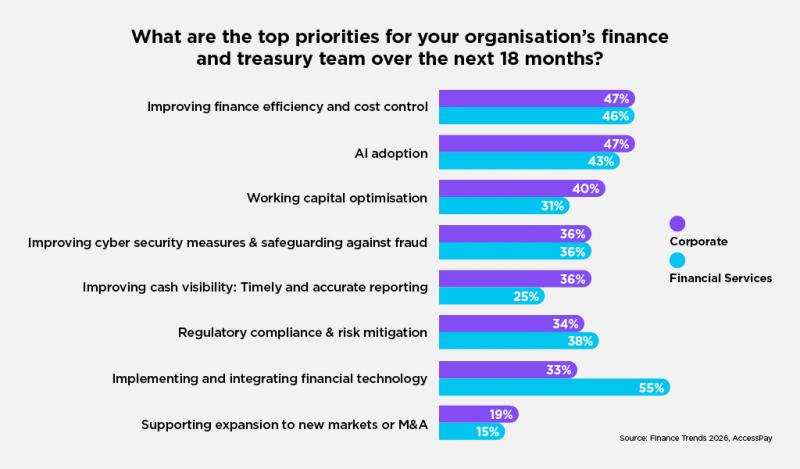

AI adoption and improving finance efficiency and cost control have come out as the top business priorities in a survey of treasury and finance leaders. However, working capital optimisation, improving cybersecurity and cash visibility are not far behind in the list of priorities for corporate businesses, according to AccessPay's Finance Trends 2026 report.

With sluggish economic growth and sticky inflation, finance leaders across all sectors continue to prioritise finance efficiency and cost control. This has been an enduring theme since AccessPay’s Finance Trends survey began in 2022, but the last 12 months have provided particular challenges, the report says.

As Karen Fagan, head of treasury consultancy services at AccessPay, says: “Corporate finance and treasury departments are being asked to do more with less. Interest rates are high and everything from people to energy has become more expensive.

“Finance and treasury teams are working hard to manage budgets and control costs, but there is always the question of how best to achieve that. Corporates need to weigh carefully whether to reduce headcount or implement new systems to increase automation.”

However, beyond the commonalities of efficiency and AI, there are clear differences between the priorities of finance leaders in financial services organisations and their opposite numbers in the corporate sector. While financial services are heavily focused on financial technology, corporates are focusing on working capital optimisation, cybersecurity and cash visibility.

This is a standard part of financial management, but is even more critical in the current macroeconomic environment, with fragile demand and high borrowing costs, AccessPay reports. And most medium-and large-sized corporates, particularly those that operate internationally, work with multiple banks, making it difficult to determine their up-to-date cash position, which slows strategic decision-making.

“It’s a volatile market, so maximising cash becomes more important,” says Anish Kapoor, AccessPay’s CEO. “Businesses will be stress-testing plans, running scenarios, and checking that they can continue to operate at the low end of their scenarios. This may have implications for cost control or even reduction.”

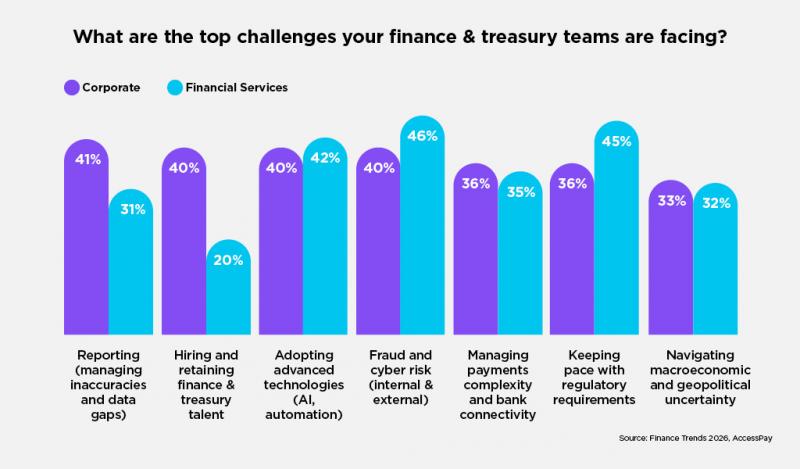

In the corporate sector, business challenges and evenly spread across a number of issues, including data gaps, talent, advanced technologies and fraud. In financial services, the key concerns are fraud and keeping pace with regulatory requirements.

“When automating, leaders need to think beyond efficiency and consider data integrity, control, and future readiness from the outset,” Kapoor says. “Creating a unified data layer between internal systems and banks is one of the most practical steps organisations can take today.”

According to the report, strengthening resilience, security and fraud controls featured strongly for both financial services and corporates. These are always critical considerations for a strong finance and treasury function, but new legislation, notably the Failure to Prevent Fraud Offence, introduced under the Economic Crime and Corporate Transparency Act 2023, is also likely to drive activity.

AccessPay warns that, from 1 September 2025, large firms are now criminally liable if an employee, agent, or associate commits, or intends to commit, fraud that benefits the firm, and the firm does not have adequate procedures in place to prevent it. The firm’s senior managers and directors do not need to have ordered or been aware of the fraud to be held liable.

Philip Smith is editor of The Treasurer