The payments landscape continues to evolve and this blog shares some of the topics that caught my attention during the last month. If you think I’ve missed anything important, do please send an email to technical@treasurers.com.

Market news

On 18 January 2021, Konsentus acquired Open Banking Europe S.A.S. from PRETA (a fully-owned subsidiary of the EBA). Formed in 2017, the OBE initiative has brought market participants together to identify issues and create workable solutions, standards and tools. the OBE 'Regulatory Directory' is a single, standardized and machine-readable repository of regulatory data that consolidates and makes available information from the National Competent Authority registers. It is used by over 500 of the largest financial institutions across Europe to support PSD2 access to account compliance processes.

Central Bank Digital Currencies (CBDCs) and other digital currencies

It is becoming increasingly difficult to keep up with all of the announcements from a raft of central banks and think tanks but here are some that caught my attention:

A clear objective for the bank will be to establish whether issuing the e-krona to the general public in electronic form is a realistic and achievable prospect. Although the Riksbank supports continued use of cash in the Swedish economy, it recognises the unstoppable force of digitised payments. Its long-term strategy is to position the e-krona as a financial tool that could allow the general public future access to its money if Sweden goes cashless.

It goes on to note the possible development of a synthetic CBDC backed by a basket of global CBDCs which was proposed earlier by former Bank of England governor Mark Carney. Such a digital reserve currency could provide efficient cross-border payment services, meaning faster processing, due to the credibility of multiple central banks backing it.

Interesting reports

The Paypers has launched the Cross-Border Payments and Ecommerce Report 2020–2021. One of their findings was that 73% of cross-border shoppers want to pay in their own local currency and 45% of cross-border shoppers felt uncomfortable buying in a foreign currency. Displaying prices in local currency is not optional. Retail Info System’s research showed that one in four shoppers left a website if their local currency was not displayed.

The EPC issued its annual Payment Threats and Fraud Trends Report which provides an overview of the most important threats and other “fraud enablers” in the payments landscape. In its conclusions it notes that “the main attack focus over the past year has continued to be the trend of shifting away from malware to social engineering attacks. Social engineering attacks, phishing and vishing attempts are still increasing and they remain instrumental often in combination with malware. Whereas in the past consumers, retailers and SMEs had been the main focus, the last year more and more company executives, employees (through CEO fraud), financial institutions and payment infrastructures appear to become preferred targets.”

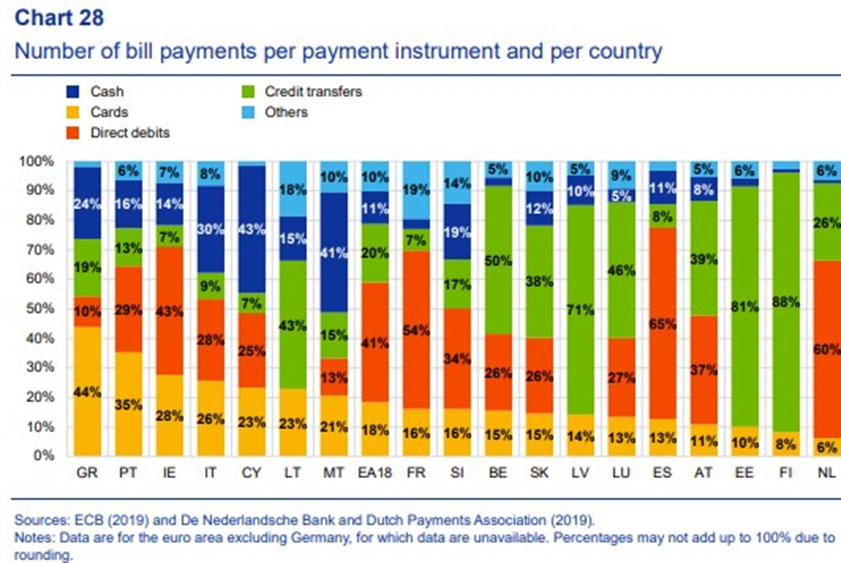

The ECB issued its Study on the payment attitudes of consumers in the euro area (SPACE). This surveyed 41,000 people during 2019, in 17 countries participating in the euro, and provides a comparison to a similar study undertaken in 2016. One area that caught my attention was:

“Chart 28 shows considerable variations in the country-level results. Direct debits were used in more than 50% of all bill and recurring payments in Spain (65%), the Netherlands (60%) and France (54%), and credit transfers in 50% or more of the payments in Finland (88%), Estonia (81%), Latvia (71%) and Belgium (50%). The wide use of credit transfers in the Baltics and in Finland can be explained by the high use of electronic invoicing in these countries. Moreover, the use of direct debits in general could be under-reported as, contrary to the other payment instruments which require an action from the payer, direct debits are passive, are automated and do not need to be pushed by the payer.”

UK payments landscape

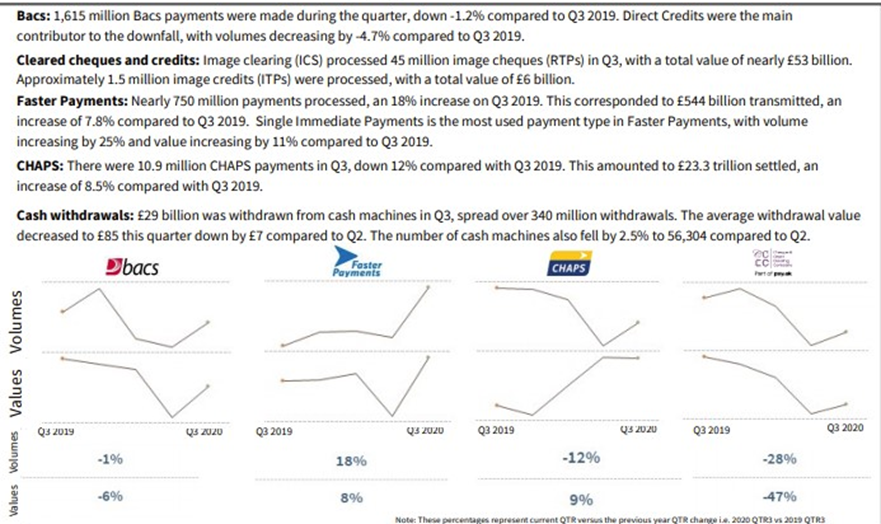

Pay.uk published its “Summary of key payment statistics for Q3 2020” which includes the following table:

In December 2020, The Bank of England published an updated self-assessment of the RTGS and CHAPS services against the CPMI-IOSCO Principles for Financial Market, with point of assessment 31 August 2020. This was the third integrated self-assessment covering RTGS and CHAPS since the Bank took on responsibility for delivering CHAPS in 2017.

The principles are internationally agreed standards considered essential to strengthening and preserving financial stability.

The Bank judged that of the 17 principles that apply to RTGS and CHAPS, it ‘observed’ 16 and ‘broadly observed’ the last one (risk management).

The PSR consultation on card acquiring services is open until 9 February. If you are interested in responding directly, this is the link. If you would like to contribute to a response from the ACT please send an email to technical@treasurers.org

Naresh Aggarwal