Yusen Germany is the local subsidiary of Japan-based Yusen Logistics Group, an international freight forwarding and logistics group.

The international nature of this business leads to a large proportion of its transactions being denominated in foreign currency, resulting in a significant foreign currency exposure.

Yusen Germany was not strategically addressing its FX risk, which meant substantial foreign currency impacts. During the financial year 2017/18, foreign currency losses totalled about 0.5% of gross revenues, which hurt the financial performance significantly.

Bearing in mind notoriously low margins in the freight forwarding industry, with the most profitable players reporting net margins of about 5%, the pressure was mounting to deal with the exposure going forward.

Initial attempts to hedge were based on the use of individual forward contracts to eliminate the foreign currency exposure associated with cash flows denominated in USD.

The dynamic, complex and highly transactional business model of international freight forwarding, however, makes it extremely difficult to make precise cash-flow projections.

Additionally, there is the question of whether the exposure should be addressed on an aggregate level or based on individual transactions; and whether to hedge on a gross or net basis considering cash inflows and outflows.

The seemingly simpler approach of addressing risk on an aggregated net basis still required significant efforts for follow-up and modification due to the ever-changing FX exposure.

Depending on the client’s preference or internal regulations, a tiered review and approval scheme can be put in place

Executing deliverable or non-deliverable forward contracts by traditional email and phone trading turned out to be too cumbersome and error-prone to manage the FX risk effectively.

Lastly, the accounting treatment of hedging instruments posed a challenge, since there was limited expertise at Yusen Germany on relevant accounting standards, such as the relatively new IFRS 9 on financial instruments.

Accordingly, there was a preference to engage only in short-term forward contracts that settled before month end closing in order to avoid any entries in the financial statements. Ultimately, these attempts did not prove to be effective.

In April 2018, Yusen began discussions with Deutsche Bank to explore options to address Yusen’s currency exposure.

Maestro is an automated FX solution embedded in the online banking environment of Deutsche Bank as a separate application, which provides complete execution transparency while simultaneously reducing the operational risk of traditional forms of execution.

Essentially, the application allows each client to upload or manually enter information regarding their FX exposure, which is then translated by the application into currency hedges.

The approach is flexible and adapts to information provided at different levels of aggregation and format. It supports the entire spectrum from uploading an aggregated FX exposure as a single-line item to many individual sales transactions.

Likewise, there is no limitation as to the frequency of the upload and modification of the FX exposure; monthly, weekly, daily and technically even hourly modifications are possible.

Additionally, rules can be defined in order to put in place a comprehensive level of security as well as a high degree of automation.

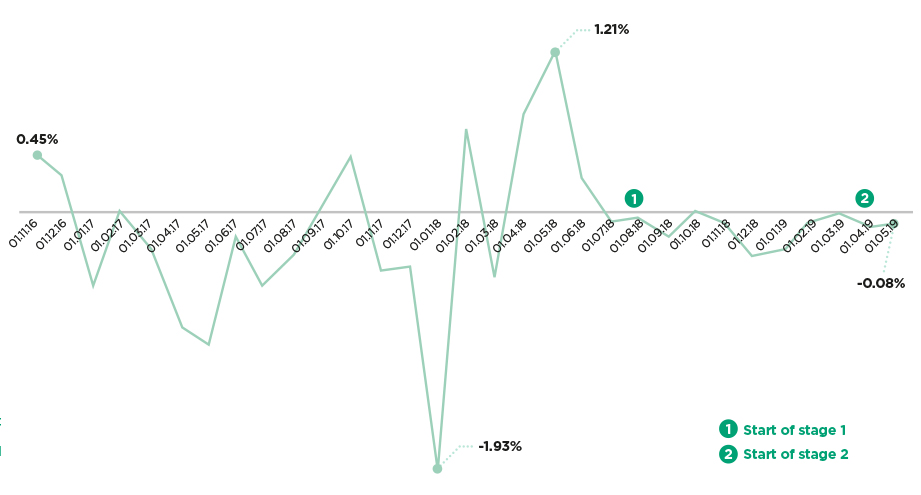

In order to gain expertise and a sufficient level of comfort, Yusen Germany decided to adopt the application in two stages. In the initial stage, only accounts receivable (AR) denominated in USD with a large third-party client were hedged using Maestro.

In the second stage, Yusen Germany advanced to comprehensive semi-automated balance sheet hedging of the entire USD exposure considering third-party AR and accounts payable (AP), intercompany AR and AP, as well as cash.

The implementation started with the hedging of a large third-party business denominated in USD. The underlying business was based on monthly invoicing with 60-day credit terms.

Whenever an invoice was issued in Yusen’s operating system and interfaced into the accounting system, the corresponding AR on an individual invoice level were uploaded to Maestro and converted into forward transactions, thus providing immediate protection against USD movements.

The trades are made available by the application for review and approval. Depending on the client’s preference or internal regulations, a tiered review and approval scheme can be put in place.

In order to provide flexibility and maintain protection against currency movements, Maestro would always settle all open trades at month end and roll-forward trades by means of a currency swap until the subsequent month end.

Accordingly, Yusen Germany is always kept in a fully protected position, even if the collection of receivables is delayed. As and when a receivable is collected, the corresponding USD amount can be drawn down from the existing hedge by means of a swap.

The benefit of the drawdown is to manage liquidity and to claim back the interest rate differential from the date of the collection until month end when the forward would settle.

The logic of this approach implies that all trades settle at month end. The only trade open from one month to the next is the aggregate roll-forward trade, conducted at the end of the month. All hedges are settled and rolled forward by new swap transactions.

Consequently, there is no requirement for a comprehensive hedge accounting using mark-to-market reports.

After about six months, it was decided to take the next step and advance to full balance sheet hedging with the support of this solution.

In order to provide protection for all USD transactions, it was decided to hedge the net amount of AR third party, AR intercompany, AP third party and AP intercompany.

The corresponding amounts were extracted from the accounting system, netted to an individual USD figure and uploaded into the application. The USD cash position of Yusen Germany’s USD bank account with Deutsche Bank was supplied to the app via an internal data-messaging service.

The net AR/AP position, the USD liquidity in the bank account, as well as any pre-existing hedges, constitute the overall USD exposure. In order to be fully hedged, all the before-mentioned exposures should be zero.

Once the netted AR/AP position is uploaded by Yusen Germany, the application calculates a hedge adjustment, taking into consideration the cash position and existing hedges.

The hedge adjustment is made available as a trade in the application that can be reviewed, amended and approved by the authorised users at the company. The hedge adjustment can be calculated and effected at any time. Currently, a weekly process has been adopted.

The financial reporting shows clearly that the hedging approach is effective. The FX effects in per cent of revenue – as shown in the graph below – could be reduced greatly.

Further improvements shall be made by extending the hedging programme to other currency exposures as well as by increasing the upload frequency.

It must be pointed out that there are various regulatory and reporting requirements to be considered, such as IFRS 9 as well as European Market Infrastructure Regulation (EMIR) requirements.

EMIR is a body of European legislation for the regulation of over-the-counter derivatives. Non-financial organisations, such as Yusen Germany, that only enter into derivative contracts with the intent to reduce risk, are likely to be exempt from many of the requirements of EMIR.

However, for transparency, non-financial counterparties must comply with the requirement to report to trade repositories. At Yusen, it was decided to delegate this requirement to Deutsche Bank.

In order to ensure full compliance with relevant regulatory requirements, it is recommended to consult a specialised accounting firm.

The implementation of an automated hedging solution has significantly reduced the impact of FX gains and losses at Yusen. Once implemented, the workload and complexity of the solution is relatively minimal.

The implementation of the hedging process requires focus and specialist advice, especially if there is limited experience with hedging solutions and FX theory.

It is recommended to build a project team with internal and external stakeholders and to schedule regular workshops, including face-to-face meetings.

Stefan Karenfort is CFO at Yusen Logistics Germany

Xavier Szebrat and Jay Hoffman have contributed to this article. The author would like to express his sincere gratitude to Detlef Hufen, Xavier Szebrat, Jay Hoffman and Felix Wacker-Kijewski for making the FX project at Yusen Germany a success.

This article was taken from the October/November 2019 issue of The Treasurer magazine. For more great insights, log in to view the full issue or sign up for eAffiliate membership