The Prompt Payment Code (PPC) is a voluntary code in the UK that sets standards for payment practices and best practice.

It is administered by the Chartered Institute of Credit Management (CICM) on behalf of the Department for Business, Energy and Industrial Strategy. Compliance with the principles of the code is monitored and enforced by the PPC Compliance Board.

The code covers prompt payment, as well as wider payment procedures.

In 2015, the Small Business, Enterprise and Employment Act introduced a requirement that large businesses should publicly report on their payment practices behaviour.

The legal requirement was brought into force by the regulations that came into effect in April 2017, and the process (sometimes referred to as ‘duty to report’ but more formally known as payment practices reporting) is now established.

We are at a point where all large businesses should have published their payment performance. If they haven’t, a criminal offence is being committed.

From 1 September 2019, any supplier who bids for a government contract above £5m per annum will be required to answer questions about their payment practices and performance. The expected standard is to pay 95% of invoices in 60 days across all their business.

Any supplier who is unable to demonstrate that they have systems in place that are effective and ensure a fair and responsible approach to payment of their supply chain may be excluded from bidding.

Based on the new payment practices reporting data that large businesses must publicly report, CICM reviewed whether businesses were meeting the standards of the code and paying their suppliers promptly.

The first phase of these reviews in April identified 17 businesses to be removed or suspended, with more removals and suspensions expected in the second phase of review currently under way.

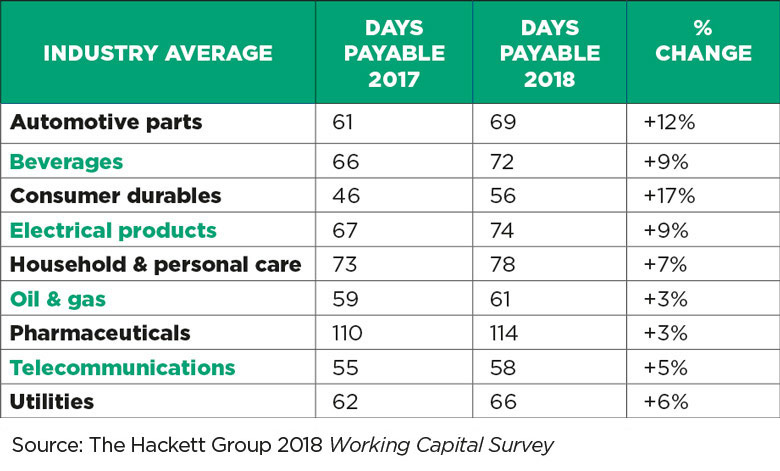

We’re all aware of the stories about how the payment practices of large organisations continue to restrict the growth of the SME and microbusiness sector and research from The Hackett Group confirms this.

The payment term objectives of the code have been raised by a number of treasurers and The Association of Corporate Treasurers’ (ACT’s) policy and technical team undertook some research via the Treasury Forum [1], following the first phase in April.

Our findings showed that all respondents were aware of the code and 67% had signed up to it (including subsidiaries).

Most respondents were comfortable with the aim to move to 60-day payment terms, but many were concerned about the objective of 30 days.

It’s clear from our discussions with treasurers that for many organisations, the people, processes and systems are not capable of supporting such payment terms.

Lack of consistency on invoices, the use of purchase orders and the level of disputes all made it more difficult to achieve faster settlement of invoices.

In addition, many firms have negotiated longer payment terms that suit both parties – especially if it gives time to resolve queries.

However, the PPC is not going away and, if anything, the code is likely to get more teeth.

At a recent interview with the Small Business Commissioner Paul Uppal, there was discussion about the need for fines and independent investigations, to force businesses to comply with these payment objectives.

Corporate treasurers must ensure they don’t take the easy route on working capital improvements by extending payment terms. They also need to support efforts of their business to pay promptly – before it gets regulated.

[1] The Treasury Forum is a cross-section of more than 100 members who we regularly reach out to for insights on a particular topic. Contact Louise Tatham or the policy and technical team if you would like to join

This article was taken from the August/September 2019 issue of The Treasurer magazine. For more great insights, log in to view the full issue or sign up for eAffiliate membership