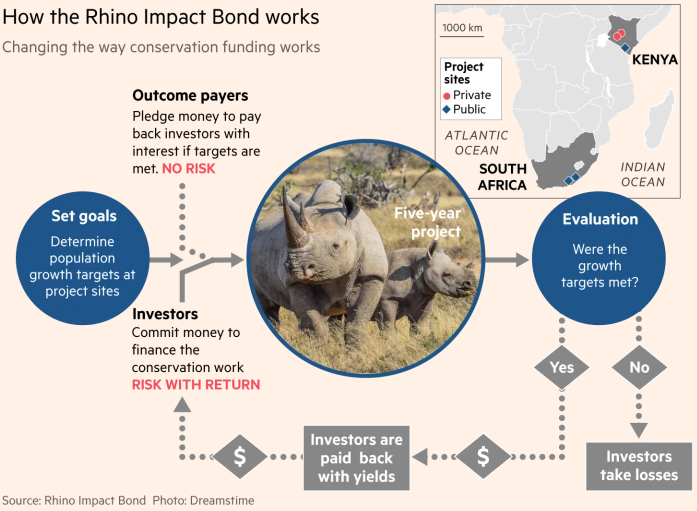

Investors in the 5 year $50m bond will be paid back their capital and a coupon if African black rhino populations in five sites across Kenya and South Africa increase over five years. The yield will vary depending on changes in the rhino population. The bond will have different categories of investment, with some investors taking a “first loss” position if rhino population targets are missed, according to Conservation Capital, who arranged the offer. If rhino numbers drop, those investors will lose their money depending on the scale of the decline and the terms of their investment while investors in other categories will be repaid.

This “outcome payments” model has been used by other issuers to finance health and education projects — could revolutionise conservation financing as traditional donors such as governments and multilateral organisations will disburse money only on results. It could also bring the private sector into species protection in a new way, because the return on investment will comprise both a financial return and a measurable conservation objective. However care will needed over the transaction costs for deals such as these to ensure that there is a fully costed genuine benefit.

Gender equality bonds are a way of making sure that equal opportunity is a priority in the businesses that investors back. Calling for more women on the board is now very much old school. This relatively new form of debt means investors can have an even larger influence.

In addition to public sector institutions such as the World Bank and private sector banks such as National Bank of Australia, during the summer, a Turkish private lender implemented a "Gender Loan" structure to finance a massive wind farm project. Within the scope of the "Gender Loan," Garanti BBVA teams will score Polat Energy's performance in the field of gender equality in accordance with international norms every year. The score will be updated and the first assessment will be considered the base. In subsequent assessments, if the company rises above the base point, the cash loan interest and non-cash commission fee will be reduced.

In 2017, Australia’s QBE Insurance Group issued a US$400m gender equality bond designed to finance or re-finance debt from companies that met its equality standards. The issue was massively oversubscribed with demand of over US$9bn, reflecting increasing investor demand for Environment, Social and Governance Bonds and demonstrating that it’s not just a philanthropic exercise but commercially viable.

The European Investment Bank (EIB) has proposed to stop funding new fossil fuel projects by the end of 2020.

It is part of the Bank’s plans to contribute towards meeting the goals of the Paris climate agreement as laid out under its draft energy lending policy.

It intends to phase out support to energy projects reliant on fossil fuels, including oil and gas production, infrastructure primarily dedicated to natural gas, power generation or heat-based on fossil fuels.

The EIB says these types of projects will not be presented for approval to the EIB Board beyond the end of 2020 as the bank moves to increase support for energy transition in Europe and the decarbonisation of the European economy.

Two CLOs closed in the summer that included explicit ESG investment restrictions. These vehicles will be used to buy about $1bn of leveraged loans and will exclude debt issued by companies that make or market landmines, chemical weapons and thermal coal. Another CLO, which closed in July, attracted $124m from the Overseas Private Investment Corporation, the US government’s development finance agency. Targeting loans made to micro-firms in emerging markets, the CLO is aimed at improving financial inclusion providing capital to about 5.6m microfinance borrowers, 81 per cent of whom are women.

Atlantica Yield, a London-based renewable electricity investor, signed its first ESG-linked financial guarantee line worth about $39m. The guarantee’s interest rate will be linked to ESG performance with the funds used solely for renewable assets. The guarantee, which was signed with Dutch bank ING, will cost Atlantica less than 2 per cent, but could increase or decrease annually based on ESG ratings.

I’m sure there’s lots more that I missed and happy to hear about them!